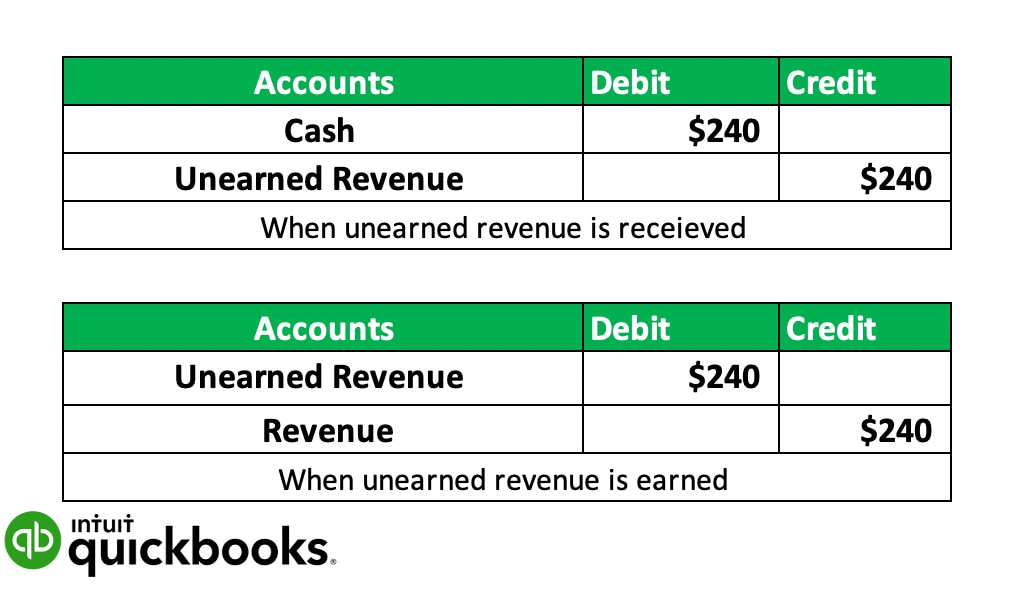

Unearned Revenue Journal Entry

When a customer prepays for a service, your business will need to adjust the unearned revenue balance sheet and journal entries. Your business will need to credit one account and debit another account with corresponding amounts, using the double-entry accounting method to do so.

Unearned revenue should be entered into your journal as a credit to the unearned revenue account, and a debit to the cash account. This journal entry illustrates that the business has received cash for a service, but it has been earned on credit, a prepayment for future goods or services rendered.

Once the goods or services are rendered, and the customer has received what they paid for, the business will need to revise the previous journal entry with another double-entry. This time, the company will debit the unearned revenue account and credit the service revenues account for the corresponding amount.

You will, therefore, need to make two double-entries in the business’s records when it comes to unearned revenue: once when it is received and again when it is earned.

Look below to see an example of the two journal entries your business will need to create when recording unearned revenue. Taking the previous example from above, Beeker’s Mystery Boxes will record the transactions with James in their accounting journals.