Since we were kids, most of us have heard our parents and grandparents talk about “saving for a rainy day.” The idea is that you need to put money aside when times are good so that you’ll have some money for when times are bad.

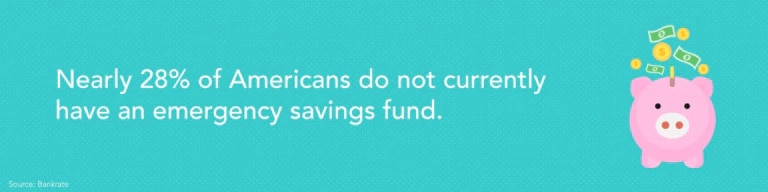

Somewhere along the line, that concept was lost on many Americans, causing savings rates to plummet. Recent surveys also indicate that nearly half of Americans would even have trouble coming up with $1,000 in the event of an emergency.

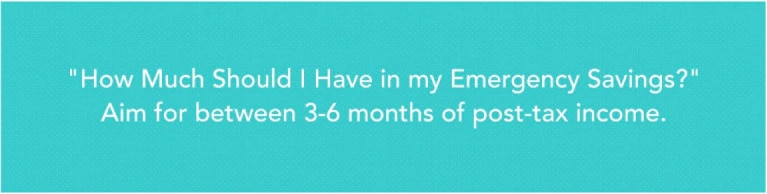

A solid emergency fund is perhaps one of the most important tools in developing and sustaining financial security. Most financial experts recommend having between three to six months of living expenses socked away because no matter how well things are going, bad things can happen from time to time.

In this post, we’re discussing what emergency funds are, why they’re useful, and, most importantly, answering important questions like, “how much should I have in an emergency fund?”. To top it all off, we’ll show you how to use our interactive emergency fund calculator to help you identify a savings goal and create a budget to get there.