What are federal withholding tax tables?

Federal withholding tables lay out the amount an employer needs to withhold from employee paychecks. This includes federal income taxes, as well as other taxes, such as Social Security and Medicare taxes.

When running a business, there are many important factors to consider, including payroll. Although setting up payroll can be a bit daunting at first, with a little guidance and preparation, you can easily navigate the process.

You'll need to gather some important paperwork and choose a reliable payroll system. One of the most important factors for running payroll is the IRS withholding tax tables for 2026, which ensures you're properly withholding taxes for your employees. The One Big Beautiful Bill Act (OBBBA) introduced several updates affecting payroll and withholding, including a higher Social Security wage base and adjusted federal income thresholds. It’s also expected to influence how the 2026 Form W-4 and withholding tables are structured. Don't worry, though—with the right resources and support, you can set up payroll smoothly and efficiently.

Jump to:

- What's new for 2026

- Key payroll tax deadlines for the 2026 payroll year

- 2026 IRS withholding tax tables

- How to use a federal withholding tax table

- How to calculate federal tax withholding

- State vs. federal withholding taxes

- What are the federal taxes withheld?

- Ways to reduce tax burden in 2025 and prepare for 2026

- Federal withholding tax table FAQ

What's new for 2026

The IRS has announced several key updates for the 2026 tax year, including inflation-adjusted brackets, standard deductions, and payroll tax thresholds. Employers should review these changes to ensure accurate withholding and compliance.

Federal income tax brackets

- Seven marginal rates remain the same: 10%, 12%, 22%, 24%, 32%, 35%, and 37%

- Income thresholds have increased to reflect inflation, meaning some employees may move into slightly lower brackets even if their pay hasn’t changed.

- Tip: Employers should review payroll to ensure withholding tables reflect the new thresholds, so employees don’t face surprises at tax time.

Standard deduction

- $16,100 for single filers or married filing separately

- $32,200 for married filing jointly

- $24,150 for heads of household

- Why it matters: A higher standard deduction reduces taxable income for many employees, which could slightly lower their withholding amounts.

Social Security wage base

- Projected to rise to $184,500 in 2026 (up from $176,100 in 2025)

- Employer impact: Employees earning above this threshold won’t have Social Security withheld on wages exceeding the cap, but Medicare withholding continues without a cap.

Payroll tax rates

- FICA rate remains 7.65% (6.2% Social Security, 1.45% Medicare), matched by employers

- Note: Medicare surtax still applies to high earners, so employers should verify additional withholding rules for employees earning over $200,000 ($250,000 for married filing jointly).

Updated withholding tables and W-4

- IRS will publish 2026 federal withholding tables in Publication 15-T

- New Form W-4 reflects OBBBA-related changes, including:

- New dependent-credit lines

- Potential adjustments for qualifying overtime and tip income (pending final guidance)

- Action tip: Employers should ensure payroll systems automatically update with the new tables and W-4 functionality. Testing early can prevent errors when the 2026 filing season begins.

Quick takeaway for employers

Even if nothing “dramatically” changed, these incremental updates affect take-home pay, reporting accuracy, and compliance. A quick payroll review now can save headaches—and potential penalties—later.

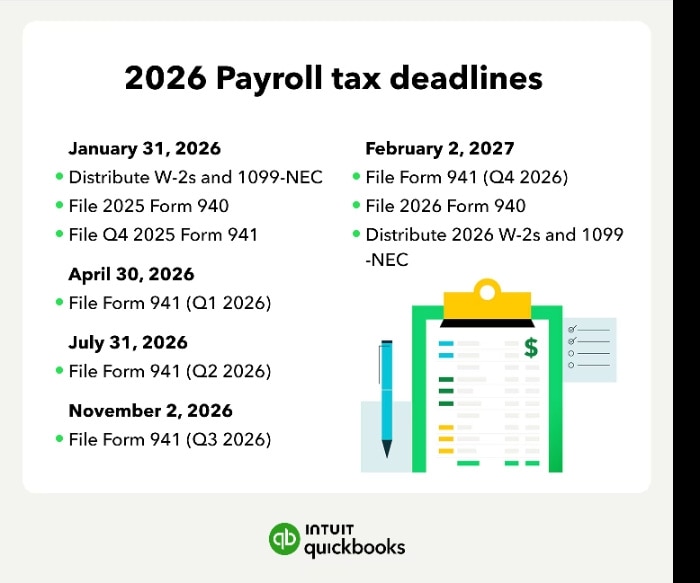

Key payroll tax deadlines for the 2026 payroll year

Keeping up with payroll deadlines is just as important as accurate withholding. Mark these key 2026 IRS payroll tax dates to stay compliant.

Start of the Year: January 31, 2026

Kick off the new year by wrapping up 2025 reporting.

- Send Forms W-2 to employees and Forms 1099-NEC to independent contractors.

- File Form 940 (FUTA) for 2025 and pay any remaining unemployment tax.

- File Form 941 (Q4 2025) if you haven’t already submitted your fourth-quarter payroll return.

First Quarter Payroll Taxes: April 30, 2026

- File Form 941 (Q1 2026) for January through March wages.

- Confirm all payroll tax deposits for the quarter are up to date.

Second Quarter Payroll Taxes: July 31, 2026

- File Form 941 (Q2 2026) for April through June wages.

- Review your deposit schedule to make sure all payments have cleared.

Third Quarter Payroll Taxes: November 2, 2026

- File Form 941 (Q3 2026) for July through September wages.

- Pay any remaining payroll taxes owed for the quarter.

Year-End Reporting: February 2, 2027

Since January 31, 2027, falls on a weekend, the deadline moves to the next business day.

- File Form 941 (Q4 2026) to report October through December wages.

- Submit Form 940 (FUTA 2026) and pay any balance due.

- Distribute Forms W-2 and 1099-NEC for 2026 to employees and contractors.

2026 IRS withholding tax tables

Here are the IRS withholding tax tables for 2026 for employers that use an automated payroll system.

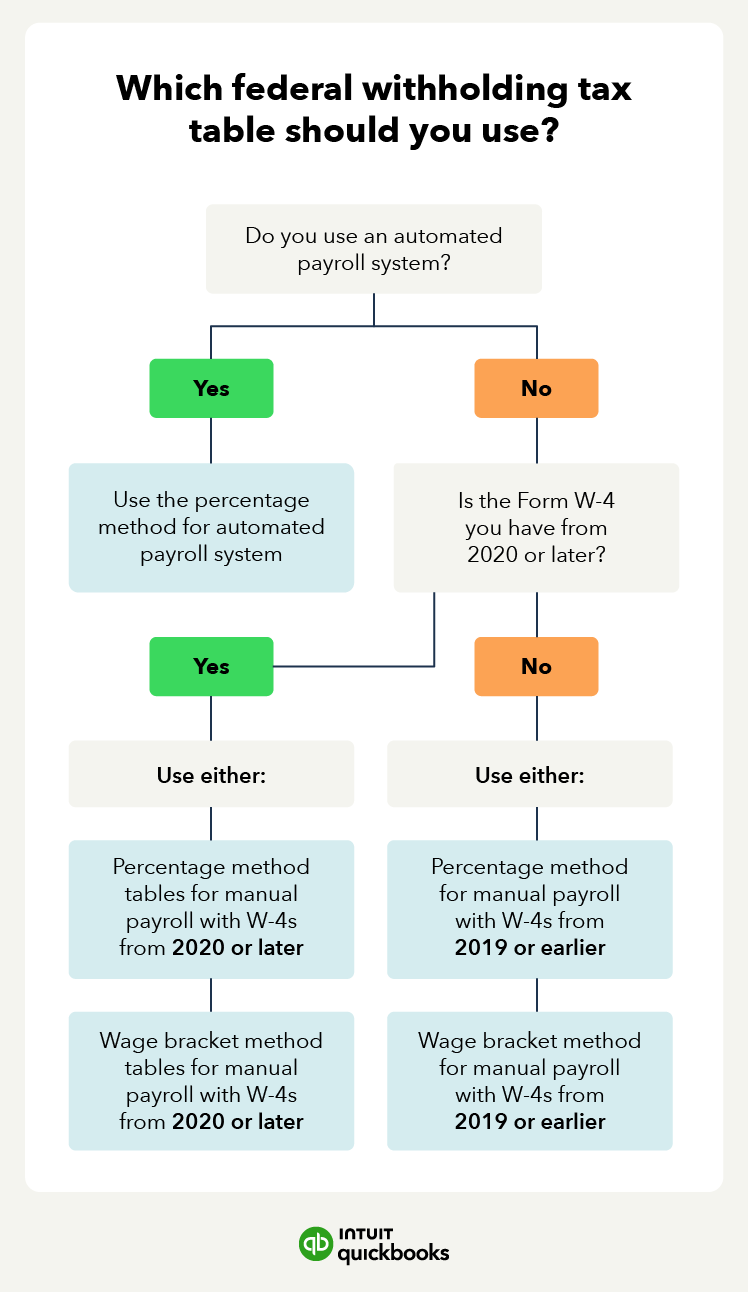

The first federal tax table from the IRS is if you have a W-4 from before 2019 or if the W-4 is from 2020 or later and the Step 2 box is not checked:

The next federal 2024 withholding table from the IRS is for automated payroll systems if the W-4 is from 2020 or later and the box in Step 2 of the W-4 is checked:

If you run payroll using a manual system, you’ll use different tables than those for businesses that use an automated payroll system built into their accounting software.

If you use a manual payroll system and have a W-4 form for 2020 or later, you can use either of these:

- IRS wage bracket method tables for W-4 from 2020 or later

- IRS percentage method tables for W-4 from 2020 or later

If you use a manual payroll system and have a W-4 from before 2019, you can use either of these:

- IRS wage bracket method tables for W-4 from 2019 or earlier

- IRS percentage method tables for W-4 from 2019 or earlier

Note that withholding allowances are not part of W-4s of 2020 or later. Before the change, employees were able to claim more allowances to decrease their federal tax withholding. But with the newer W-4s, employees can only lower their withholding by using the deduction worksheet or claiming dependents.

The IRS typically releases the final Publication 15-T for the upcoming year in December. Employers should download the official 2026 version once available to confirm the correct tables.

How to use a federal withholding tax table

A federal withholding tax table is usually in the form of a table or chart to simplify this process for employers. To determine the withholding amount, you will need an employee’s W-4 form, filing status, and pay frequency. Every new employee at a business needs to fill out a W-4 for this purpose.

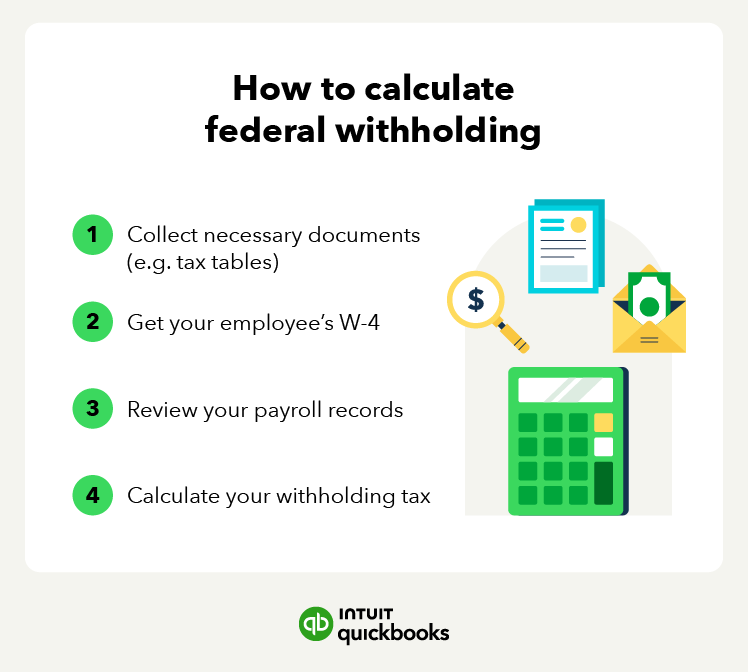

Let’s discuss how to calculate the withholding tax. Follow the steps below to calculate the necessary federal withholding income tax rate:

1. Collect necessary documents

Gathering all relevant documents from your employees is the first step in correctly calculating withholding tax. To calculate withholding tax, you’ll need your employee’s W-4 form, gross pay for the pay period, and an income withholding tax table.

2. Get your employee’s W-4

It’s important your employee fills out their W-4 correctly for your withholding tax calculations. Your employee will have to fill out their filing status, number of dependents, and additional income information. You will need to reference this form to calculate withholding tax.

3. Review your payroll records

To calculate employee withholding tax, you will need to review important information from your payroll.

As an employer, you will need to look at these payroll records:

- Payroll period information

- Frequency of the pay periods

- Gross pay amount for the pay period

An employer is also responsible for payroll withholding, which is money taken out of an employee’s gross wages. This money taken is then used to pay the employee’s portion of the payroll taxes to the federal government.

There are also payroll deductions—money taken out of an employee’s paycheck to pay for costs like employee benefits. Payroll deductions can either be mandatory, which employers are required to pay, or voluntary, which employees can pay.

Understanding payroll can be overwhelming, which is why it is useful to use a payroll accounting service to keep track of payroll costs and employee compensation.

4. Calculate withholding tax

The final step is to calculate the withholding tax. However, you’ll need to use one of several tax tables. There are two federal income tax table methods for use in 2024—the wage bracket method and the percentage method.

How to calculate federal tax withholding

There are three key types of withholding tax methods: wage bracket, percentage, and computational bridge:

The method you choose will depend on your payroll system and which W-4 you have from your employees.

Wage bracket method

The wage bracket method is a simpler method, and it tells you the exact amount of money to withhold based on an employee’s taxable wages, number of allowances, marital status, head of household, and payroll period.

QuickBooks Tip:

If you use a manual payroll system, you can use either the wage bracket or percentage method.

Percentage method

The percentage method is a bit more complex as it involves more calculations. It differs in that it has no wage limits. You can use this method if your employee’s wage exceeds the wage bracket limit. If you use an automated payroll system, it will use the percentage method.

Computational bridge

Employers can use a computational bridge to treat 2019 or earlier W-4s as if they were 2020 or later W-4s, specifically for tax withholding purposes. The computational bridge helps reduce complexity by allowing you to use data from older W-4s to calculate the withholding for your employees.

The bridge is optional, but it does mean you don’t have to use separate rules and withholding tables if you have older W-4s.

Follow these four steps to use the computational bridge:

- Step 1: Find the employee’s marital status: Select the filing status in Step 1(c) of a 2020 or later Form W-4 that most accurately matches the employee's marital status on line 3 of a 2019 or earlier Form W-4.

- Step 2: Enter an amount: Fill in an amount in Step 4(a) on a 2020 or later Form W-4 based on the filing status determined in Step 1:

- $8,600 for single or married filing separately

- $12,900 for married filing jointly

- Step 3: Multiply withholding allowances: Multiply the number of allowances claimed on line 5 of the 2019 or earlier Form W-4 by $4,300 and enter the result in Step 4(b) on a 2020 or later Form W-4.

- Step 4: Add additional withholding amounts: Enter any additional withholding amount requested by the employee on line 6 of their 2019 or earlier Form W-4 into Step 4(c) of a 2020 or later Form W-4.

QuickBooks Tip:

If your employees filled out a 2020 or later W-4, note that they can no longer request adjustments to their withholding allowances.

State vs. federal withholding taxes

Every paycheck includes taxes withheld for the government, but what’s withheld—and where it goes—depends on both federal and state rules.

Federal withholding

Federal withholding applies nationwide and includes:

- Income tax – Based on the employee’s W-4 form and IRS withholding tables (Publication 15-T).

- Social Security – 6.2% of wages, matched by the employer.

- Medicare – 1.45% of wages, also matched by the employer.

State withholding

State withholding rules vary by location:

- Most states collect state income tax, but some—such as Florida, Texas, and Washington—do not.

- States with income tax may have their own withholding forms or rely on the federal W-4.

- If an employee lives and works in different states, employers may need to withhold for both.

Understanding how federal and state systems work together helps ensure accurate paychecks and compliance while avoiding tax-time surprises. Payroll tools like QuickBooks automatically apply the correct rates for every employee, keeping your business up to date and compliant.

What are the federal taxes withheld?

Federal taxes withheld from employee paychecks generally include federal income tax, Social Security tax, and Medicare tax. The Social Security and Medicare taxes comprise what’s known as FICA taxes (Federal Insurance Contributions Act).

As a business owner, it’s important to understand each of these because you’re responsible for withholding these from your employee’s wages and submitting them to the government.

Ways to reduce tax burden in 2025 and prepare for 2026

For business owners managing payroll and expenses, staying proactive pays off. Here are some effective ways to reduce taxes now and set your business up for success in 2026 and beyond.

Maximize Bonus Depreciation and Section 179 expensing

The One Big Beautiful Bill Act restored full 100% bonus depreciation for qualifying business property placed in service after January 19, 2025. This means you can immediately deduct the entire cost of most new or used equipment, technology, or machinery in the year you purchase it, instead of spreading it out over several years. Section 179 expensing limits have also increased, allowing even more upfront deduction flexibility for small and midsize businesses.

Tip: Review your major purchases and upgrades before year-end to ensure you’re optimizing these deductions for 2025.

Claim the Qualified Business Income (QBI) deduction

OBBBA made the 20% Qualified Business Income Deduction (Section 199A) permanent. Eligible owners of S-corporations, partnerships, LLCs, and sole proprietorships can deduct up to 20% of their qualified business income from taxable income on their federal return, even if their income exceeds prior thresholds. This powerful provision can significantly reduce taxable income for many small businesses.

Take advantage of the Work Opportunity Tax Credit (WOTC)

The WOTC is a tax credit for employers who hire individuals from certain targeted groups by December 31, 2025. Employers can claim 40% of up to $6,000 in wages for employees who work 400+ hours, with a max credit of $2,400. The credit may be higher for certain other hires.

Contribute more to employee health insurance premiums

Employer contributions to health insurance are generally tax-deductible.

Benefit from the Credit for Increasing Research Activities

The Credit for Increasing Research Activities (R&D Tax Credit) is a federal incentive that allows businesses to reduce their tax liability by claiming a portion of qualifying R&D expenses, such as wages, supplies, and patent-related costs. Small businesses, including startups, can apply this credit against both income and payroll taxes, with a maximum of $500,000 per year in payroll tax offsets. This credit encourages innovation by reducing the financial burden of research and development efforts.

Consider hiring independent contractors

Independent contractors manage their own taxes, reducing your payroll tax obligations.

Start an employee retirement plan

You may be able to significantly reduce your tax bill by claiming a tax credit of up to $5,000 per year, for the first three years, when you set up a retirement savings plan such as a SEP, SIMPLE IRA, or a qualified plan like a 401(k). This tax credit directly offsets your tax liability, potentially saving you thousands of dollars.

Claim unemployment insurance tax offset

Unemployment Insurance (UI) is a federal-state program funded by employer payroll taxes. Employers must pay both federal and state unemployment taxes if they meet certain wage or employment thresholds. The Federal Unemployment Tax Act (FUTA) requires employers to pay a 6.0% tax on the first $7,000 of each employee's wages, but employers who pay state unemployment taxes on time can receive a 5.4% credit. See the IRS website for details.

Deduct everyday business expenses

Not every tax-saving opportunity requires complex calculations. Many everyday operating costs are fully deductible, helping lower your taxable income year after year. Typical business tax breaks include:

- Rent or lease payments for business property

- Office supplies and equipment

- Business insurance premiums

- Professional and legal fees

- Advertising and marketing costs

- Utilities, phone, and internet services

- Business travel and meals (subject to IRS limits)

Stay informed and seek guidance

Tax laws evolve every year, especially under new legislation like the OBBBA. Regularly review IRS updates and consult a tax professional to identify deductions and credits your business qualifies for.

Find peace of mind come tax time

Correctly calculating withholding taxes is crucial for many reasons. To run a business efficiently and pay your employees accurately, you want to ensure employee W-4 forms are complete.

Using a payroll service like QuickBooks Workforce to handle calculations can simplify your life as a business owner. QuickBooks Workforce offers everything from HR support to a paycheck calculator, so you can spend less time focusing on payroll and more time running your business.

Federal withholding tax table FAQ

What are the federal income tax rates for 2026?

The federal withholding tax rates from the IRS for 2026 are 10%, 12%, 22%, 24%, 32%, 35%, and 37%. This is unchanged from 2023.

Do employers have to withhold taxes?

Yes, employers do have to withhold taxes. Incorrect federal withholding tax calculations can result in many issues for your business. An employer is legally responsible for withholding payroll taxes and paying those taxes to the Internal Revenue Service (IRS).

How do you determine federal withholding?

The federal withholding tax an employee will pay will depend on filing status and the amount of money they make. This will depend on the individual’s filing status, such as single or married filing jointly.

Did federal withholding tax tables change for 2026?

Yes, the federal withholding tax tables are different for 2026. The IRS adjusts income thresholds for the tables each year to account for inflation. Thus, the federal income withholding tables change every year.

Call Sales: 1-877-202-0537