ACH bank transfers are a practical way for businesses to improve how quickly their clients pay up. A major QuickBooks survey reported that 56% of small companies have to wait more than 30 days for customers to pay their invoices. ACH payments settle in just a few days, easing pressure on your cash flow by closing the gap between sending an invoice and getting paid.

Below, learn about the different types of ACH payments, how they work, their benefits, and how to handle them with your accounting software.

Jump to:

- Understanding what ACH payments are

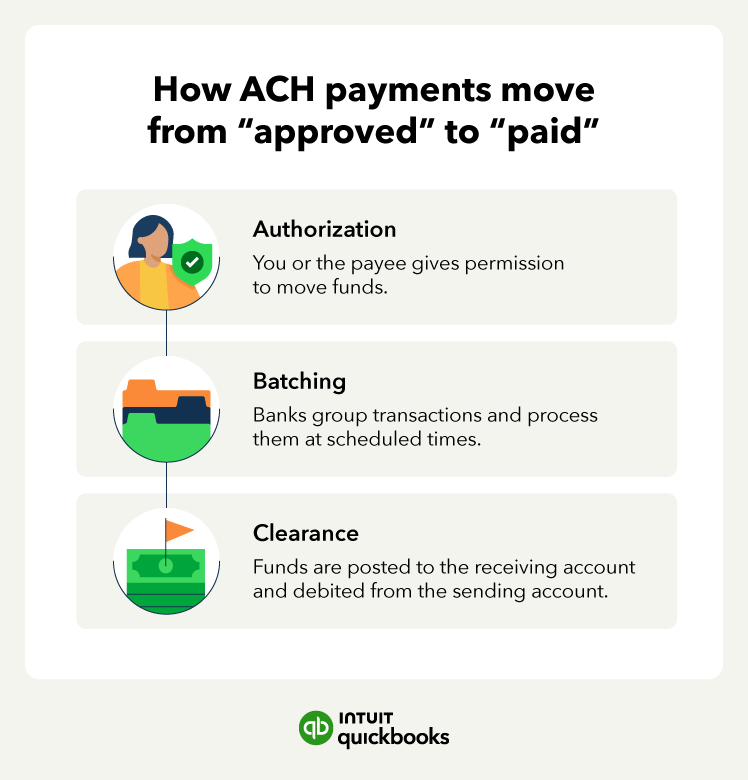

- How ACH payments work

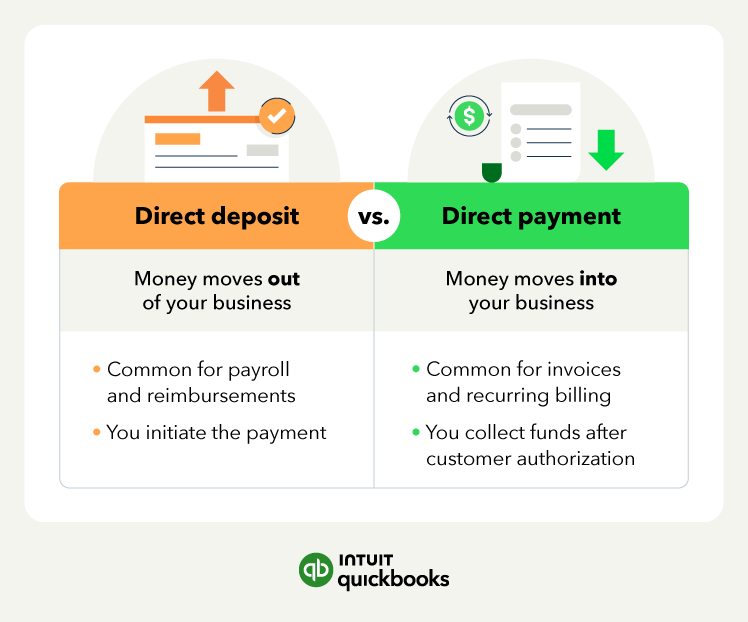

- Types of ACH payments

- What's the difference between ACH payment vs. wire transfers?

- How to accept ACH payments as a business

- What are the benefits of ACH payments?

- How much does ACH payment processing cost?

- How long do ACH transfers take?

- Choose the best payment setup for your business