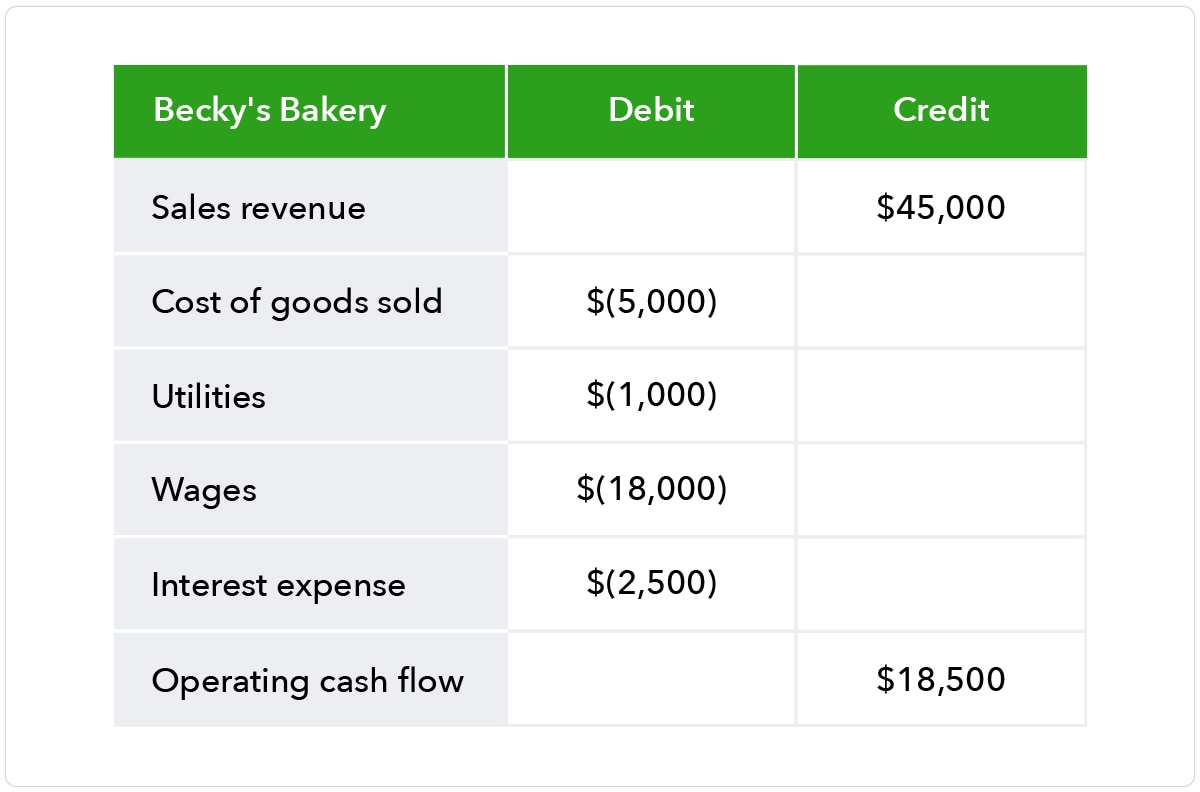

Indirect method

Operating cash flow formula:

Net income +/- changes in assets and liabilities + noncash expenses = OCF

The indirect method uses the statement of cash flows formula to compute cash flows from operations. The statement of cash flows reports increases and decreases in cash and divides the activity into three categories:

- Cash flow from financing activities: This category includes raising money by issuing stock or debt, paying stockholders dividends, and repaying debt.

- Cash flow from investing activities: Cash transactions that involve buying and selling company assets.

- Cash flow from operating activities: All of the cash activity that is not included in the first two categories. Purchasing inventory, making payroll, and collecting customer payments are posted here.

You can calculate cash flow from operating activities using the indirect method. Here is the indirect formula in detail:

- Net income

- Add: Decreases in current assets

- Add: Increases in current liabilities

- Add: Noncash expenses

- Subtract: Increases in current assets

- Subtract: Decreases in current liabilities

Current assets include cash and assets that are expected to be converted into cash within 12 months. Inventory, for example, is expected to be sold within a year. On the other hand, current liabilities are expected to be paid within 12 months. Your accounts payable balances are a current liability.

Noncash expenses include depreciation expenses and amortization expenses. Depreciation expenses are posted to record the decline in value of physical assets, including machinery or equipment. You post amortization expenses to record the decline in value of intangible assets, such as a patent.

The formula is complex, so let’s use a basic example to explain how the calculation works. Assume a company has $50,000 in net income, and other accounting activity that impacts the formula:

- $50,000 net income

- Add: $5,000 decrease in inventory (current asset)

- Add: $2,000 increase in accounts payable (current liability)

- Add: $10,000 in depreciation expenses (noncash expense)

- Subtract: $12,000 increase in accounts receivable (current asset)

- Subtract: $4,000 decrease in long-term debt due within a year (current liability)

OCF equals $51,000.