It’s a scenario many midsize business leaders know too well: Your P&L looks fantastic. Sales are up, revenue is climbing, and on paper, the business is more profitable than ever. Yet, when it comes time to run payroll or pay vendors, the bank account tells a different story.

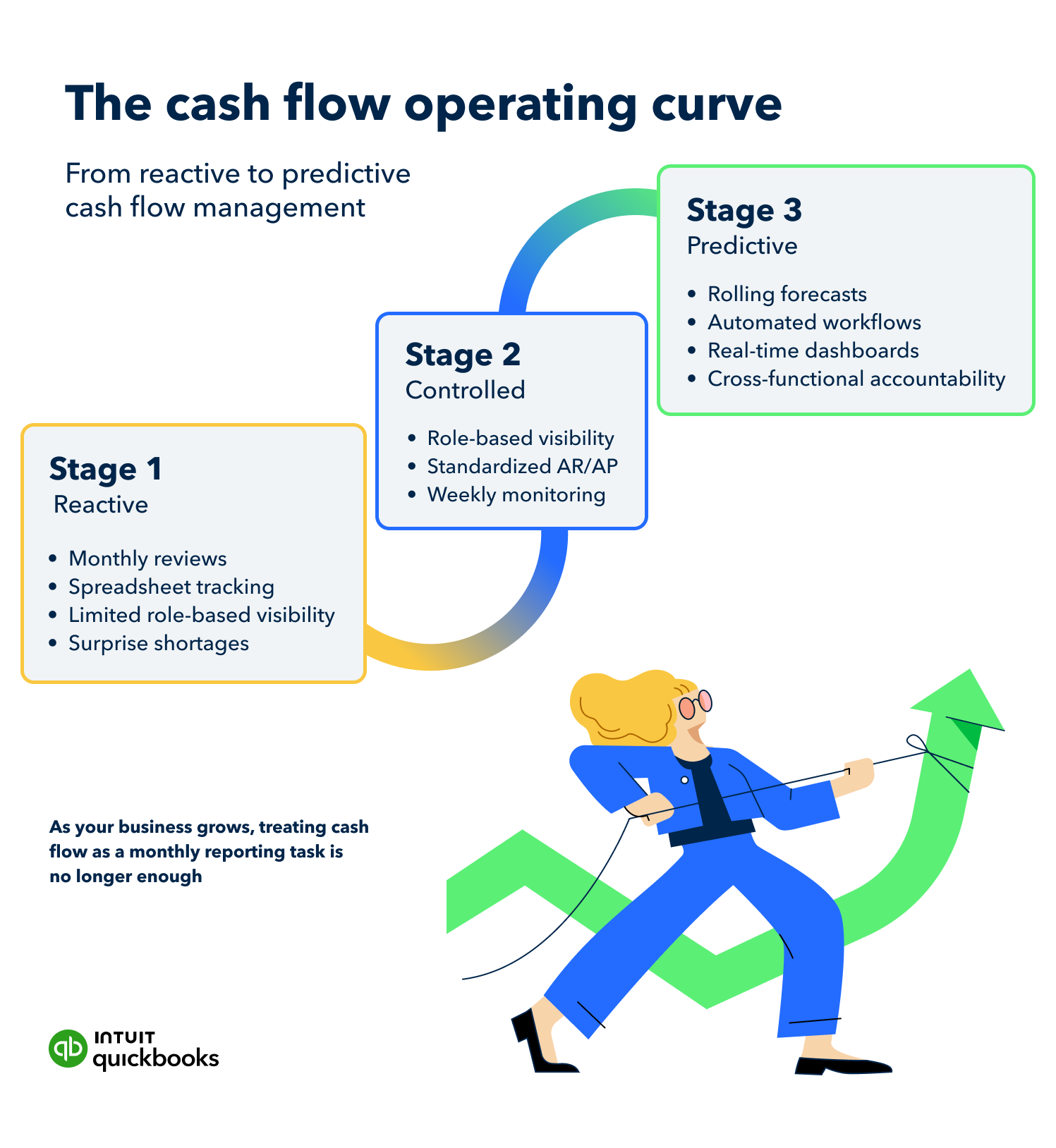

This disconnect is often a sign of growth. As your business scales from a small operation to a mid-market contender, the timing gap between earning revenue and collecting cash often widens.

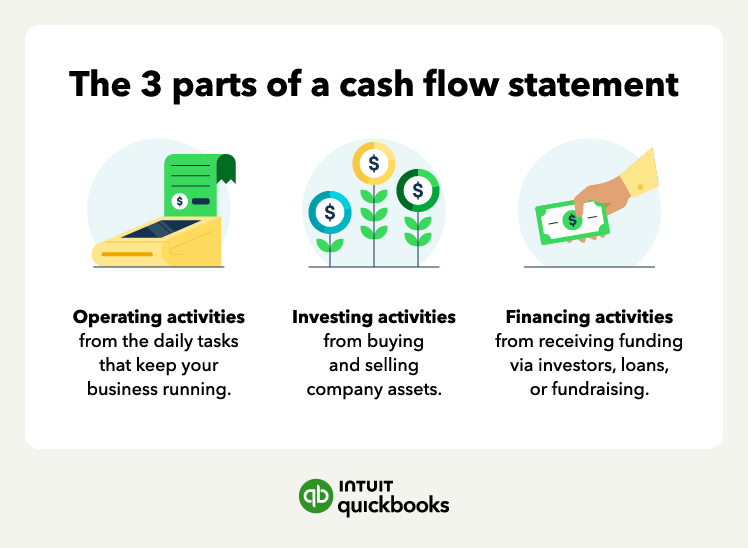

A statement of cash flows explains why strong profits don’t always result in available cash. It doesn't just tell you where the money went; it highlights how your operational decisions, investment choices, and financing strategies impact your liquidity. For scaling businesses, the statement of cash flows provides the visibility needed to fund the future.

Access to real-time financial data becomes even more important when growth accelerates. Platforms such as QuickBooks Online Advanced offer live reporting and forecasting to help teams monitor cash flow as decisions happen.

Jump to:

- Why cash flow gets harder as companies scale

- Parts of a cash flow statement

- How to calculate cash flow

- Where cash flow visibility breaks down

- How to calculate cash flow

- Direct vs. indirect method

- Statement of cash flows template

- Statement of cash flows example

- Cash flow management best practices for growing businesses

- Moving from reactive reporting to proactive planning

- Navigate midsize business challenges and opportunities

- Statement of cash flows FAQ