Turn on suggestions

Auto-suggest helps you quickly narrow down your search results by suggesting possible matches as you type.

Showing results for

Get 50% OFF QuickBooks for 3 months*

Buy nowAs a recent treasurer,using QB desktop Premier for Non Profits, I f ind our cash and fund accounting has been adequately managed through using bank sub accounts identified as temporarily restricted and non restricted. A new accountant has directed the use of equity accounts to replace thie bank sub accounts and I am trying to determine how to best track transactions through our system when QB registers are primarily bank registers.

Premier provides for Balance Sheet by Class; that's why you didn't need to micromanage by Subaccounts, or more Rows in the financial reporting. That's why you don't use Pro, which doesn't handle Bal Sheet by Class and requires micro-management by subaccounts.

What the accountant describes does not Replace Banking by Class. They are describing Rebalancing Equity, which is in addition to managing Bank. This is covered in the book Running QB for Not For Profits, by Kathy Ivens.

You don't necessarily need to Rebalance Equity for everything, if you are properly using Bal Sheet by Class. If you intend to micro-manage Rows, you don't necessarily have the segregation required. That is likely why they made the suggestion to add Duplicate Data handling.

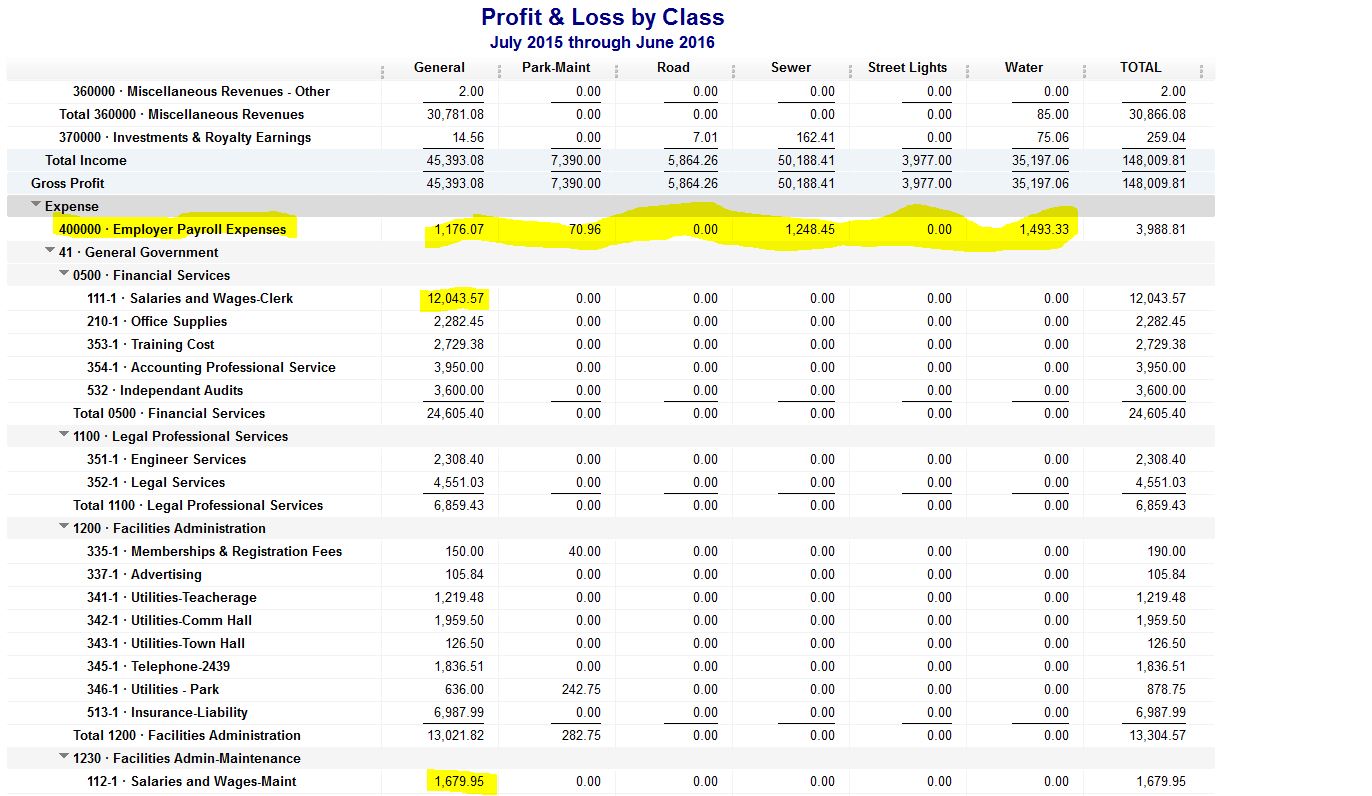

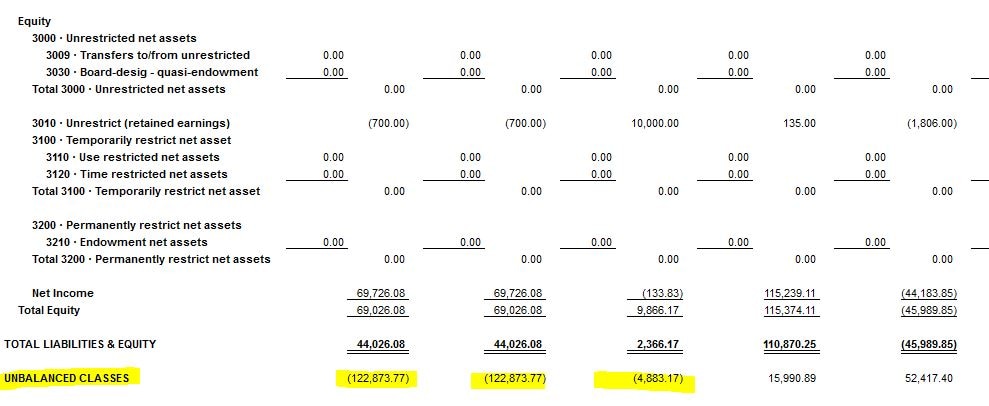

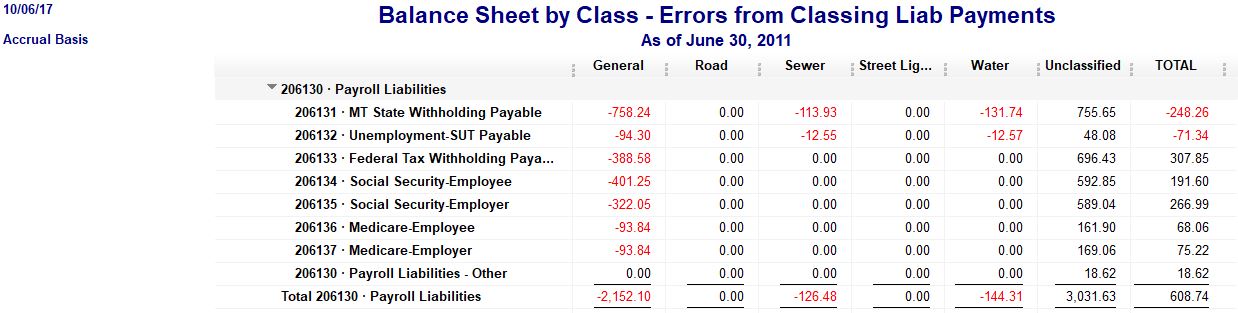

I have an attached example of a file that was in Pro, and once we moved it to using Class and to Premier, you can see the redundant ZERO rows. We also simplified their banking and found lots of out of balance errors.

Thank you for your response. It appears, then, that the accounts as I received were managed by several prior and correct establishment of class structure was attempted but not achieved resulting in a large COA and somewhat redundant classes.

I have been using the Kathy Ivens book, Running QuickBooks in Non-Profits as well as QuickBooks for Churches by Lisa London and can not seem to find the references to Rebalancing Equity or the accompanying managing bank management to which you refer. I continue to search.

Thank you for your response. It appears, then, that the account I have acquired has had several previous owners resulting in a large COA, structured in departmental accounts and a never fully developed class or job structure which where existent almost is redundant to the account lines.

I have been working with the Kathy Ivens book, Running QuickBooks in Nonprofits, as well as QuickBooks for Churches by Lisa London and am having attempting to locate reference to the rebalancing equity with the accompanying bank management to which you refer, in either book, but am not yet successful.

Thank you, again.

Kathy describes it, and I took an online Church accounting with QB session that includes it. It's pretty easy to understand:

QB closes Net Income to Retained Earnings, or Unrestricted Net Assets for the first date of the new fiscal year; so, everything you do is relative to that account, even if yours is named Net Fund Balance. Open the Chart of accounts and Double-click each Equity account. Whichever one does Not Open as a register view, that is Yours.

You get a Restricted Grant, so that amount that is going to Increase net income and Increase Restricted banking and Increase Restricted Net Asset (equity). I would decrease Unrestricted Net Asset (equity) and Increase the Restricted Funds balance (equity). I can do this routinely, monthly, with every financial transaction, or only at year end. I run a Single Purpose Entity, so I don't do Equity Rebalancing at all in that file.

Now, you are ready to Spend Restricted Funds. Let's buy something for $500. On the Check Details, it would be Splits:

Office Supplies $500 <== provides the Debit to supplies expense; Class = Restricted (or the Program/Purposes that by definition is Restricted or not); Job = Grant name here; not Billable (you already got the income)

Unrestricted Net Assets Negative $500 <== makes a Credit = Increases it (because FYE will result in All Expenses closing here, which will reduce it again, anyway)

Restricted Net Assets Positive $500 <== makes a Debit here, showing you Used Some, and that Decreases the Net Amount restricted in this file

Or, you enter the Spending for that event, and separately make a JE. The JE will Debit Restricted (used some Funds) and Credit Unrestricted, as I noted.

But, you cannot use an Out Of Balance By Class JE. That JE is for Rows, not Class, because you would be "Moving" across the Bal Sheet Columns, and equity = Net Assets. That means the Banking Changes for funds spent are no longer in the same Column as that JE.

That's why you try to reduce the chaos and not make the work harder than necessary. If you wanted to use Pro, not Premier, to manage By Class, then the Row redistribution makes sense. In Premier, you Already see Equity = Net Funds Balance" in Columns by Class, in the reporting.

That's why I was surprised that this Accountant asked you to rebalance Equity, but didn't scold you for managing Banking using Subaccounts :)

Please see my attachment, from the same sample file you have in your program's list in the No Company Open screen, bottom right.

Again, thank you for your response. I will, as you mention, look for the online Church accounting QB session.

Commenting on your last paragraph first, the accountant did in fact scold me for using bank subaccounts to separate the temp restricted funds and unrestricted fund accounts. Since they are all in the same bank it seemed reasonable, and it has also been suggested by each of the books mentioned. What had not been described in the books and has been very clearly described in your response to my query was the method to have the proper equity accounts agree with what seemed to be correct to put in segregated "bank accounts". I have been instructed to eliminate the bank sub accounts through the use of JE to populate Equity accounts created with the same or similar name and the same character (temp restricted and unrestricted).

The instructions have been apparently unclear and my execution imperfect.

The church maintains two departments: a church department with an unrestricted operating fund account, and several temp restricted funds accounts; and a second department with a second department restricted fund account within which there are several departmental temp restricted funds(grants) and departmental unrestricted fund accounts (all temp restricted from use in the church accounts).

All of this made the segregated bank sub accounts seem reasonable.

In your response you make mention of the use of "Restricted Banking" ( I will assume it is not a separate bank account, but a bank sub account)

My real next step has to be to revisit the class list, reducing it from a previous size. There is a large number of lines in the COA reflecting departmental separation and each with the "program/fundraising/administration" sections. (This has been the legacy from several predecessors).

My use of the desktop premier is supposed to make the book keeping and accounting system easier than the other versions of QB but in the need to serve each product the explanations appear to be not necessarily specific for the learning user.

Thanks again.

I used this:

http://www.churchaccountingsoftwareguide.com/

This is why Class is used = Creates Columns. You don't need more Rows:

"was the method to have the proper equity accounts agree with what seemed to be correct to put in segregated "bank accounts"."

You only need Rows when you are using QB Pro, which does not create Balance Sheet by Class.

"I have been instructed to eliminate the bank sub accounts through the use of JE to populate Equity accounts created with the same or similar name and the same character (temp restricted and unrestricted)."

Did you simply run Bal Sheet by Class, to see Equity is already doing this? And you don't use JE for this. I noted the problem with that concept. Banking doesn't use JE, and Mixing class on JE also is a problem. I showed that report problem as an attached image.

"In your response you make mention of the use of "Restricted Banking" ( I will assume it is not a separate bank account, but a bank sub account)"

No; I am the one trying to keep from using Micro-managed subaccounts in Banking, since you bought QB Premier. The Bal Sheet by Class would reflect that the Grant Income for a restricted purposes is "income = new asset in the Same Column." Not more Rows.

You would run the Bal Sheet by Class. If that looks fine, you simply Merge all that bank subaccounts into each other, then move it to be Parent and Merge it into what was its Parent.

"My real next step has to be to revisit the class list, reducing it from a previous size."

The best reference is the tax form your entity files. There is the UCOA for reference, and I cannot attach an Excel file here, so search the web for:

UCOA Keywords

To find that cross-reference Excel file that is amazingly helpful.

"There is a large number of lines in the COA reflecting departmental separation and each with the "program/fundraising/administration" sections. (This has been the legacy from several predecessors)."

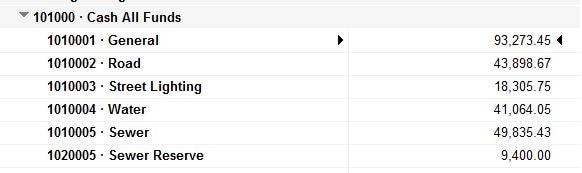

Yes, I showed that in my attachment from my client, we transitioned them from Pro to Premier. Please see the attachment here that was their banking structure. The other problem was that they micro-managed as Subaccounts, separate and real bank accounts in real life, under a common Parent. You never do this. Someone even made an Upper Level Parent, in the Chart of Accounts, linking all of them; the reporting already does this as Cash and Equivalents, but someone made "Cash All Funds" which is an error for reconciling and managing. Now you need multiple statements and need to do the math, to Reconcile an Artificial Parent, such as "Sewer Reserves" is one part of operating checking + a CD, as an example.

"My use of the desktop premier is supposed to make the book keeping and accounting system easier than the other versions of QB but in the need to serve each product the explanations appear to be not necessarily specific for the learning user."

Programs are simply tools. I hand you a hammer, and show you how to Hold and use it. Separately, I have to teach you to build a doghouse or a hospital with it.

"The instructions have been apparently unclear and my execution imperfect."

You are Learning. Some tools work better than others for specific needs. Don't be so hard on yourself. There is a Lot to learn for each type of Client File you work with. I have gone to seminars and had direct support from two different State employees for governmental accounting, because they rely on my to be the QB resource when they get a town clerk or other governmental unit trying to use QB. I know QB, the two State employees know what the State requires, and together, we try to teach the clerks what to do and I teach them How to do it using QB.

And by the way, I have them get Desktop Accountant. Premier is fine, too. Online is inadequate and Pro is inadequate. So, you are on the right track.

Upon further thinking, let me try this concept:

"I have been instructed to eliminate the bank sub accounts"

Yes, you can Merge, as I noted.

"through the use of JE"

That won't be used for Banking. That can be used for Rebalancing Equity, as I noted.

"to populate Equity accounts created with the same or similar name"

Yes, you can use a JE in balance by Class, to rebalance Equity. Do Not Change Banking. That isn't your issue.

If, for instance, you realize the Subaccount bank for "Day Care Class" is seen only in the row as Unrestricted Net Asset, then the JE is:

Debit Urestricted Net Asset, Class = Day Care

Credit Restricted Net Asset, Class = Day Care

To show the Amount in subbank is also Restricted Equity. And you do this only if you intend to Micro-manage and rebalance Equity.

If, instead, you run Bal Sheet by Class and the value from Day Care bank subaccount already is in the right Column, but the Tow = Unrestricted Net Asset, then rename that one equity account to be Fund Balance. The Column identifies Restricted or Not.

And of course, this would not meet your needs if you need Restricted, Unrestricted, Temp Restricted, Time Restricted, Committed, etc, as that is a Lot of Class and Subclass details. In this example, you very well might also want to use the Rebalancing of Equity with Every transaction, as I previously noted.

Don't let this person treat this as "Just make one large JE like ripping off the bandage" because you cannot finesse the data using a Brute Force accounting entry. I showed Out of balance Bal Sheet, from that concept. Sometimes, taking a client file from Pro to Premier also reveals their Class Tracking errors, and then we need to fix these, as you see in my attachment here.

Thank you for responding. I do appreciate your pointing to churchaccountingsoftware guide. I have completed it and am very please with the work the author put into its creation. I did, however come away asking where in the cycle of the year, either monthly or annually, do the Unrestricted Net Asset equity and Temporarily Restricted Net Asset equity accounts get populated. In the entire main part of the course material (not in the appendix) there was only the reference to these accounts in the initial setup. When are they used? If funds are captured there, at what frequency? At the monthly reporting, or annual reporting cycle? The Statement of Financial Position shows the "calculated net income" from the Statement of Financial Income and Expense but

I am having difficulty understanding what the problem is with maintaining QB sub bank accounts, designated as unrestricted and temporarily restricted with sub-sub accounts indicating restriction by specific grant when they themselves are Net Asset accounts as money moves in and out.

I certainly am going to do the work to judiciously work with the COA and class structure.

Returning to your response, you indicated I might gain insight into looking at the form our entity files. We are rather a small religious organization and what ever tax forms are prepared are done so by our payroll company. We are not required to file a 990. We do, however have donors and search for grants that require us to maintain standard reporting. There is a section in the churchaccountingsoftware guide intended for some guidance in the GAAP but I have not gotten that started as yet. I was more disappointed as noted earlier regarding the treatment of the equity accounts.

Thanks again.

"I did, however come away asking where in the cycle of the year, either monthly or annually, do the Unrestricted Net Asset equity and Temporarily Restricted Net Asset equity accounts get populated."

On any date you run the Balance Sheet "as of" you see that the Net Income from the P&L (income statement) is also reporting as Net Income in Equity. On the first date of the new fiscal year, as I explained, this is "rolled into" Whichever of your Equity accounts really used to be Retained Earnings = the one Not Opening as a Register View. The Program does this. That's why you are the one that needs to rebalance them if you are going to use rebalancing equity as part of the methodology. So, the question of, "Where in the clcye does this happen?" Is going to be answered as, "When you Date your activities and how often you do them." I noted it can even be with every transaction where that change needs to be reflected. That Church Accounting guideline was monthly, if I recall right.

"In the entire main part of the course material (not in the appendix) there was only the reference to these accounts in the initial setup."

In the Appendix, I see it in lesson 43.

"but I am having difficulty understanding what the problem is with maintaining QB sub bank accounts"

You are the one that asked about meeting your accountant's request. You would have to ask that person why they want you to use Equity Rebalancing. As I noted, it is a valid method or strategy that doesn't Have to be used at all. I also explained the differences between Pro and Premier. You are using micro-management of banking as Rows, which doesn't need to be done in Premier, because Premier shows it as Columns in the "By Class" reporting. Pro needs it to be managed by subaccounts, because Pro does not manage Balance Sheet By Class.

"by specific grant"

Grant is Customer, or Customer and Job tracking. That way, you can run, for instance, P&L by Class, filter on Name = County, to see all Program funds provided by county grants. Or, P&L by Job, filter on Program = Food Bank, to see the columns for each Grant you received that was a funding source or source of spending for the Food Bank.

"Returning to your response, you indicated I might gain insight into looking at the form our entity files."

Get the UCOA. Get the UCOA keywords Excel file, a great cross-reference resource.

"We are rather a small religious organization and what ever tax forms are prepared are done so by our payroll company."

These are Resources that help you understand the types of terminology and how that applies to operations and activity tracking and reporting. That isn't Payroll. That is understanding how to set up and manage Activities using some standards that apply in your Industry. Just like manufacturing has Work In Process, Bills of Materials, and Costs of Goods Sold, you have standard terminology and tracking references.

"We are not required to file a 990"

Think of this as a dictionary and a Thesaurus and a Look Up Cheat Sheet. No one stated you Must File anything. What I state in my classes is, you cannot report what you did not track.

"We do, however have donors and search for grants that require us to maintain standard reporting."

There you go!

Again, thank you. I did follow the lessons 42 and 43 more closely and understand how it is done. Still a little unclear if there needs to be continuous transactions into the Net Asset accounts.

The following direction has been made to utilize NA accounts instead of bank subaccounts for restricted and unrestricted assets:

"Journal entry to eliminate sub category bank account balances."

"Example: Credit to Checking:Restricted Fund A the balance in that account, Debit to Checking Parent account, same amount.

Credit to new equity accounts Temporarily Restricted Net Assets, subcategory Fund A. Debit to Unrestricted Net Assets account.

Repeat for each subcategory account."

In as much as moving the funds from the bank sub account to it's parent is reasonable, and creating an equity TRNA account is reasonable to accumulate funds, the other side of the equation moves a negative into the UNA account. First, is this the default account created by QB? In any case the UNA is decreased and the TRNA is increased. Is there an expectation the UNA already had the funds there?

For this answer to this question: "Still a little unclear if there needs to be continuous transactions into the Net Asset accounts."

You have to Ask Your Accountant. They are the person directing you to do this in the first place, so no one on the internet can answer for them and their expectation from you, and your response to them might now be better informed. Have you considered running Balance Sheet by Class to show them that what they want to see, you can show them with your current method?

"The following direction has been made to utilize NA accounts instead of bank subaccounts for restricted and unrestricted assets:

"Journal entry to eliminate sub category bank account balances." "

In your real file, all you needed to do is Merge the accounts together. Remember the issue of Unbalanced JE by Class; the Church Accounting Guide had these errors. No matter what I review, there seems to be some sort of usage error in every concept, but they seem to have different errors, so it helps to review lots of them. I teach this in class: Review 5 videos for that same task. If 3 agree, that might be the best method for you, but try it and then run your own reports, to see if you like the results."

"Repeat for each subcategory account."

Merging works just fine, too.

"In as much as moving the funds from the bank sub account to it's parent is reasonable"

But you won't do this unless you intend to eliminate the subaccounts be Merging, anyway. You never post to a Parent level account when there are Subaccounts, because the Parent is used only to reconcile and nothing should be posted there directly. That creates "- Other" in reporting.

"First, is this the default account created by QB?"

As I previously described, find the Equity account that does Not Open as a register view when you double-click it. That is the one QB makes and uses; you get to Name it to meet your needs. For instance, if nearly everything your organization does is Restricted, Name this Restricted.

"In any case the UNA is decreased and the TRNA is increased. Is there an expectation the UNA already had the funds there?"

If the entity has prior year data, there is Prior Year RE, by definition. It might have been allocated into various other Equity accounts, but any/every activity contributes to Equity.

Many thanks for your responses to my queries. I continue to review our communications. The accountant and we have ended the relationship so I am moving forward.

A separate but linked question having to do with the use of and reporting of a temporarily restricted donatiion physically received in the month prior to the start of our fiscal year but intended soley for use in this fiscal year for one specific purpose. The grant was recorded as income in the previous fiscal year (maintained in a bank sub account) and of course expense accounts are debited as used in this fiscal year. The periodic Statement of Financial Position show the reducing fund balance but I have not been able to figure out how to show on the statement of activities (I&E) an income from the TR fund to balance out the expenses (in this case those of a specific employee's compensation). Is it possible to use the previoius fiscal year's Net Assets (which I have yet to determine how to accurately separate the Unrestricted and TR Net assets - a different question ), debiting the NA and crediting an account, "Release of TR funds"?

Thanks, in advance.

You have clicked a link to a site outside of the QuickBooks or ProFile Communities. By clicking "Continue", you will leave the community and be taken to that site instead.

For more information visit our Security Center or to report suspicious websites you can contact us here

{kind=link}

{kind=link}

{kind=link}

{kind=link}