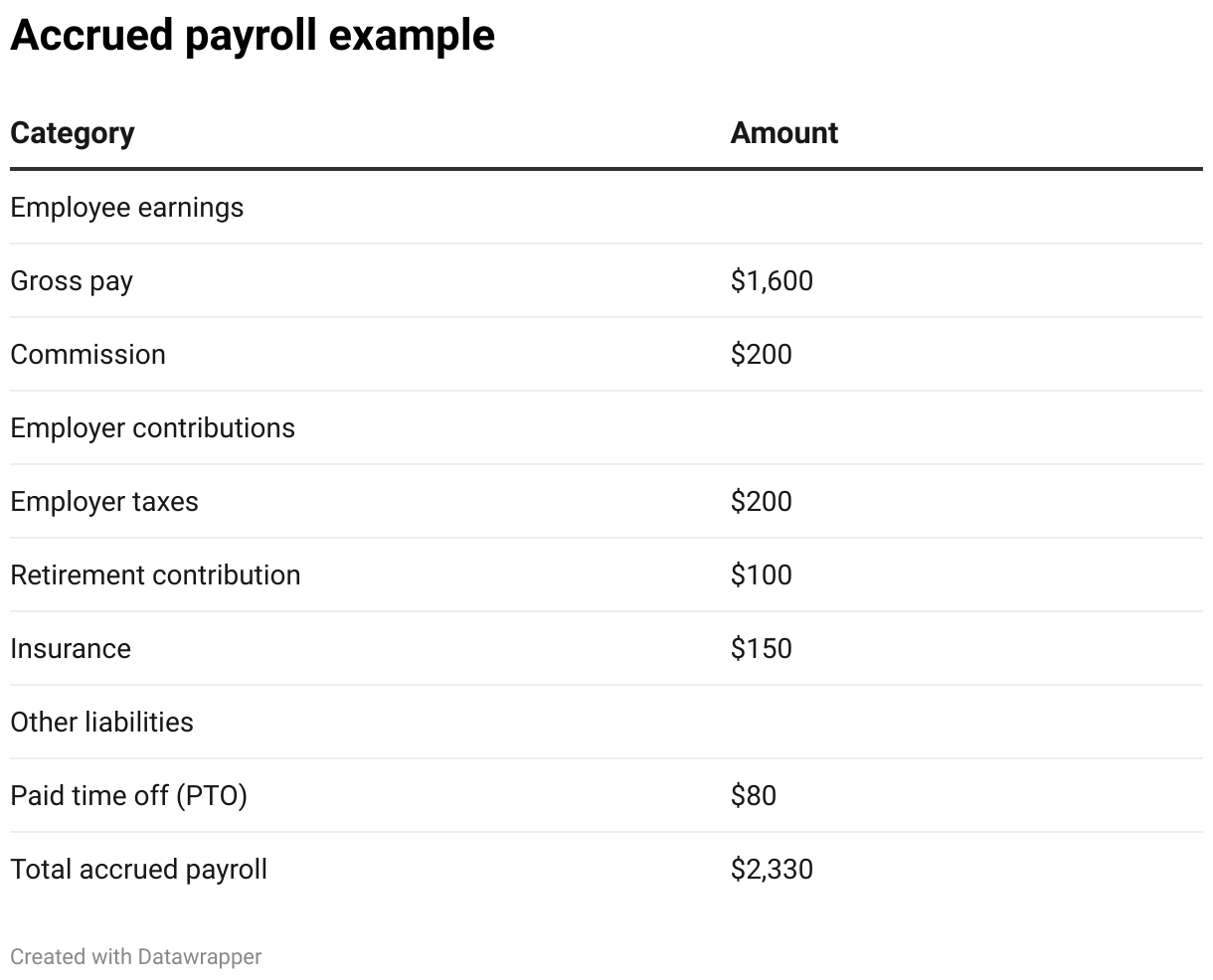

How to calculate accrued payroll

Curious how to calculate accrued payroll yourself? Follow these steps for each employee who works at your business:

1. Hours worked x hourly wage = outstanding payroll

First, calculate the number of hours a given employee worked. Then, multiply that by their hourly wage. That is the total amount that you owe them for that pay period.

Be sure that you add together only the hours that they’ve worked that they have not been paid for. It’s a good idea to pay your employees on a regular basis. That way, they know when to expect a paycheck, and you know the period to calculate their pay for. Plus, most states have a required pay frequency—make sure you’re familiar with these laws.

2. Factor in bonuses, commission, and overtime

If your employee has earned any extra wages apart from their regular hourly rate, add that to the total. If you’re not sure how to calculate overtime pay, you can check out our informative guide: How to calculate overtime pay for hourly and salaried employees.

Any bonuses, cash prizes, or commissions that were awarded to employees immediately won't be counted in accrued payroll.

3. Payroll taxes (FICA), health insurance, and retirement contributions

The next step is a bit tricky. Be sure to differentiate between employee contributions to Federal Insurance Contributions Act (FICA) taxes and employer contributions to FICA taxes. The latter will be a portion of your accrued payroll; the former was already accounted for in gross pay.

Next, add the amount you contribute to your employee’s health insurance premiums. Usually, this amount is split between an employer and an employee, so account for only your portion of this cost. In addition, if you include a retirement contribution matching program for employees’ 401(k) accounts, then also include your contribution amount during this step in the calculation.