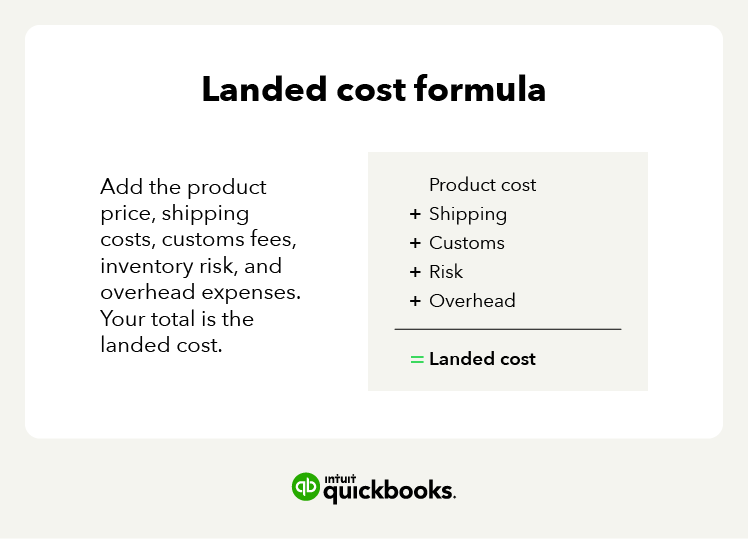

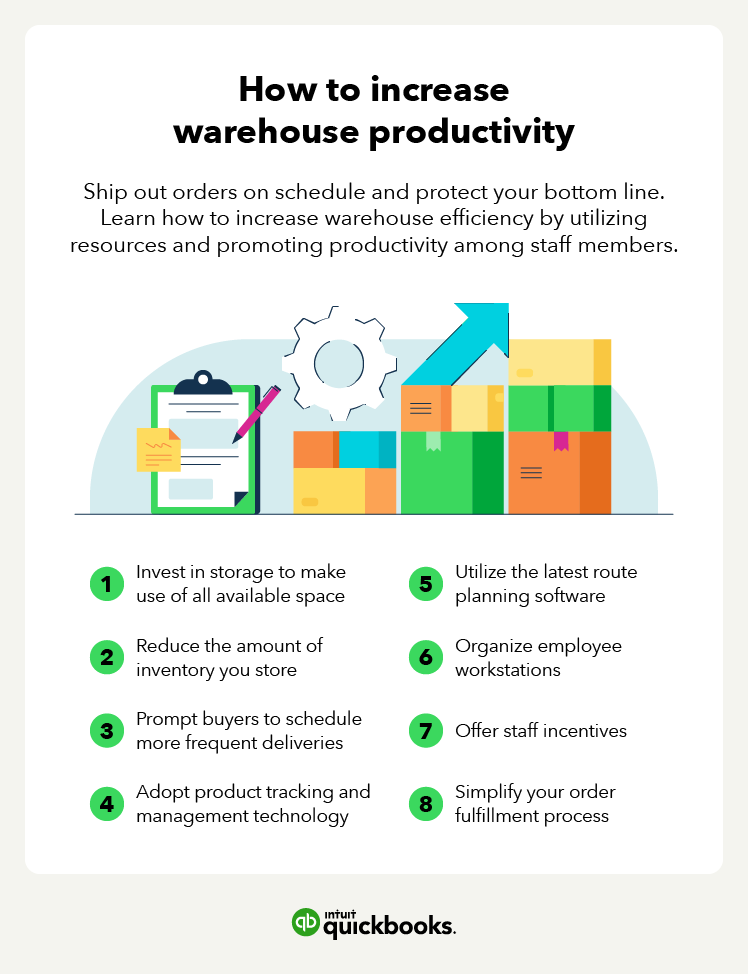

7 International shipping considerations

If you’re generating demand from countries outside of the U.S., consider variables like shipping, handling, insurance, and customs-related fees. To keep your customers happy, find the fastest, safest, and most affordable delivery option to ship your products.

Before you start shipping abroad:

- Create international shipping labels.

- Complete customs forms.

- Fill out electronic trade forms.

- Create origin country labels.

1. Freight shipping options

Any shipment that weighs more than 150 pounds is considered freight and generally costs a flat rate to ship. Shipments that weigh less than that are classified as parcels or less than truckload (LTL) and are priced by weight and package dimensions.

If you’re willing to send your packages separately, you may qualify for multiweight shipping and a lower price.

The most common ways for businesses to ship packages are by:

- Air

- Train

- Truck (TL or LTL)

- Ocean

2. Best shipping companies for small businesses

Finding a speedy and reliable shipping service that offers fair freight rates and won’t damage your products en route is a struggle most business owners are all too familiar with.

If you’re in the market for a cargo shipping service, try to form a relationship with a company that values communication, shipment safety, prompt delivery, customer service, quality tracking software, and professionalism.

Look into these shipping companies known for helping small businesses meet their goals and keep customers happy. These shipping companies are the best for:

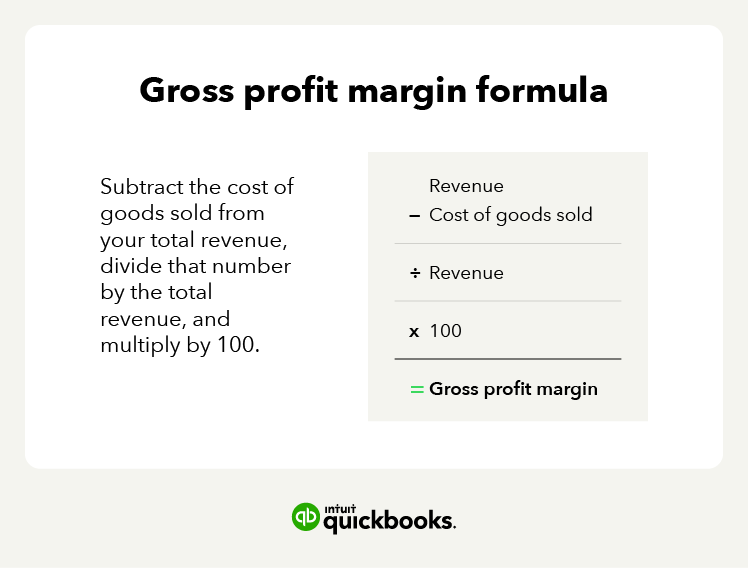

3. Import duties and taxes

Customs-related fees like import duties and taxes are in place to protect small and local businesses by making products coming in from outside of the country more expensive.

These policies also safeguard jobs, residents, the economy, and the environment from harm. Depending on the items you’re shipping and where you’re sending them, these fees can rise or fall drastically.

Most countries set import taxes and duties rates based on the following criteria:

- Product value

- Trade agreements

- Product manufacturer origin

- Harmonized System (HS) code

- Product description and purpose

- Regulations

Canada, Singapore, Australia, New Zealand, and countries in the European Union (EU) apply either a goods and services tax (GST) or a value-added tax (VAT).

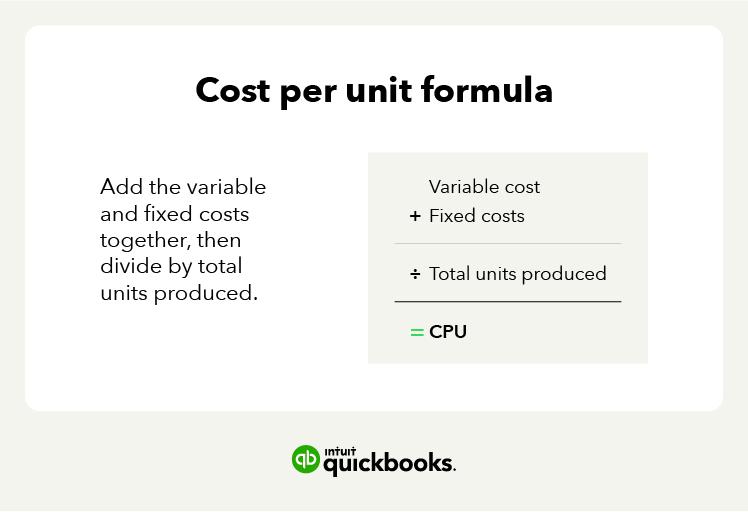

4. 263a regulations

More commonly known as Uniform Capitalization Rules or UNICAP, 263a mandates that taxpayers capitalize direct and indirect costs to property they produced or obtained.

This means that, as the taxpayer, you would need to record the cost of an expense over its lifetime to show depreciation and amortization on direct and indirect costs.

Costs that 263a requires to be capitalized include:

- Storage

- Handling costs

- IT

- Accounting

- HR

Anything that has a relationship to inventory production or the resale of an item should be documented on your company’s balance sheet. Taxpayers that are classified as a “small taxpayer” aren’t required to adhere to these statutes.

5. Cargo insurance and protection

International shipping insurance isn’t legally required, but it does protect you and the buyer in the event that the product you ship is damaged, lost, or stolen.

Most global trade carriers will automatically offer up to $100 USD of coverage. However, if you want additional financial protection, you will have to purchase it.

6. International shipping compliance guidelines

Before shipping your products out of the country, double-check that you are complying with U.S. federal regulations as well as those mandated by the country you will ship to.

Important compliance guidelines that you should consult include:

- Export Administration Regulations (EAR)

- International Traffic in Arms Regulations (ITAR)

7. Shipment fees and surcharges

Freight shipment fees are generally divided out by charges applied before main transit, during, and once the cargo reaches its final destination.

Additional charges that you may encounter include:

- Customs examination fee

- General rate increase (GRI)

- Courier and documentation fees

- Overweight container fee

- Container management fee

- LCL consolidation shipment fee

- Bunker adjustment factor (BAF)

- Emergency bunker surcharge (EBS)

- Currency adjustment factor (CAF)

- Peak season charge (PSS)

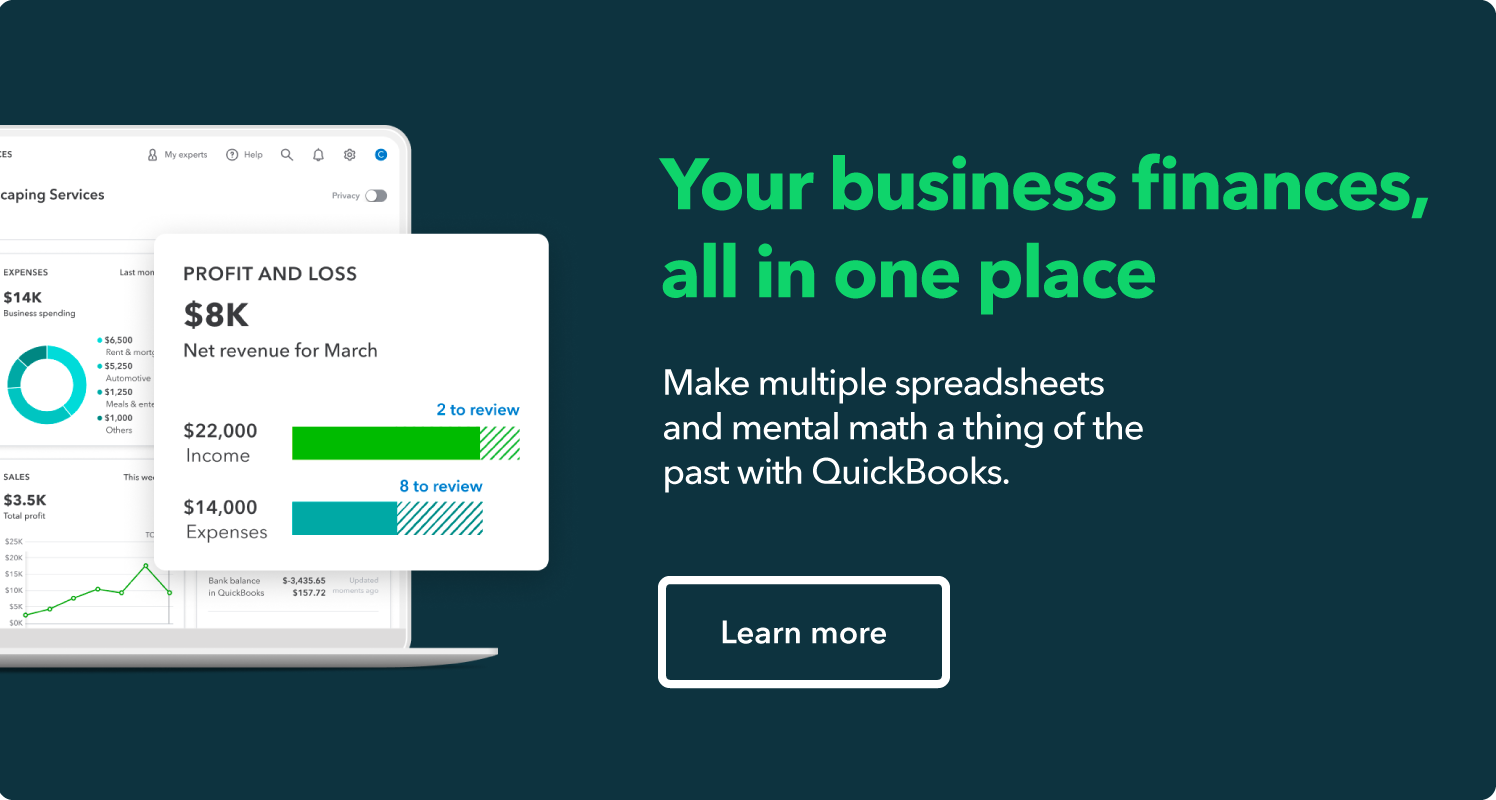

Take control of inventory management with turnover tracking software

Whenever you produce and distribute merchandise, you will encounter an untold number of business-related expenses.

Keeping a close eye on your costs allows you to act swiftly and with confidence based on the information from your accounting system. One of the best ways to reduce those costs is to carefully track your inventory in real time and to run inventory turnover ratio calculations regularly.