Turn on suggestions

Auto-suggest helps you quickly narrow down your search results by suggesting possible matches as you type.

Showing results for

I have Quickbooks desktop Pro 2016 and I created a profit and loss report. when I clicked into my cost of goods sold balance I see that the credits I received from my vendor is included in my Cost of Goods Sold account as a plus to my balance and not as a deduction. Has anyone had any experience with such a case?

Hello there, @Ruthy Vos.

Thanks for reaching out to us. I'm here to provide some information about how Vendor Credit shows on the P&L report.

The amount for the Vendor Credit would likely to add on your COGS balance if it isn't applied as payment to a Bill. This means, you still have an outstanding credit that you can apply to a future Bill. Please see attached screenshots below for your references.

This should provide you information about Vendor credit posting on P&L report. Let me know how things go and if there's anything else you need from me. I'm always here to help in any way I can. Have a great rest of your day!

My credits are actually applied to bills already.

Thanks for your quick response, Ruthy Vos.

I’d love to clarify why the vendor credits are included in the Cost of Goods Sold account.

This may happen when the Cost of Goods Sold account is used for the item on the credit. You can open the transaction and item list to review the transaction.

To open the credit:

To view the Asset account:

If this is the case, change the account where you want to post the vendor credit. If you’re in the Credit window, go to the Expenses tab.

From there, click on the drop-down to change the posting account. If you're in the Item List window, go back to the item and right-click your mouse.

Once the Item window opens, go to the Asset account section and choose the correct posting account.

With these steps, the credit will no longer show in the Cost of Goods Sold.

Stay in touch if you have additional questions working in QuickBooks. I'll be around to answer them. Have a good one.

Hi and Thanks for your help.

My issue is that I entered a credit which includes items, that have an income account of Cost of Goods Sold and an asset account of Inventory Asset and nothing in my expense tab. Do I have to change any of these so that my cost of goods sold should be correct?

Thanks again

Hello, @Ruthy Vos.

Thanks for getting back to us. Allow me to loop in for a moment and help make sure that the credit you've created will show as a deduction on your Profit and Loss report.

For me to be able to provide you with the best resolution, can you please give us a screenshot of the credit you created, your Profit and Loss report, and the Asset Account of the item you selected?

Once I know this, I'll be able to work towards getting you the fastest resolution.

Looking forward to your response and providing further help.

Hi @Ruthy Vos,

Thanks for giving us a screenshot of the credit amounts showing in the P and L report. I'm here to share my insight about it.

What are the actual credit memo amounts? I've gone through this thread and you've mentioned that you set up the item with an income account of Cost of Goods Sold.

COGS is a special expense account. It is the cost of acquiring or manufacturing the products that a company sells during a period of time. Therefore, it shouldn't be associated to an income account.

When you create an inventory item, the Cost of Goods Sold account is automatically assigned in the Purchase Information section. You'll want to remove the COGS in the income account field of the Sales Information and replace it with an income account.

Here's how:

Once done, re-open the P&L report, refresh the page and review the balance of your Cost of Goods Sold account.

You should see some changes on the posting of the transactions. Be sure to touch base with me here on the results of your testing, I want to ensure this matter gets resolved.

Wishing you and your business continued success this 2019!

Yes, if you Return something, it is Negative to the original account. Sales will be positives to COGS for inventory assets and for purchases that are directly posted as COGS, such as Noninventory items. Returns are "negative expense" and that is Negative in COGS, for this reason. It Reduces the total in COGS.

This is strange, though: "that have an income account of Cost of Goods Sold and an asset account of Inventory Asset "

The COGS is backwards and that would be your problem. Edit your items, Fix the account link, and let QB move existing data for you.

Income is Sales Revenue. Cost or Expense is COGS, and Asset = where it is held when you first bought it. That is only for Inventory item = three account links.

Two Sided noninventory items are Expense when you buy it = COGS, and Income when you sell it.

Thanks so much for your constant support it's greatly appreciated.

I went ahead and changed all my inventory to an income account of Sales Income instead of Cost of Goods Sold. However unfortunately nothing has change on the end of the P and L report even after I refreshed it.

See the attached credit memo for the first example I attached before.

Looking forward for your assistance again.

Let's review Basics. First, inventory flows like this:

Buy it = Inventory Asset value in stock

Sell it = Gross Revenue as income; plus the QB program removes that Carried Cost or Basis from Inventory Asset and puts it to Cost of Goods Sold, because now that it is sold, you no longer have it on hand. This also reflects that the Income minus the COGS for this Dated Sale = this is when Profit is computed, with this info.

When you Remap the item links, you need to accept the program's offer to Move Existing Data. That should have fixed the P&L, in that you have Credits to COGS (negatives) because they should have been Credits to Income. This means the Sale is Increasing COGS and Increasing Income. This remapping should have removed the Negative entries from COGS and left Positives there.

Meanwhile, the opposite or Mirror image of Buying something from a supplier = Returning it. That means Inventory Asset goes down (you no longer have what you had). COGS should not be impacted at all, because this simply is a Removal of Inventory Asset on hand.

The opposite or Mirror image of Selling something to a customer = Returning it to you. That means you just 'lost" the sale, so Income is going to show a negative for the value on the Credit Memo. Since this also results in the removal from COGS, the COGS account is going to show Negative, as well. Remember that the user of an inventory item on a customer return implies you got it Back into stock. That means 3 things are happening" sales income is reversed, COGS expense is reversed, and the Inventory Asset just got back that item with a value. So, in this example, Customer Return = COGS and Income both just got a negative amount and reduced Income on the P&L and reduced COGS on the P&L.

That's what you are Supposed to see. What you were seeing, seemed backwards.

I didn't totally get you.

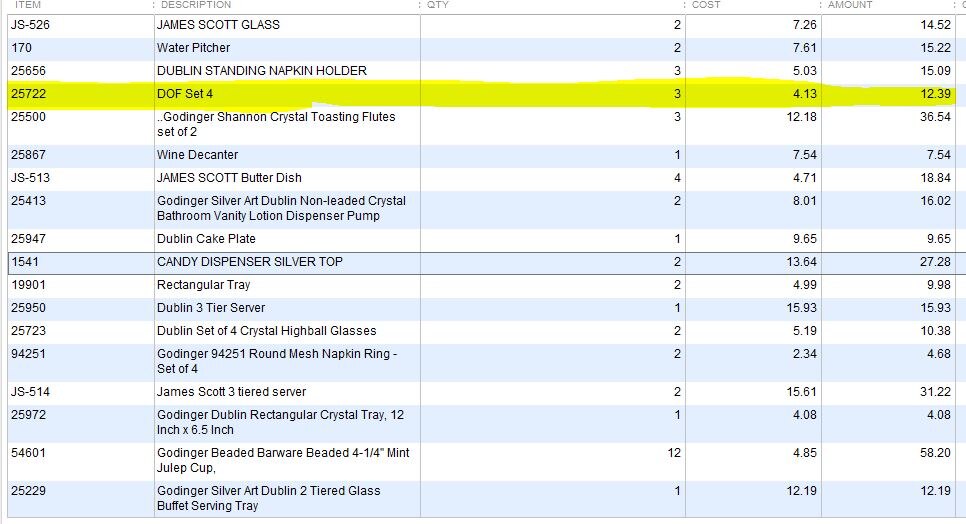

This is not a customer return it's a credit from the vendor for damaged items. As you can see on both attachments from this item 25722 DOF set of four we were credited 3 units at $4.13 each which is a total of $12.39. While on the P and L report it comes up -.26. Why is this soooo off?

Hope you can solve this issue ASAP since I need already my reports for my accountant.

Uh, this is a problem: "Hope you can solve this issue ASAP since I need already my reports for my accountant."

You are On the Internet. This is a text-based peer user community and not Tech Support, Accounting Support or Program training.

We do our best to help you understand what you tell us you see and what you show, and I completely understood that this is Vendor Credit. You used the phrase Credit memo, which is Customers. Vendor Credit is Vendors. I explained Both types of credits from the perspective of how the data flows and what you should expect to see.

Next, it depends on if the Item is inventory or not. For Inventory, a Vendor Return simple removes the Asset Value from inventory and never hits COGS at all. For @VivienJ reference: You don't put the entry as Expense to COGS; you use the Item on the Items tab details.

You told us these details, which is Wrong, and we addressed it: "which includes items, that have an income account of Cost of Goods Sold and an asset account of Inventory Asset and nothing in my expense tab. Do I have to change any of these so that my cost of goods sold should be correct?"

In Edit Item, Inventory is Asset, bottom left, when first purchased, Sales Income right middle when sold, and COGS as the Expense, left middle side. If you did not Relink your items and let QB move the existing data, this explains why COGS is wrong.

I really appreciate your time and effort even though you're not a technical support agent.

You wrote "If you did not Relink your items and let QB move the existing data, this explains why COGS is wrong." How do I reling my items?

Would relinking help that QB should generate an accurate report?

Next you wrote "Next, it depends on if the Item is inventory or not. For Inventory, a Vendor Return simple removes the Asset Value from inventory and never hits COGS at all. For @VivienJ reference: You don't put the entry as Expense to COGS; you use the Item on the Items tab details." This is actually inventory items. If it doesn't have to hit COGS only decrease assets then why isn't it so? As you saw on my attachments I do have my vendors credits coming in by COGS.

Isn't this awfully wrong?

"Would relinking help that QB should generate an accurate report?"

Yes, you Edit and relink them to the right account and when you try to Save that change, QB offers to Move existing data for you. Example: Everything you sold, where the Income link was COGS (backwards), you link it to income for the Sales account, the program offers to Move the existing data, you let it do so, and it Sorted Out your data; It moved Income to Income.

"Next you wrote "Next, it depends on if the Item is inventory or not. For Inventory, a Vendor Return simple removes the Asset Value from inventory and never hits COGS at all. For @VivienJ reference: You don't put the entry as Expense to COGS; you use the Item on the Items tab details." This is actually inventory items."

Which is why you Never Post to COGS manually and directly. You are supposed to list the Products. That's the point of Inventory = the Names are controlling the data file, and values, on every financial transaction. You don't post to Inventory manually if you bought 50 widgets; you list that you bought quantity 50 of Widgets, by name. That's what managing Inventory using Inventory items is all about.

"If it doesn't have to hit COGS only decrease assets then why isn't it so?"

Inventory asset goes Up when I bought 50 Widgets. It goes Down if I return them. That is All that is happening here. It't not an issue of "doesn't have to hit COGS" but an issue of is not supposed to hit COGS. That is an Error.

"As you saw on my attachments I do have my vendors credits coming in by COGS."

And that is an Error, for either purchases or returns of inventory products, where you are using QB and inventory Items. That is an Error and indicates bad setup or data flow or posting Manually on the Expenses tab when you need to list the Item. Remember, you told Us, this is inventory Items.

"Isn't this awfully wrong?"

I see a lot that is very wrong.

I've got the issue solved regarding my credits and non of them are coming up under Cost of Goods Sold anymore.

What is supposed to come up?

Doesn't all my vendor bills need to come up too?

Would appreciate if you can help me out again.

Thanks in advace

Go to Edit menu > Preferences, Reports & Graphs on the left, Company Preferences tab on the right, the Format button on the right, the tab for Fonts & Numbers, checkmark Negatives as Bright Red.

"What is supposed to come up?"

The actual data from the events, is supposed to show, and show properly.

"Doesn't all my vendor bills need to come up too?"

Top Left of your reporting, you need to be running Accrual Basis; that default setting is in the same place as you found the Format button.

Run the P&L Detail and the Balance Sheet Detail. Customize the two reports and select to see Item, from the Display tab.

Here's what you see, far left = Transaction Types.

Here's what you expect to see for the value data:

Buying inventory, using Check, Bill, Credit Card Charge = positive value into inventory asset and the Item is listed on each row (transaction details), because you Specify what you just bought, such as my example of 50 Widgets, By Name. Nothing here hits the P&L.

Returning inventory using Bill Credit or Credit Card Return = negative value reducing inventory asset and the Item is listed on each row (transaction details), because you Specify what you just returned, such as my example of 50 Widgets, By Name. Nothing here hits the P&L.

Adjusting inventory for waste = transaction type is Inventory Adjustment and you control if that increased or decreased inventory and you control the offset account. Example: I just discovered all of those widgets got damaged in a flood, so I reduce inventory for them, and now I see a negative Inventory Asset value and the offset is the Waste Expenses account, that will be this same transaction on the P&L as Positive value for that lost value as Expense.

Selling inventory using invoice or sales receipt: Inventory asset is Negative value; COGS and Income on the P&L are both Positive values. All of this happens from that one invoice number or sales receipt number = three accounting events. Inventory went Down, because I sold the 50 widgets. Income goes up by my Price that I just sold them for. COGS goes Up, for the Average Cost on Hand, which in this case would be All of them.

Thanks Loads for getting back to me.

You wrote that Bills shouldn't effect my P and L report and shouldn't even come up there.

However, the bills that I entered without a Purchase order I do see coming up on my P and L report,while all other ones that I first entered as a PO, then receipt and then the bill, aren't showing.

Is this an issue?

Could this be making a mess?

It's good to see you here again with us, Ruthy Vos,

Let me help share information about the transactions affecting Profit and Loss report.

Upon creating a Bill and assign it to an expense account, it will reflect in the Profit and Loss report. Also, when you make a Bill Billable then created an invoice.

However, when creating Purchase Order using items then created a Bill, it will not affect your accounts in any way.

For proper guidance, it would also be best to contact your Accountant.

If there's anything else I can do for you, please feel free to reach back out. Have a great day!

You wrote: "Upon creating a Bill, when you make it Billable and use an account under Cost of Goods Sold, it will really affect Profit and Loss report." How can I see if I used an account under cost of goods sold? If that's the case, how can I change it?

Then you wrote: ".......it will only affect Profit and Loss report once you'll convert it into a Bill or an Invoice. I'm talking about bills that were converted from PO that do not show up under Cost of Goods Sold. Where could they have gone?

Wrote the part about Posting to COGS directly, showing the image where COGS is listed on the Expenses tab. That is an Error for inventory management.

You Don't Want to do it that way. I explained that if you are managing inventory using QB Inventory Item Names, you need to list the actual Products on the Items tab. Recall my example of 50 Widgets. The Item Names need to control the flow for the accounting.

"How can I see if I used an account under cost of goods sold?"

Open any Bill or Check or Credit Card Charge that you know paid for Products that you manage as Inventory items. Make sure the Items are listed on the Items tab.

"If that's the case, how can I change it?"

You can delete entries from the Expenses tab and put the right info on the Items tab. As long as the transaction is the right amount, nothing about the Value changed.

"Then you wrote: "

Is giving Bad Guidance or Incomplete Details.

".......it will only affect Profit and Loss report once you'll convert it into a Bill or an Invoice."

Not the Bill. Yes, the Invoice. As I explained, selling Inventory will then result in Two Parts hitting P&L: Gross Sales Income and "cost on hand" from Inventory now showing in COGS. This is how you see that Profit has occurred: income minus your cost = profit because of the sale of the inventory and not because of the Purchase of inventory.

"I'm talking about bills that were converted from PO that do not show up under Cost of Goods Sold. Where could they have gone?"

If the Items on the PO are inventory, they "went" into Inventory Asset. They resulted in Quantity on hand increasing and Basis or Cost on hand is Added, because your bought More.

You listed Items on the Purchase Orders. If these are Inventory Type, you are buying more Assets.

Think about this: money in the bank is my Asset. If I use it to buy Stuff that then is on hand, that still is Asset. I changed Money asset for Inventory Asset.

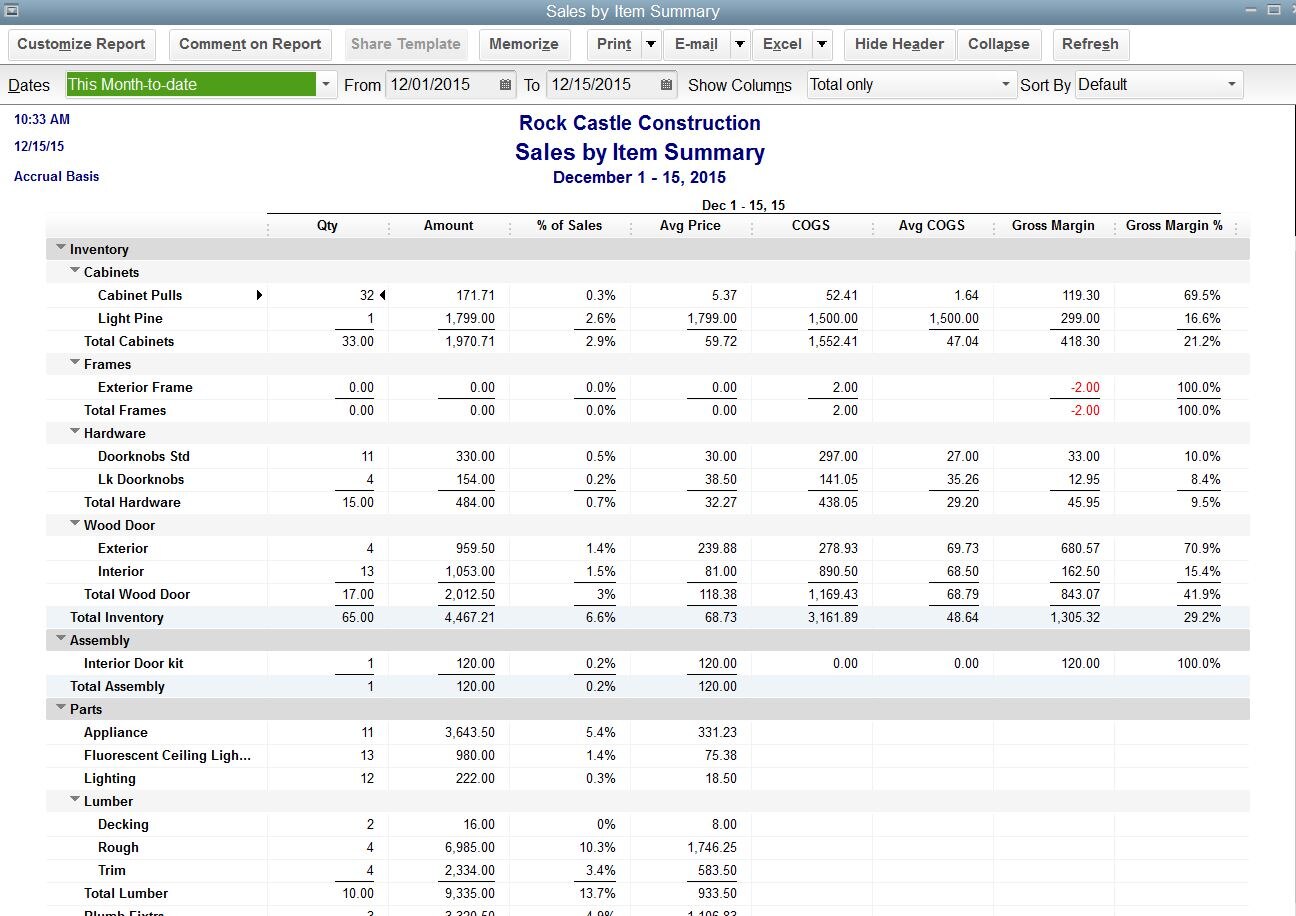

Don't you have a CPA that can help you learn about the financial tracking, data flow, and reporting to use? Did you run your Inventory Valuation or Stock Status reports, for the date you bought new stuff, and the date you sold stuff? Have you run your Item Profitability reports? Sales By Item Summary?

Please see my attachment.

You have clicked a link to a site outside of the QuickBooks or ProFile Communities. By clicking "Continue", you will leave the community and be taken to that site instead.

For more information visit our Security Center or to report suspicious websites you can contact us here

{kind=link}

{kind=link}

{kind=link}