Financial confidence remains a major hurdle for new business owners. In fact, according to QuickBooks report on Business Ownership in 2026 more than half of U.S. adults say they lack confidence in key business finances, from cash flow management to taxes. This uncertainty often stems from not having a clear source of truth for their data.

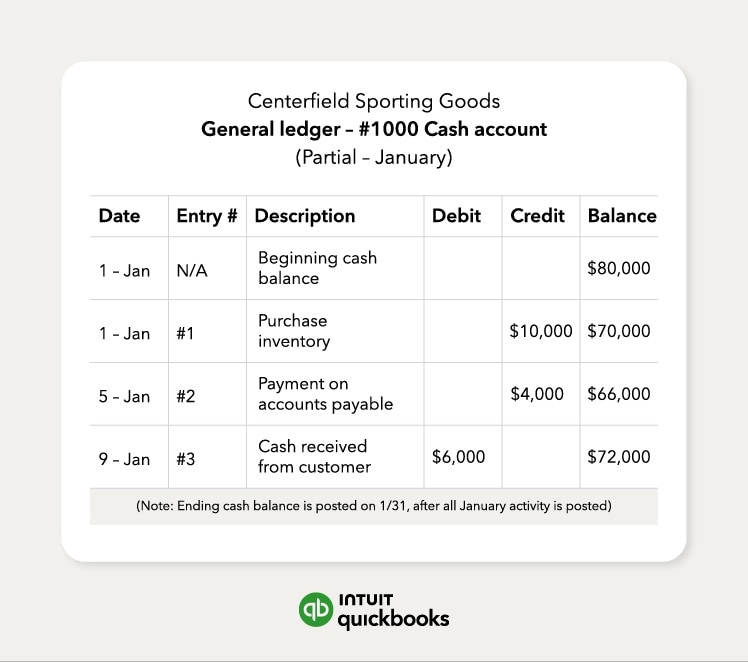

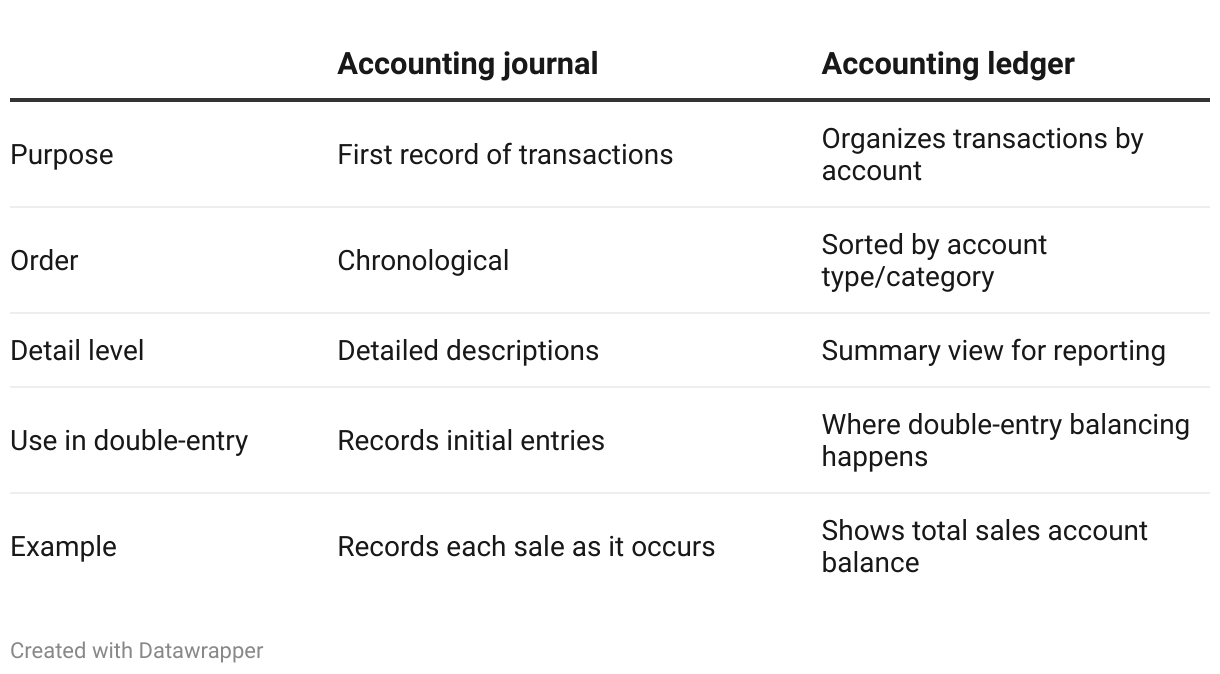

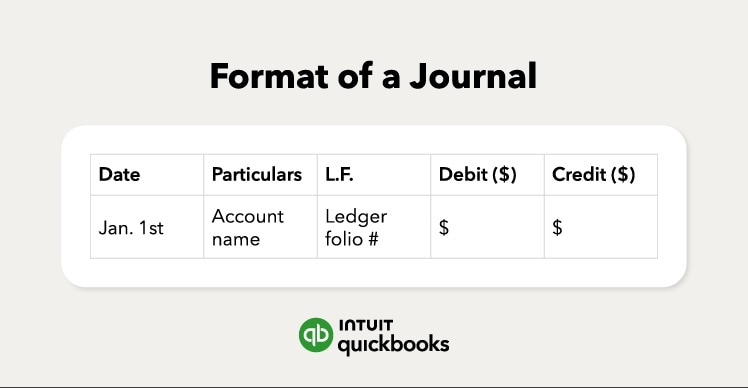

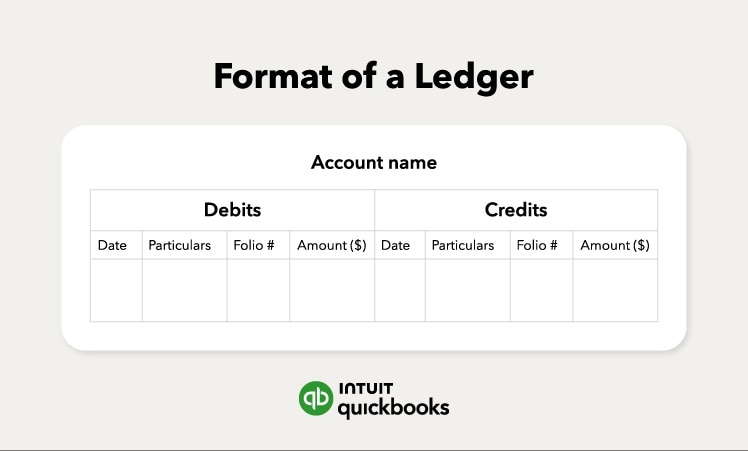

A general ledger, or an accounting ledger, is the main record of your business’s financial standing that centralizes all your financial transactions. Businesses use an accounting ledger to help keep finances in order and prepare several reports, such as balance sheets and income statements.

By maintaining an accurate accounting ledger, you move past the guesswork that impacts 70% of owners' ability to reach their goals. This record is the foundation used to prepare critical reports, such as balance sheets and income statements, ensuring you always have a clear view of your financial health.