You could save up to 25% on transaction costs².

Speak with us now to see if you qualify.

Talk to sales 1-800-515-8366

Monday - Friday, 6 AM to 4 PM PT

Table of contents

Table of contents

As a small business owner, you have a lot on your plate, and payroll is one of the most important things to get right. From keeping your employees paid on time to ensuring that additional payments like overtime, tips, and bonuses are accounted for, you have a lot to juggle.

And that's before you factor in taxes. According to our QuickBooks Entrepreneurship survey, 34% of business owners have made an error when filing business taxes, whether that's overpaying, underpaying, or using the wrong forms.

Payroll withholding is one area where those mistakes are especially costly. It’s the process of deducting the correct taxes and contributions from each employee’s paycheck before they’re paid—and as the employer, the responsibility falls on you to get it right.

This guide breaks down everything you need to know about payroll withholding, from what it is and which taxes you’re responsible for to how to calculate and master the process for your business.

Payroll withholding is when an employer deducts a portion of their employees' pay to satisfy legal tax requirements. While freelancers, independent contractors, and other self-employed workers must pay quarterly taxes, full- and part-time employees have those taxes withheld from their paychecks by their employer.

Payroll withholdings are considered a payroll liability for companies until they've been submitted to the government. However, the withheld employee pay used to cover payroll taxes isn't technically a business expense, since it's already accounted for in each employee's gross pay.

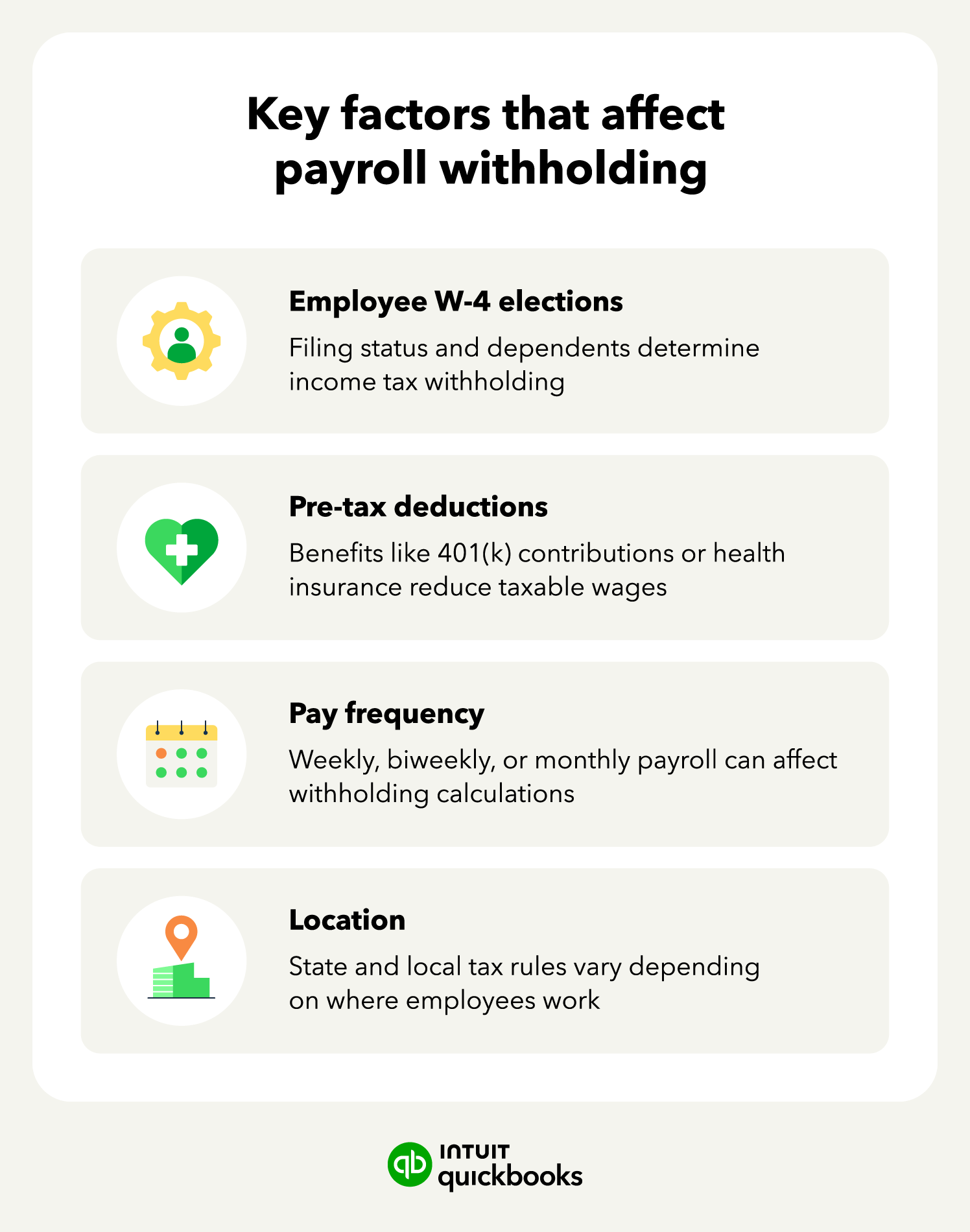

As the employer, you're responsible for withholding, reporting, and submitting taxes on your employees' behalf. Employees indicate how much should be withheld by completing a Form W-4 (typically completed during onboarding), which helps determine the amount of federal income tax to withhold.

However, you’re responsible for applying IRS withholding tables and calculating the correct amounts each pay period. Employees can update their W-4 at any time if their tax situation changes, so make sure they know that option exists.

Payroll withholding includes several different taxes and deductions that must be taken from employee wages each pay period. Let’s go over some of the most common payroll deductions employers need to manage.

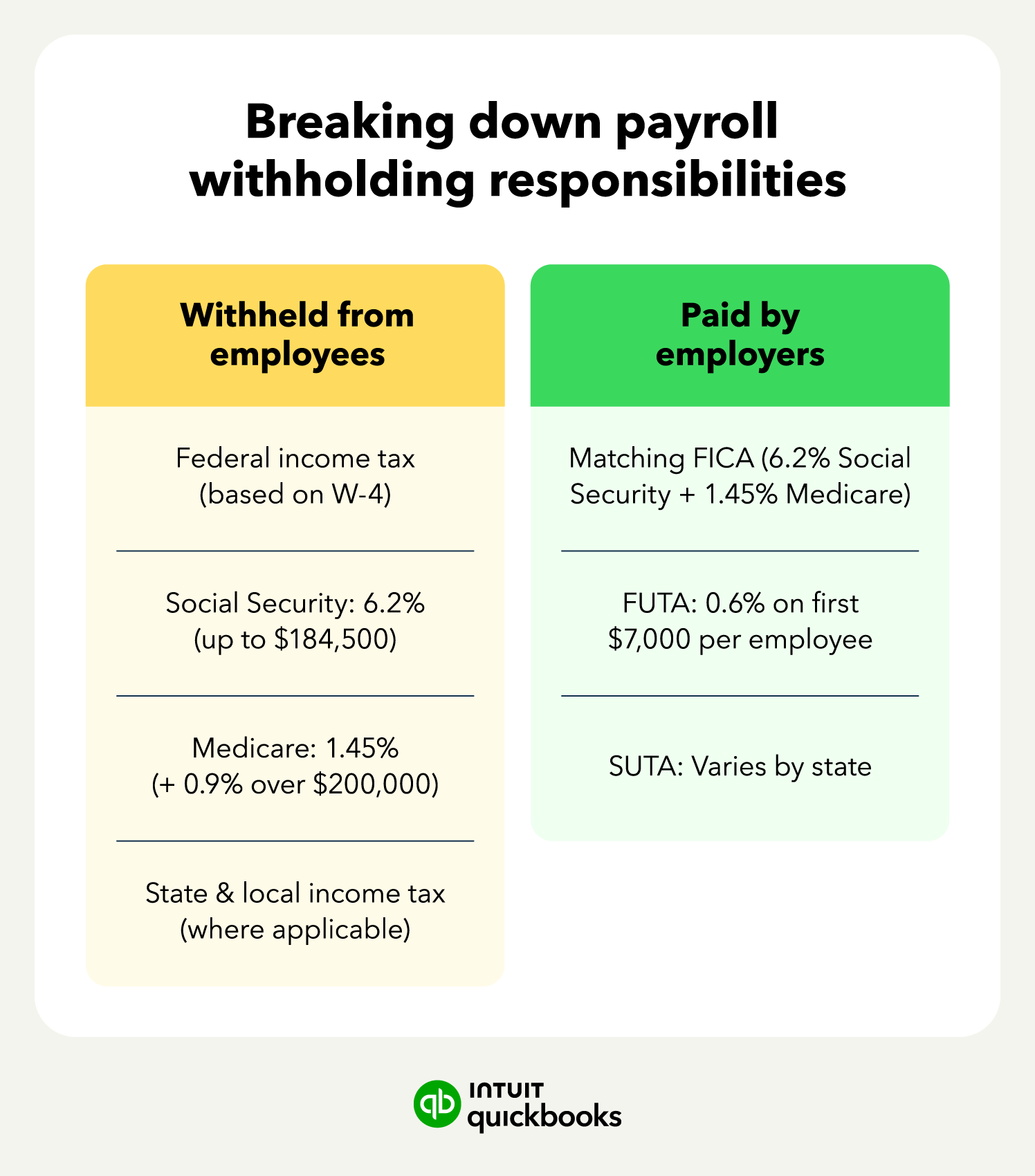

Social Security taxes fund the program that provides financial support to retirees, people with disabilities, and those unable to work. Along with Medicare taxes, they make up FICA taxes, established under the Federal Insurance Contributions Act.

According to the IRS, employers must withhold 6.2% of employee wages for Social Security (up to the $184,500 wage base limit in 2026) and contribute a matching 6.2%, for a combined 12.4% total.

Medicare is the public program that provides reduced-cost health care to retirees who no longer receive benefits from work. Employers withhold 1.45% of employee wages for Medicare and contribute a matching 1.45%, for a combined 2.9% total. And unlike Social Security, there's no wage base limit, so all covered wages are subject to Medicare tax.

High-income employees earning over $200,000 also owe an additional 0.9% Medicare tax. You're required to start withholding it in the pay period if their wages exceed that threshold and continue through the end of the calendar year. Note that there's no employer match for the additional 0.9%.

Federal income tax is withheld from employee wages each pay period based on their W-4 elections. The amount withheld depends on factors like filing status, dependents, and any additional withholding the employee requests.

State and local tax rules vary significantly depending on where your business operates. Some states have no income tax; others have additional local taxes on top of state withholding. Make sure your payroll is set up to reflect the correct tax rates for every state or jurisdiction where your employees work.

If an employee has a legal need to pay a fine or other court-mandated withholding, an employer may be required to garnish wages on their behalf. You have to comply with these orders to help the authority recover unpaid debt.

Be sure that employees always have an open line of communication to ensure that you’re withholding the right amount. For example, if you receive a court order for child support, you’re required to withhold the specified amount from the employee’s wages and remit it as directed.

Know your deposit schedule The IRS assigns businesses either a monthly or semiweekly payroll tax deposit schedule based on total tax liability. Missing a deposit deadline can result in penalties, so check your schedule in IRS Publication 15 and set reminders to stay on track.

Know your deposit schedule The IRS assigns businesses either a monthly or semiweekly payroll tax deposit schedule based on total tax liability. Missing a deposit deadline can result in penalties, so check your schedule in IRS Publication 15 and set reminders to stay on track.

Employers are also responsible for paying federal and state unemployment taxes, which fund unemployment benefits for workers who lose their jobs.

The Federal Unemployment Tax Act (FUTA) rate is 6% on the first $7,000 of each employee's wages, though most employers qualify for a credit that reduces it to 0.6%. State unemployment tax (SUTA) rates vary by state and are based on factors like your industry and claims history.

Unlike other payroll taxes, unemployment taxes are paid entirely by the employer—nothing is withheld from employee paychecks.

In addition to required payroll deductions, employees may decide to have more money taken out of their paychecks to cover various employee benefits. Here are some of the most common voluntary deductions employers manage through payroll.

Employees may opt into your company-provided health benefits. If they do, then they may ask you to withhold a part of their wages to cover the employee-paid portion of the premiums. The way the responsibility for health care premiums is divided between the business and employees is up to you as the employer.

Many businesses offer basic group-term life insurance to employees at no cost. Under IRS rules, the first $50,000 of this coverage is tax-free. Employees wishing to increase their coverage or buy life insurance for a dependent may do so through post-tax deductions.

If your business offers a 401(k) retirement plan to employees, you're responsible for withholding employees’ contributions if they choose to use it. Helping your employees automate these savings is a powerful way to boost total compensation value without direct salary increases.

Withholding payroll taxes may seem complicated, but the process is fairly straightforward. You can calculate payroll tax withholding by following these steps:

Start with the employee's total earnings for the pay period before any deductions. This includes base wages or salary plus any overtime, bonuses, commissions, or tips. Gross pay is the starting point for all withholding calculations.

Next, subtract any pre-tax deductions from gross pay, such as 401(k) contributions, health insurance premiums, and FSA or HSA contributions. These reduce the employee's taxable income, which lowers the amount of federal and state income tax withheld.

Using the employee's W-4 and the IRS withholding tables in Publication 15-T, calculate the federal income tax amount. The result depends on the employee's filing status, pay frequency, and any additional withholding they've requested.

Federal income tax withholding calculations can get complex fast. Payroll software like QuickBooks automatically applies the correct withholding tables so you don't have to do it manually—reducing the risk of costly errors.

Multiply taxable wages by the current FICA rates—6.2% for Social Security (up to the $184,500 wage base) and 1.45% for Medicare. Remember to calculate your matching employer contribution as well.

Apply the applicable state and local tax rates for where your employees work. Rates and rules vary by jurisdiction, so make sure you're working with current figures.

Using a payroll system like QuickBooks automatically applies the correct state and local rates based on your employees' work locations, so you don't have to look them up manually each pay period.

Finally, subtract any post-tax deductions such as wage garnishments, union dues, or voluntary deductions that apply after taxes have been calculated.

Pay the withheld taxes to the IRS on the deposit schedule designated for your business—typically monthly or semiweekly. Missing a deadline can result in penalties, so make sure you know which schedule applies to you.

Be sure to always keep thorough payroll records, including W-4 forms, pay stubs, and tax payment receipts. You'll need these when it's time to file your small business taxes.

Let's walk through a real example to see how payroll withholding works in practice.

Say you have an employee, Sarah, who earns $4,000 in gross pay per month. She contributes $200 to her 401(k) pre-tax, has employer-sponsored health insurance with a $150 employee premium, and has selected "Single" with no additional withholding on her W-4.

Here's how her withholding breaks down:

As the employer, Sarah’s paycheck isn’t your only cost. You must also pay a matching $226.30 for Social Security and $52.93 for Medicare. In total, while Sarah sees $2,969.27, the actual cost to your business for this pay period is $4,279.23 (gross pay + employer taxes).

Now that you understand how payroll withholding works, the next step is making sure your process is accurate and efficient. Manually calculating withholdings leaves room for error, which can be time-consuming and expensive.

Payroll software like QuickBooks handles the calculations for you, keeps up with changing tax rates, and automatically generates the forms you need to stay compliant. It's one of the simplest ways to protect your business and free up time to focus on growth.

Call Sales: 1-800-285-4854