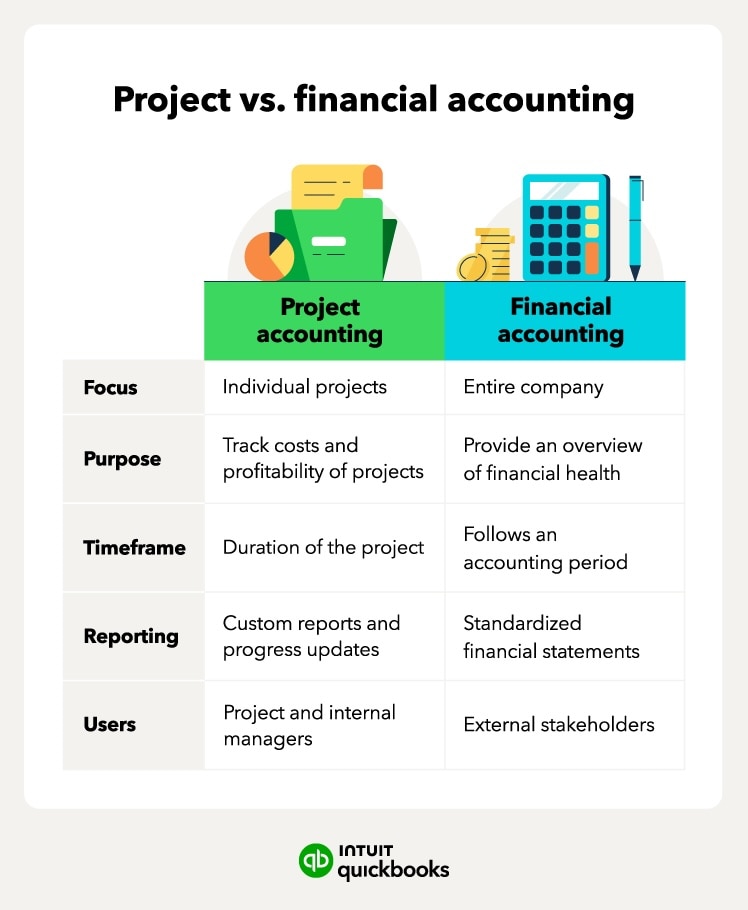

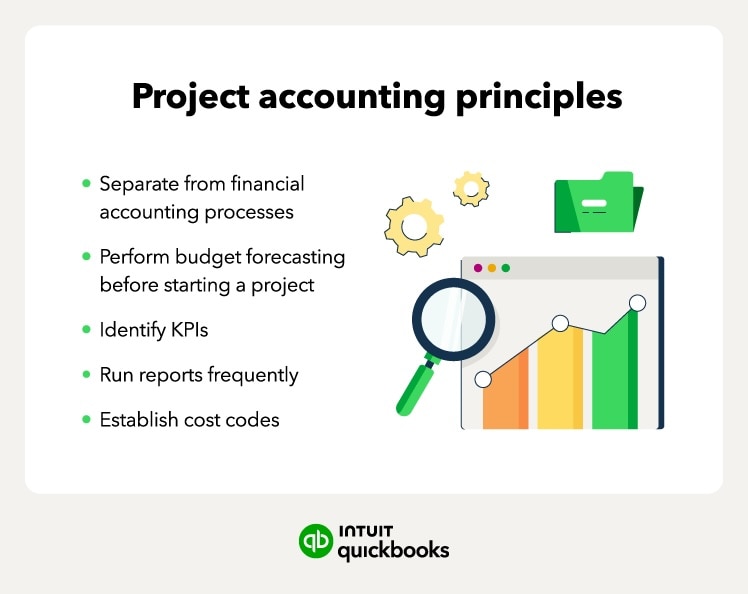

Job costing

Job costing involves detailed estimates of material quantities, labor hours, and equipment usage in construction. By comparing these estimates to actual costs throughout the project, you can identify variances and make adjustments as needed.

Estimate, track, and analyze all project costs, including your direct and indirect costs. Direct costs include labor, materials, and equipment, while indirect costs cover overhead and administrative expenses. To set a realistic budget and timeline, you should try to account for every cost you might incur.

Project forecasting

Based on your current data, project forecasting helps you predict future costs, forecast revenue, and estimate timelines. Project forecasting helps project managers prepare for potential challenges and determine how best to keep things on track. Like project costing, this is an ongoing process, and you should update it regularly when data becomes available.

For example, project forecasting was especially important during the pandemic when bottlenecked supply chains caused delays in material deliveries. In addition, the materials themselves became more expensive. With project forecasting, construction companies were better prepared to adjust their budgets accordingly.

Resource management

Resource management can help you save time and money on your project. By using labor, materials, and equipment efficiently, you can better ensure that resources are allocated effectively, reduce waste, and minimize delays.

On a construction site, resource management may involve scheduling workers in shifts to help ensure the project progresses steadily without downtime or bottlenecks. You may also have time blocks to be mindful of. For example, if you’re repaving a busy road, you might be limited to late nights and weekends and must plan to use your resources accordingly.

Revenue recognition

Revenue recognition refers to when and how revenue from a project should be recognized in your company’s financial statements. You’ll usually receive payments in stages for long-term projects like a new office complex. Identifying what these stages are will help you budget for them.

You may recognize revenue during each completed milestone, like finishing the foundation or installing the roof. When done well, revenue recognition ensures that your company’s financial statements accurately reflect the project’s progress and economic health.