You could save up to 25% on transaction costs².

Speak with us now to see if you qualify.

Talk to sales 1-800-515-8366

Monday - Friday, 6 AM to 4 PM PT

Table of contents

Table of contents

As a small business owner, meeting the needs of your employees is a crucial component of building a productive, reliable team. While reasons behind high churn and low productivity can vary by the individual, the broad trends remain clear: According to Intuit QuickBooks and Allstate Health Solutions survey, 78% of employees would switch jobs for better benefits, and 74% of employees report financial stress negatively affecting work motivation.

Small business leaders are tackling both problems at once. By offering paycheck advances as part of a well-rounded compensation benefits package owners are expanding perks and increasing financial stability for their employees. But what is a paycheck advance, exactly?

This blog will cover the benefits and limitations of paycheck advances, how best-in-class payroll software can properly implement it into your company, and the measurable improvements they can mean for worker productivity and your bottom line.

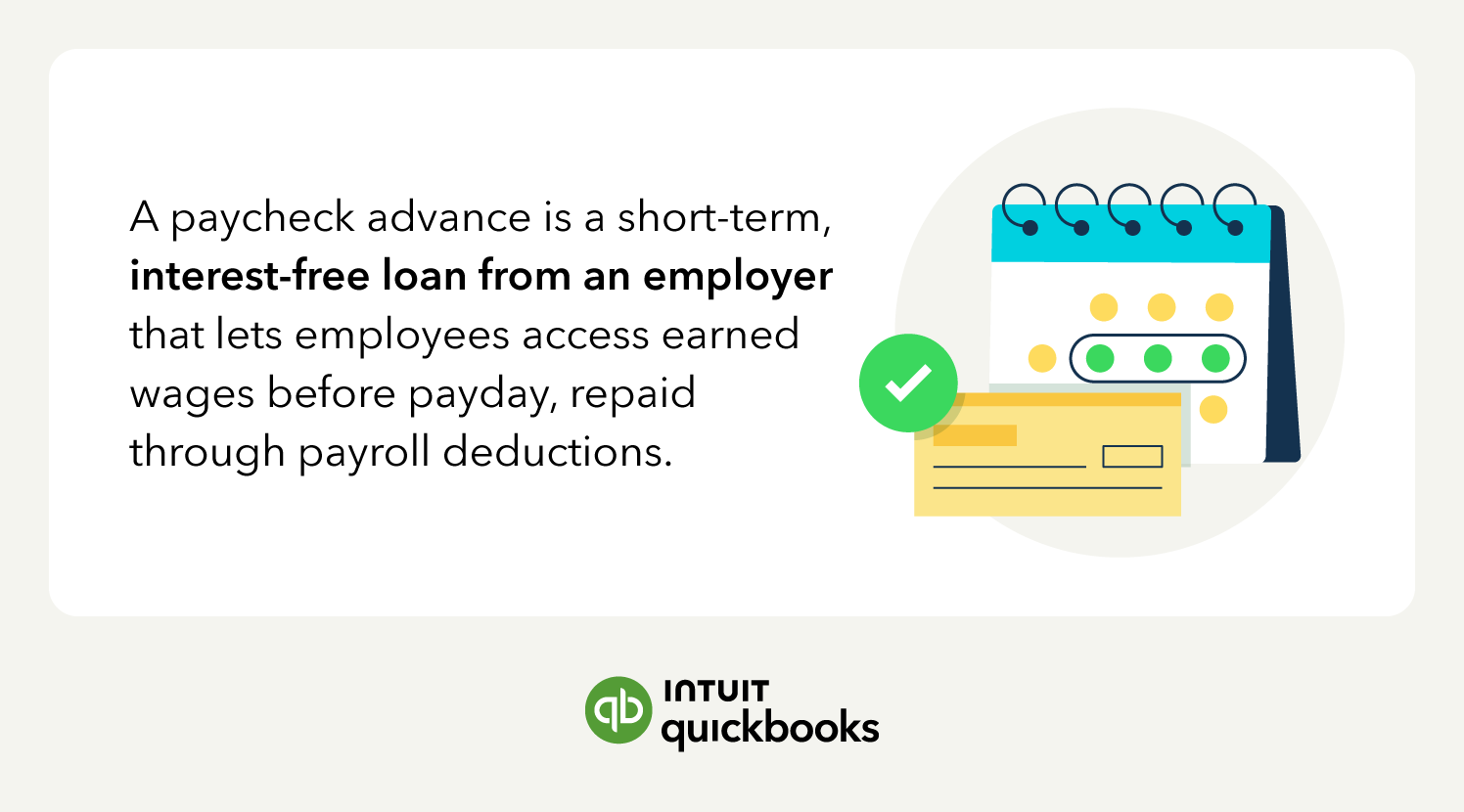

A paycheck advance (also known as a payroll advance) is a short-term loan paid by an employer to an employee before their scheduled payday, repaid through deductions from future paychecks.

While paycheck advances are interest-free and not taxed when issued, taxes are calculated and withheld as usual when the employee's wages are processed through payroll.

Paycheck advances should not be confused with payday advances, which are high-interest loans provided by third parties or term loans, which bridge cash gaps for the small business itself, not the employee.

Offering paycheck advances provides welcome financial relief to employees, especially when facing unexpected emergency expenses, without increasing payroll expenses.

For example, an employee needing $500 to cover a hospital bill before payday may ask for that sum as a paycheck advance. If a $500 payday dedication all at once would cause additional strain or undercut the benefit of the advance, the employee could ask to repay the loan over five pay periods with automatic deductions of $100 on each paycheck.

Once the exact sum, repayment timeline, and installment amounts are agreed upon, the employer can issue a check or an ACH payment immediately, providing much-needed peace of mind.

States like California, Maryland, and New York have specific labor laws regarding wage deductions. When offering paycheck advances, employers must follow state rules on written authorization, repayment terms, and minimum wage requirements.

Because these rules vary by state, it’s important to review local labor laws or consult with HR or legal counsel before implementing a paycheck advance policy. Make sure your policy complies with both federal and state labor laws.

Employers must manage cash flow, document all agreements, and comply with labor and tax laws. Other responsibilities include:

When handled correctly, paycheck advances can be a helpful employee benefit.

While they sound similar, these options work differently and carry distinct risks and benefits.

Paycheck advances can offer greater coverage than earned wage access, since the amount isn’t limited to hours worked that pay period. Unlike payday loans, paycheck advances are interest-free.

Now that you know what an advance on a paycheck is, you can start offering them to employees. If you decide to offer paycheck advances, start by introducing the policy clearly and proactively. Don't wait for an emergency—get ahead of questions by building understanding into onboarding, employee handbooks, or staff meetings.

Clearly explaining the process up front can help avoid confusion or misunderstandings later. Use the following points to guide your internal messaging.

Paycheck advances should be offered sparingly and only in situations where an employee faces a short-term financial emergency. Try to set limits on how often and how much employees can request.

Without clear policies, salary advances can create confusion, legal issues, or financial strain on your business. Your policy should include:

Discuss repayment terms up front, including how taxes and deductions may be affected. Be clear that the advance will reduce future net pay, and explain how that may impact employees who live paycheck to paycheck.

This benefit can build trust and improve morale, but it works best when both sides know what to expect and how it fits into your company’s broader financial policies.

Imagine an employee named Jordan normally earns $1,200 net per pay period but needs $300 to cover the cost of a window that got broken during a storm. Without a paycheck advance, Jordan could face a week or more of uncomfortable drafts, high utility consumption, and home security concerns.

Instead, Jordan comes to you and asks for a paycheck advance. You both agree to a single payment installment, rather than smaller deductions over several pay periods.

You issue the $300 paycheck advance, Jordan is able to fix the window quickly, and come payday, your system automatically deducts the $300 advance from Jordan’s net salary and issues a paycheck of $900.

The best accounting software will automatically record the paycheck advance, the deducted repayment, and the revised payday paycheck while withholding all applicable taxes on Jordan’s total salary so that net pay is unaffected.

Before offering paycheck advances, it’s important to understand the potential upsides and trade-offs for both your employees and your business.

While these advances can be a lifeline during emergencies, they also require careful planning and clear communication to avoid unintended consequences. Below, we break down the key pros and cons:

Processing a paycheck advance requires clear communication, proper documentation, and payroll coordination. A consistent, step-by-step process ensures both legal compliance and financial clarity for everyone involved.

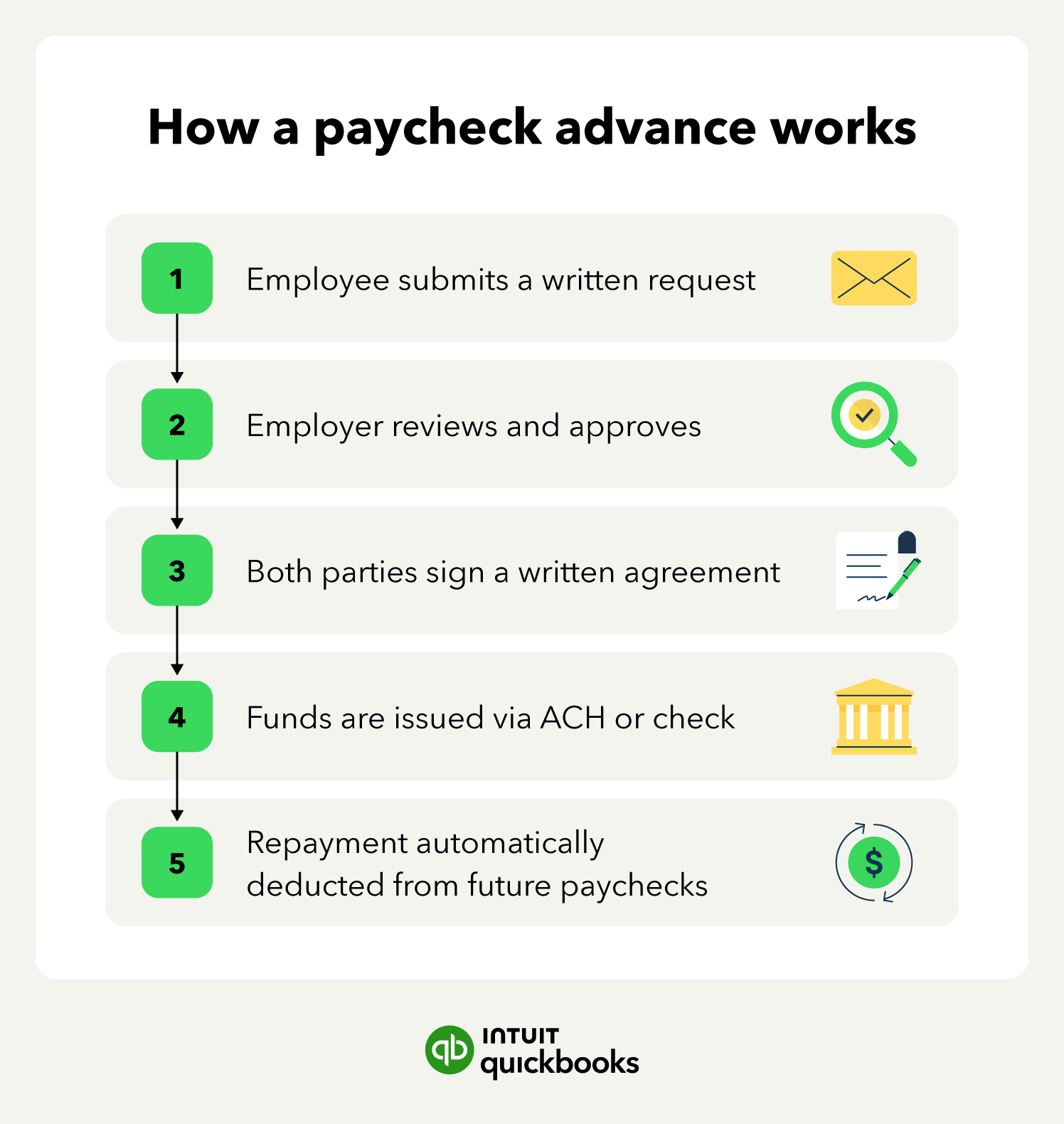

You can follow these five steps to process a paycheck advance:

1. Have the employee submit a written request, including the amount needed and the reason for the advance.

2. Review and approve the request with HR or management to confirm the employee meets your eligibility criteria.

3. Draft a paycheck advance agreement that both parties sign. Document the advance amount, disbursement date, repayment schedule, deduction amounts, and a contingency plan if employment ends before repayment.

4. Record the advance in your payroll system as a nontaxable loan—not income—and set up automatic deductions. Confirm that deductions won't reduce the employee's pay below minimum wage.

5. Maintain records for auditing and internal tracking throughout the repayment period.

While paycheck advances are designed to be flexible, they cannot be treated as completely freeform. There are several payroll compliance factors to consider.

Payroll advances from employers structure repayment around deductions from subsequent paychecks. However, the Fair Labor Standards Act (FLSA) mandates that the deducted wages cannot be so large as to drop the employee’s take-home pay below minimum wage for the hours worked that pay period.

The federal minimum wage is $7.25 per hour, but many states have implemented higher minimum wages, and the employee is entitled to the greater of the two.

Therefore, depending on the size of the paycheck advance, a single, lump-sum payment may not be legally possible. In such cases, the employer will be obligated to spread the repayment over several pay periods, even if that goes against the employee’s preference.

Secondly, paycheck advances are nontaxable loans only if they are documented as such. While professional accounting software can improve reporting compliance in this respect, it is still wise to loop in HR, legal, and accounting teams when formalizing a policy or individual agreement.

New policies should be added to onboarding and employee handbooks proactively before a need arises. This allows you to respond to employees’ concerns with a plan in place, rather than trying to create a solution in real time.

Both company-wide policies and individual advance paycheck agreements need to be issued in writing and formally agreed upon by both parties. Again, consider conferring with HR, legal, and accounting to ensure written authorization requirements and legal considerations are met.

Once a policy is approved and a payroll advance is issued, state-of-the-art account software like Intuit QuickBooks’ payroll solution can record agreements, track deductions, and maintain federal and state compliance at every step.

According to U.S. News, 43% of Americans would not be able to cover an unexpected expense of $1,000. Having a formal advance paycheck policy in place creates peace of mind and prevents hasty, reactive decision-making during emergencies.

Both parties play a role in making paycheck advances work smoothly. Here's what each side should understand before moving forward.

Employers must ensure every advance is properly approved, documented, and deducted in compliance with labor and tax laws. Transparency and consistency are critical, so employers should:

Loop in HR, payroll, or legal when needed. Doing so helps ensure that policies are applied fairly, funds are recovered appropriately, and risks are minimized.

Employees must follow company policy and fully understand the terms before accepting an advance. This protects them from surprises later, so employees should:

Ask questions early. If there’s uncertainty about how deductions work or what happens if employment ends, get clarity before signing. Being informed helps employees avoid added financial strain.

Instead of offering paycheck advances, you might explore options that give employees more control over their finances.

Earned wage access (EWA) platforms, like Payactiv or DailyPay, let workers access wages they've already earned before payday. These services often integrate directly with your payroll provider and reduce the need for short-term loans.

Earned wage access (EWA):

You can also offer financial wellness programs that include budgeting tools, credit counseling, and savings education. These programs encourage long-term planning and can reduce repeated financial stress.

Financial wellness programs:

Similarly, emergency savings programs help employees build a cushion through small, automated paycheck deductions, minimizing future reliance on advances.

Emergency savings programs:

Another option is partnering with a local credit union. These institutions often provide affordable loans and personalized financial support that employees can use during emergencies.

Credit union partnerships:

Compared to paycheck advances, these options can deliver greater financial stability without disrupting your company’s payroll or cash flow.

When employees feel more financially secure, they perform better at work. Around 58% of companieswith financial wellness programs report measurable productivity improvements linked to those initiatives.

When employees feel more financially secure, they perform better at work. Around 58% of companieswith financial wellness programs report measurable productivity improvements linked to those initiatives.

Payroll advances can relieve employees’ financial stress during times of need, adding a level of security that not only improves peace of mind but also workplace productivity. With employee wellness, job performance, and legal compliance all being major considerations, business leaders are turning to expert payroll software to improve their workflows.

Intuit QuickBooks can be used to create paycheck advance policies, track repayments, and monitor compliance at every turn. Learn more about our payroll software today.

Call Sales: 1-800-285-4854