Turn on suggestions

Auto-suggest helps you quickly narrow down your search results by suggesting possible matches as you type.

Showing results for

BLACK FRIDAY SALE 70% OFF QuickBooks for 3 months* Ends 11/30

Buy nowSolved! Go to Solution.

I have been entering my bills in QB and applying the inventory to COGS-COGS account. ... At no point does the P&L or Balance sheet note the value of the inventory assets that were not sold and remain on hand to be sold. ... Also, throughout the month I have to write off inventories due to damage or shrink.

Then you are expensing the full amount of the purchase and there will not be an inventory asset value on the balance sheet.

And since you are expensing the purchase, there is nothing to adjust either.

Since you are not using QB inventory, you must use the periodic inventory method. There are two ways to do periodic inventory, choose one and stick with it, you can not mix and match

1. Create an asset account called purchases and post all purchases of item for resale to that account. Periodically, weekly, monthly, etc value the inventory on hand, subtract that value from the amount shown in the purchases account and do a journal entry for the answer to the subtraction

debit COGS for that value

credit purchases for that value

OR

2. Post all purchases to COGS. Periodically, but at least at the end of the year, you value the inventory on hand and do a journal entry.

debit the asset purchases account for that value

credit COGS for that value

Print the P&L

then reverse the journal entry

debit COGS for that same value

credit the asset purchases account for that value

This last journal entry, moves the value of what was on hand at the end of year back to COGS so the cost will be counted against the new year sales.

I have been entering my bills in QB and applying the inventory to COGS-COGS account. ... At no point does the P&L or Balance sheet note the value of the inventory assets that were not sold and remain on hand to be sold. ... Also, throughout the month I have to write off inventories due to damage or shrink.

Then you are expensing the full amount of the purchase and there will not be an inventory asset value on the balance sheet.

And since you are expensing the purchase, there is nothing to adjust either.

Since you are not using QB inventory, you must use the periodic inventory method. There are two ways to do periodic inventory, choose one and stick with it, you can not mix and match

1. Create an asset account called purchases and post all purchases of item for resale to that account. Periodically, weekly, monthly, etc value the inventory on hand, subtract that value from the amount shown in the purchases account and do a journal entry for the answer to the subtraction

debit COGS for that value

credit purchases for that value

OR

2. Post all purchases to COGS. Periodically, but at least at the end of the year, you value the inventory on hand and do a journal entry.

debit the asset purchases account for that value

credit COGS for that value

Print the P&L

then reverse the journal entry

debit COGS for that same value

credit the asset purchases account for that value

This last journal entry, moves the value of what was on hand at the end of year back to COGS so the cost will be counted against the new year sales.

"such as outdated milk that is thrown out"

For something with a short life, there is no reason to track this purchase as Inventory. The products such as milk and fresh produce that spoil quickly if not sold, or are sold soon, they might as well be posted as Purchases of COGS and not held as inventory at all.

You might as well make it easier on yourself and not track things as Asset on hand, when that will require micromanagement from you.

Asset value is meant for the value of stuff "on hand over time" so that the Sale is not a long time period after the entry as expense. For milk and other "quick turnaround" products, just post them to COGS directly.

Sorry to be so slow, but I am still trying to figure out how to deal with inventory as an asset. I sell wine. I buy a container of wine at a time. I pay a price for that wine that I had been registering as a COGS. But the value of the asset that I own the moment I buy it is actually the price at which I will sell it--not the price I paid for it. If there is a way I can assign that value somewhere, then as I sell the wine I can subtract, thereby decreasing the value of the asset. I am definitely not a financial person, but that logic makes sense to me. First--is it correct? Then second, if so, how do I properly record everything in QB?

Thanks!

Thanks for joining the conversation, @traviswine,

I can add a bit more about the inventory management in QuickBooks Desktop and how it affects the Inventory Assets and COGS accounts.

When you set up the inventory item you have the option to enter the item Cost. Here's how:

QuickBooks uses the weighted average cost to get the value of your inventory and the amount debited to the COGS account once you sell your inventory. You can check this article to know more about inventory tracking: Understand Inventory Assets and COGS tracking

Let me know if you have any more question about inventory management. I'll be glad to help. Have a good one!

I am trying to correct the COGS from last year for a company but I am not sure of the best way to do it. At the beginning of the year all purchases for resale were being recorded directly to COGS. In May someone decided to set up the inventory tracking system in Quickbooks, and recorded beginning inventory balances to the inventory asset account. For the rest of the year, the COGS was automatically recorded with each sale as the inventory asset account was simultaneously reduced. The problem is that by year-end the COGS balance is artificially high. Staff did do an inventory count at year-end, and I made adjusting journal entries to correct the inventory asset account balance. This did reduce the COGS slightly, but the amount is still too high based on the amount of sales that occurred before inventory tracking was set up in May. I need to make another adjustment that does not affect the inventory asset account, as that balance is actually correct.

Hello – We had a bunch of negative (and some positive) inventory that is being adjusted.

It’s a mix of mistakes of sales receipt errors, item receipt errors, etc.

Anyways, if we “correct” these through an inventory adjustment, it really skews the cost of goods. Is there a way to offset or zero out that adjustment so that it doesn’t show a profit or loss?

I appreciate you joining the conversation, @NateP.

The inventory adjustment will ensure you're correctly tracking your items in QuickBooks. As long as you've posted the adjustment to their proper accounts, your inventory status report will show accurate tracking of your inventory quantities.

To ensure you track your COGS correctly, you can check out this article for more information: Adjust your inventory quantity or value in QuickBooks Desktop.

However, if you need to offset your adjustment, I'd recommend reaching out to your accountant first. This way, your accountant can decide which accounts to use to properly track your inventory.

If you have additional concerns, let me know by leaving a comment. I'll be ready to pop-in and help.

Thanks. I have an inventory adjustment account that is an expense account. I’ve also tried using a CoGS account for inventory adjustments. They both affect profit statements. The issue is that these are mostly drop ship items that we ever physically had in stock. For example, a customer cancelled his order, but there was a sales receipt made for his order that never got canceled (customer never got charged/billed either). This sales receipt goes unnoticed for months. Anyways . . . It’s a challenge and I’ll see what my accountant says.

Rustler,

I'm in need of a little more clarification for a client of mine. I've done the three part transaction for furniture purchases, i.e.

Purchase

dr-inventory

cr a/p

Sale

dr: Cash

cr: COGS

Inventory adjustment

dr: COGS

cr: Inventory

Client is saying that I need to have recorded this in a way that the sales of products(Furniture) should not show in sales. Am I missing something here? There is no way to do that, correct? The COGS will adjust his gross profit; however, we have a GL Audit coming up and client doesn't want gross sales to show the furniture sales...

Hello--I noticed that my current inventory have been adjusted. I'm not sure how this occurred, the only explanation I can think of is when I was adding the expense/item for this inventory which probably caused the additional inventory quantity. My questions are below.

1) Should I enter the Expense/Items first before entering a new product in the Product and Services section?

2) Before I adjust my inventory quantity, how do I make this adjustment without affecting my Inventory Shrinkage account?

Hello @Jshoplist,

You'll need to create the item first to enter a transaction or enter an initial purchase of the item. Let me guide you how.

After entering the quantity (On Hand), you'll no longer need to use the inventory adjustment. This also applies when you create the purchase transaction of the item manually. Please see this article for more information about adjusting your inventory quantity or value in QuickBooks Desktop.

In case you encounter negative inventory, please check this article for details: Fix negative inventory issues in QuickBooks Desktop.

Feel free to comment anytime if you have other questions or concerns. I'd be around to help. Thanks for jumping in and have a wonderful day.

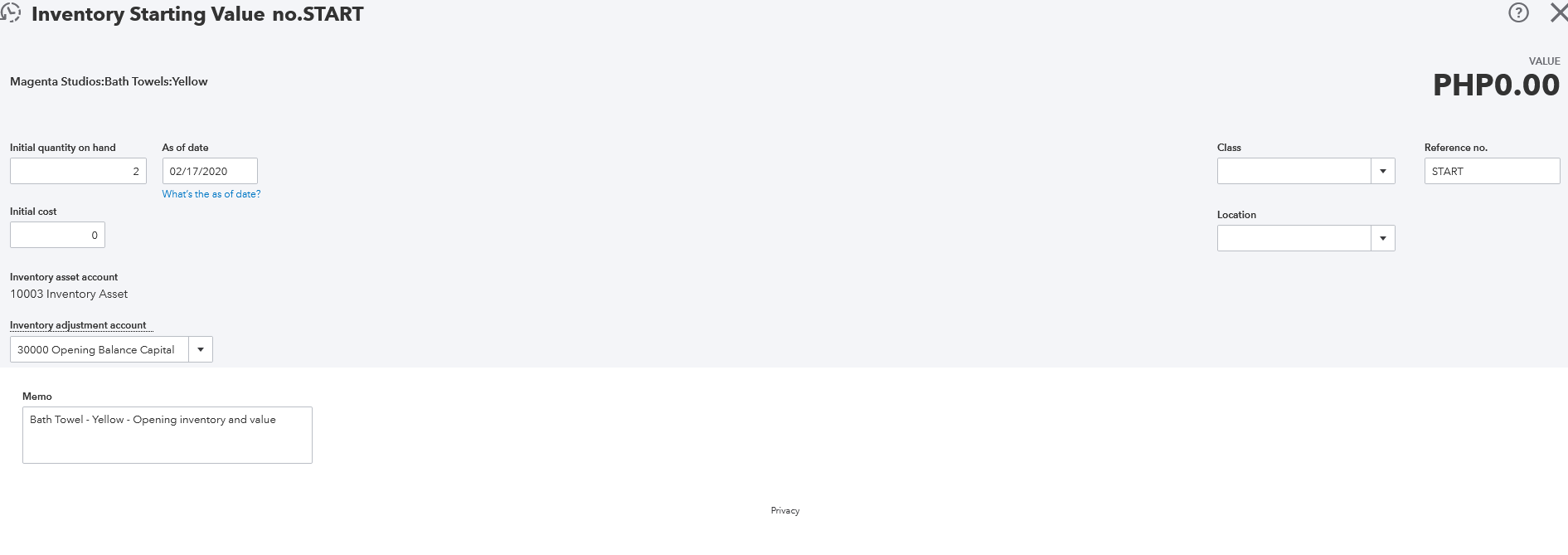

Below is a screenshot example of the inventory. What I did was 1) Enter the inventory items from Lists/Products and Service then 2) Entered the expenses from Expenses/Expenses/Items Details. By doing this, it looks like it duplicated my inventory. How should I be entering my inventory items without making this same error? Also, how do I fix this? Thanks.

Attached is an example report of my inventory. What I did was 1) Entered the products via Lists/Products and Services and then 2) Entered the expense via Expenses/Expense/Item Details. By doing this, I think it duplicated my items. How do I fix this and what should I do so that I do not make the same error next time?

Let's correct the count of your inventory, Jshoplist.

The screenshot shows that you’re using the QuickBooks Online version, so we’ll base our steps on this platform.

You can create inventory items with a zero starting quantity. When you purchase them, you can record a vendor transaction with the items, and this will increase their counts. However, if you have items on hand before starting your business, you'll enter the quantity the moment you create them in QuickBooks.

The bottom line is you only want to enter a quantity on hand if you won't need to record your inventory purchases.

To correct the count, you can edit the items and update the Starting value.

By default, the affected accounts in this adjustment are the Inventory Asset and the Opening Balance Equity accounts.

You can run the Inventory Valuation Detail report after correcting the initial value.

Feel free to reach back out if you still need with your inventory items.

Hi Jshoplist,

Entering a bill or expense transactions add the quantity on hand of your items. You'll want to edit the quantity of the items. Then, enter an invoice so it will deduct from your product and services quantity on hand.

Here's how:

Moving forward, create an invoice if you want to be deducted from your product and services quantity on hand. Please check this article for the detailed steps: Create Invoices in QuickBooks Online.

You can also track inventory that you're donating, please check this article for more information: Track Donated Inventory.

Feel me in if you have any other concerns. I'm always right here to help.

Hey Jshoplist, If I'm reading your posts correctly the total quantity should be 2 not 4? If so the reason you're having this problem is that you made the initial quantity 2 and then added 2 more with the expense/purchase. If you are going to enter the 2 through the purchase then your initial quantity needs to be set at 0. If you edit the inventory item look under "Quantity on Hand" there should be a clickable "starting value" click that and adjust your starting quantity to 0. Then every time you purchase that item and expense it it will add more inventory.

Hope that helps.

Can you help me with how set up inventory mid year in desktop. Client has been putting all purchases to Cost of Goods and now wants to start tracking.

Thanks,

Alice Burnett

[email address removed]

I’ve been doing inventory like your option 2 for years, but recently we are having difficulties matching the books and we believe is because we haven’t adjusted the inventory for loss items. How should I make that entry properly?

You have clicked a link to a site outside of the QuickBooks or ProFile Communities. By clicking "Continue", you will leave the community and be taken to that site instead.

For more information visit our Security Center or to report suspicious websites you can contact us here

{kind=link}

{kind=link}

{kind=link}

{kind=link}