Nervously, you open the letter from the IRS, and your heart sinks; it's an audit notice. Depending on the complexity of your business, you may have IRS agents combing through your finances for 6+ months.

No one wants to be in this situation, but is there anything you can do to help prevent an audit? While some audits are random, there are known triggers. In this article, we’ll take a look at what triggers a tax audit, what you can do to avoid the trigger, and what key steps you need to take to decrease your audit risk.

Jump to:

- What is a tax audit? How the IRS evaluates your finances in 2026

- Trigger 1: Digital payment mismatches

- Trigger 2: The new Form 1099-DA

- Trigger 3: Contractor and third-party payment gaps

- Trigger 4: The rounding red flag

- Trigger 5: S-corp distributions

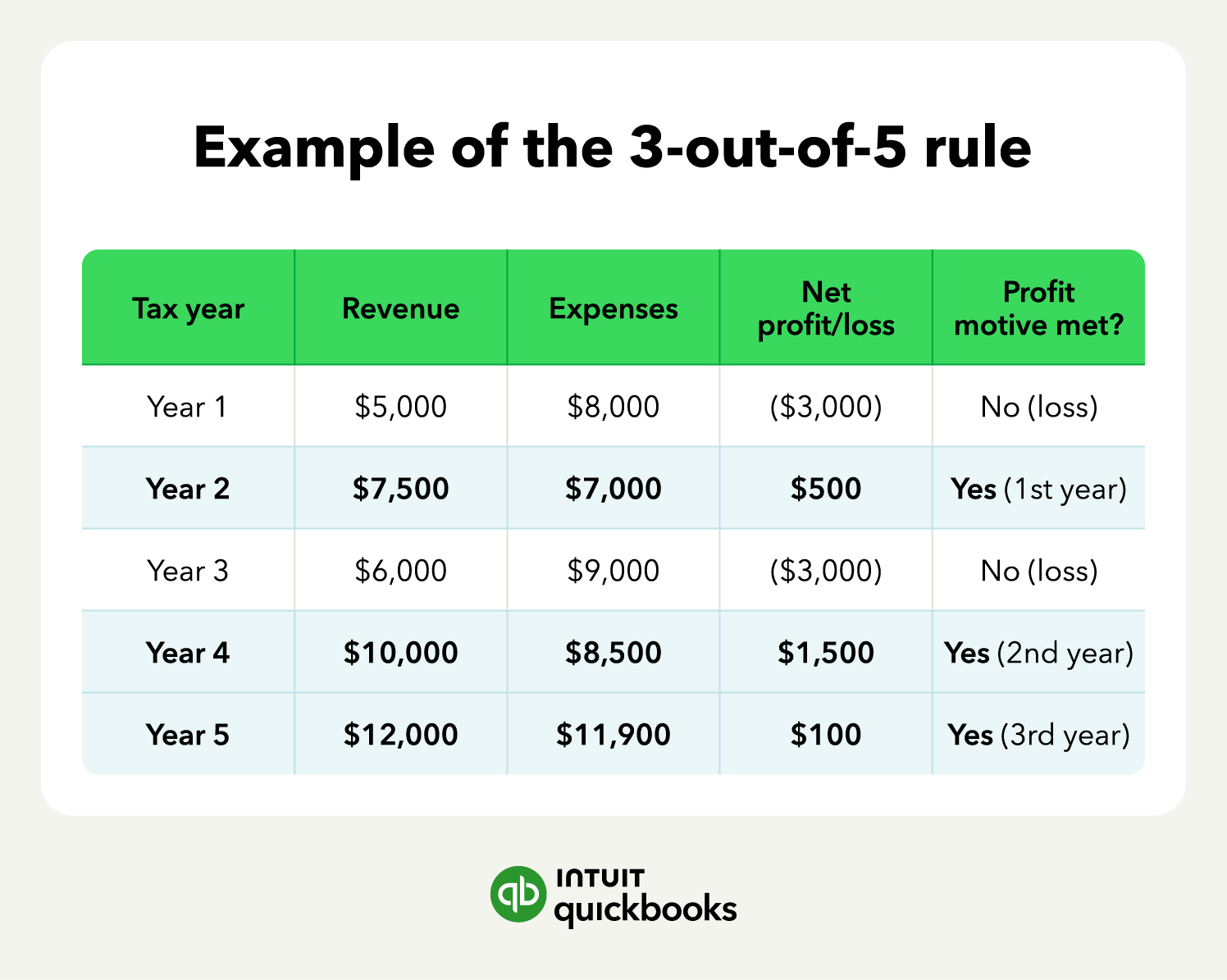

- Trigger 6: The 3-out-of-5 rule

- Trigger 7: Excessive home office & vehicle claims

- How to protect yourself against a tax audit

- Find peace of mind come tax time