You could save up to 25% on transaction costs².

Speak with us now to see if you qualify.

Talk to sales 1-800-515-8366

Monday - Friday, 6 AM to 4 PM PT

Table of contents

Table of contents

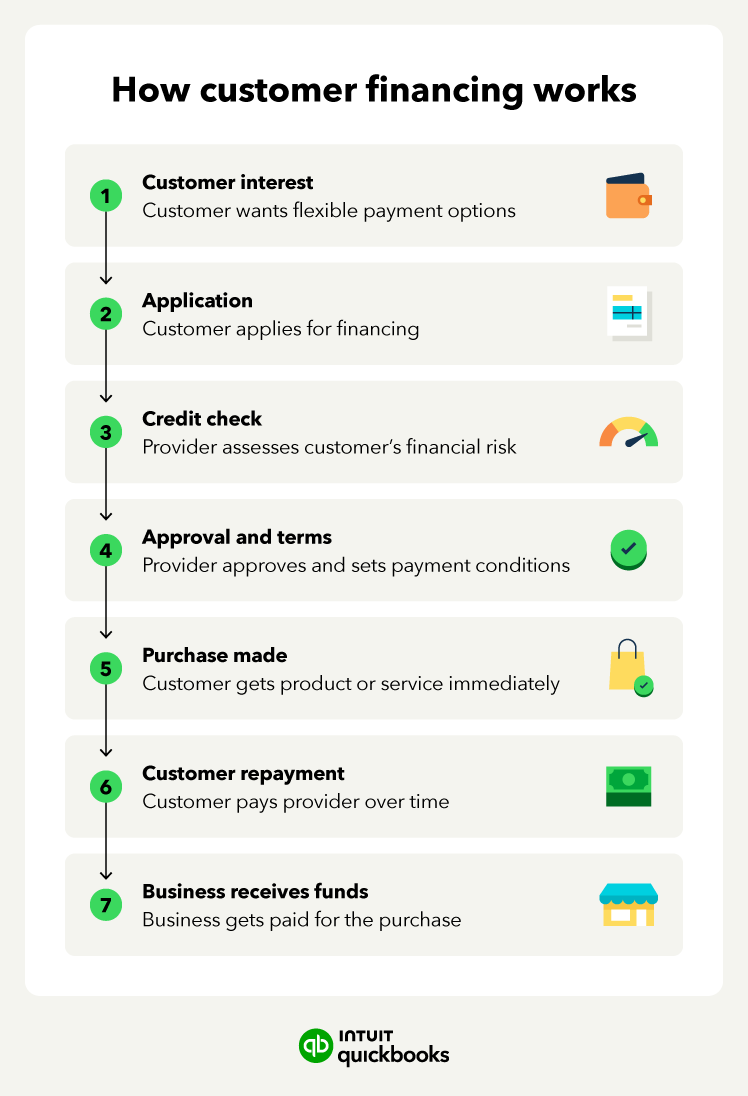

When a customer wants what you're selling but can't pay in full, you lose the sale. Customer financing changes that. It lets your customers pay in installments instead of upfront, spreading the cost over weeks, months, or years.

This doesn’t mean you have to wait to get paid. Instead, a third-party financing company funds the purchase, paying you the full sale amount upfront, often minus a small fee. Below, find out how customer financing works and how to use it to generate bigger orders and more sales.

Customer financing is a payment option that allows your customers to pay in installments for your products and services, rather than all at once. They spread their payments over weeks, months, or longer, depending on the terms you or your financing provider set.

This is not a loan you take out to grow your business, like a commercial mortgage or equipment financing. Instead, it's something you offer your customers so they don't have to find the full amount before they buy.

Once you offer customer financing, make sure your customers know about it. Add it to your product pages, receipts, and in-store signage. Mentioning it early in the buying process, before someone walks away over price, is where it makes the biggest difference.

Offering customer financing is important because it stops you losing sales to customers who want to buy but can't pay the full amount upfront. Here's how that looks across different types of business:

Three advantages of offering customer finance:

That’s how customer financing for small businesses benefits both you and your customers.

Always calculate the fees associated with third-party providers or the administrative costs of in-house programs to ensure that offering financing will actually generate a profit for your business.

How customer financing works varies depending on the provider and type, but the basic flow from application to repayment is similar:

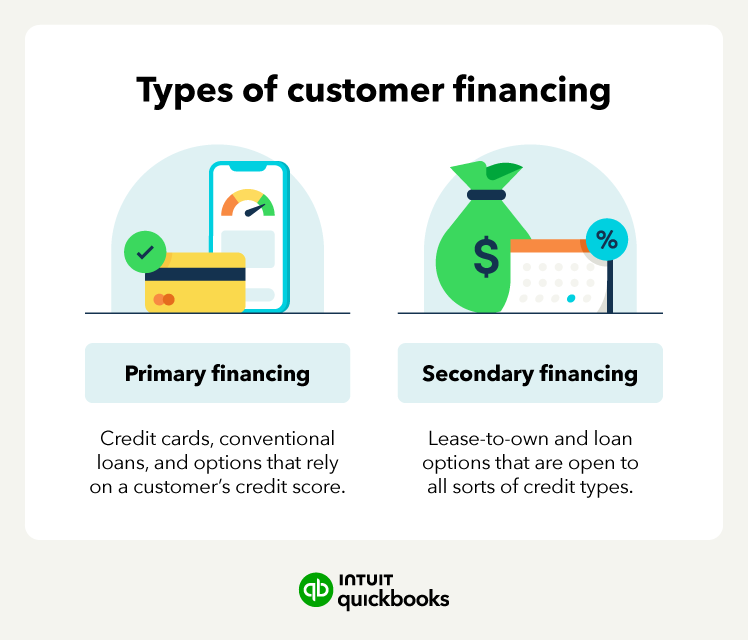

There are multiple ways to offer your customers finance, and they broadly fall into two categories:

Some give you greater control, while others take the work and the financial risk away from you.

Customer financing type: Primary

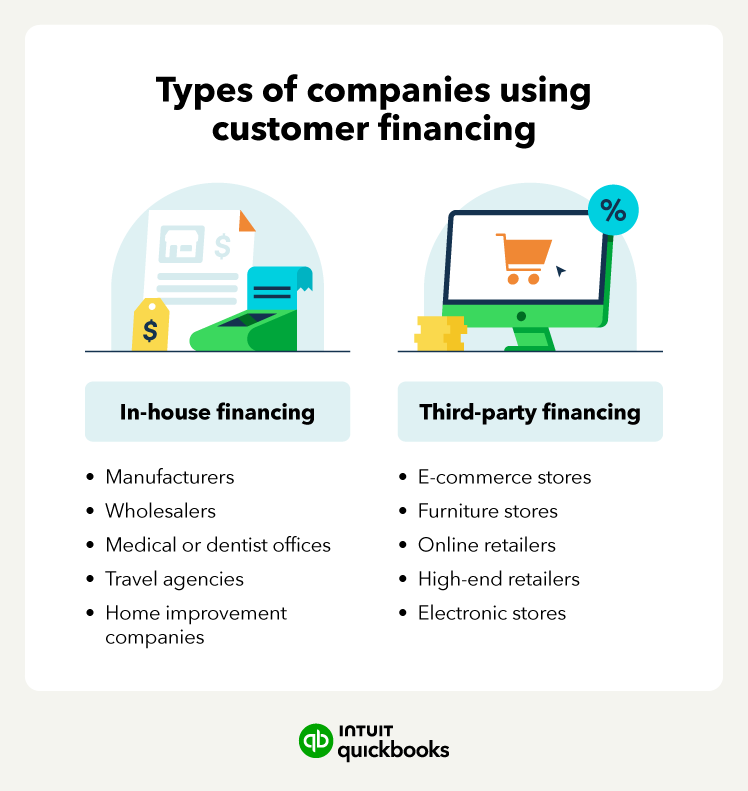

In-house finance is when a business acts as the lender and collects payments directly from their customers.

To do it well, in-house financing requires a solid accounts receivable process and the following four things to be in place:

In-house financing works well for contractors, medical or dental practices, auto repair, or businesses offering high-ticket services. There’s no provider taking a fee, and you control the terms.

The risk is that your business will have to chase money from clients who stop paying. According to the Intuit QuickBooks Small Business Late Payments Report, over half (56%) of small businesses surveyed are actively challenged with unpaid invoices, with impacted businesses holding an average of $17,500 in tied-up revenue.

If they don't pay at all, that becomes a bad debt expense your business absorbs. You also need a very healthy working capital position to manage cash flow between the time you deliver products or services to customers and the time you receive full payment.

Customer financing type: Primary

With third-party financing, a financing company handles the loan. They pay you upfront, and the customer repays the lender directly, so you're not responsible for collecting payments.

Providers typically charge a percentage of the transaction for their service, so you'll want to factor that into your pricing.

Getting set up is straightforward. Most providers offer plugins for e-commerce platforms, POS systems, and contactless payments terminals, so you can add financing to your checkout without rebuilding anything.

Third-party financing is a good idea for businesses that don’t want the administrative burden of collecting payments or the credit risk of customers not paying what they owe.

Customer financing type: Secondary

BNPL is a type of third-party financing that splits a purchase into short-term, often interest-free installments. The repayment schedule is typically four payments over up to six weeks.

Approvals happen almost instantly, and the whole process is designed to feel easy for the customer. Most providers let you add a payment link or checkout button with very little setup. The main providers are Afterpay, Klarna, Affirm, and Sezzle.

BNPL works best for lower-to-mid ticket purchases and is popular with online shoppers and younger buyers.

BNPL is a good option for an online store, a boutique, or if you want a simple financing option that requires minimal setup.

Customer financing type: Primary

Accepting credit card payments is the simplest form of customer financing. The customer pays you by card and manages their own repayment schedule with their card issuer.

Some businesses go further and partner with a card issuer to offer deferred-interest or promotional financing, like 0% for 12 months. That gives the customer an extra reason to buy now without you needing to set up a separate financing program.

This option has the lowest setup burden but also the least control over terms. It’s best suited to businesses with smaller average transaction sizes, or you don’t want to work with a dedicated finance partner just yet.

Offering customer finance can grow revenues and attract new customers, but it also comes with costs and risks, depending on the type of finance you choose to offer. Here are the main trade-offs to help you decide whether it's the right move for your business:

Offering your customers a way to pay over time can encourage loyalty and win you sales on higher-ticket items. Here's a four-step process covering how to set up customer financing and get it running.

Before you pick which type of financing you want to offer, consider:

The table below shows how in-house and third-party finance differ:

Once you’ve decided between in-house and third-party financing, you need to set it up. The route you take depends on the choice you’ve made.

If you select a third-party approach, there is a lot of competition, so shop around before you commit. Each one has its own way of operating, so compare:

You should also consider the type of third-party finance provider you want to partner with. BNPL providers like Afterpay, Klarna, Affirm, and Sezzle work well for retail and e-commerce, where the typical sale is in the low hundreds to low thousands.

Point-of-sale finance providers like Synchrony, CareCredit, and GreenSky fund bigger purchases over longer repayment terms, often with interest. They’re popular with car dealerships, dental practices, and home improvement contractors.

If you select in-house, you'll need to work everything out yourself, including:

With the terms and agreements sorted, the next step is making it visible to your customers.

Once you have your financing plan, it’s time to implement it.

Whichever route you take, offer customers as many electronic payment options as possible, like card, bank transfer, or AutoPay . The easier you make it, the more likely you’ll be paid on time.

Once the system is live, promote it. Mention financing in your email campaigns and on social media, especially when you're promoting higher-priced items. If you take payment in person, like at a physical location, add signage where people can see it as they browse, not just at the till.

At a minimum, customers should know:

The clearer you are from the start, the fewer problems you'll deal with later.

On your end, track every outstanding balance in your accounting system and follow up on late payments as they happen. If you're running it in-house, this is where having a proper collections process already set up makes all the difference.

Try offering financing on your highest-ticket items first or if a customer spends over a certain amount. You’ll find out how customers react to the offer and how much admin it creates before you roll it out further across everything you sell.

Customer financing helps you close more sales you might otherwise lose because of the price. Whether you run it in-house or through a third-party provider, the extra revenue and repeat business it generates can more than cover the cost.

If you decide to manage financing yourself, QuickBooks Online Payments lets you send invoices, collect installments, and track what's outstanding, all from one place.

Disclaimers:

*QuickBooks Payments: QuickBooks Payments account subject to eligibility criteria, credit, and application approval. Subscription to QuickBooks Online required. Money movement services are provided by Intuit Payments Inc., licensed as a Money Transmitter by the New York State Department of Financial Services. For more information about Intuit Payments' money transmission licenses, please visit https://www.intuit.com/legal/licenses/payment-licenses/.*

Call Sales: 1-800-285-4854