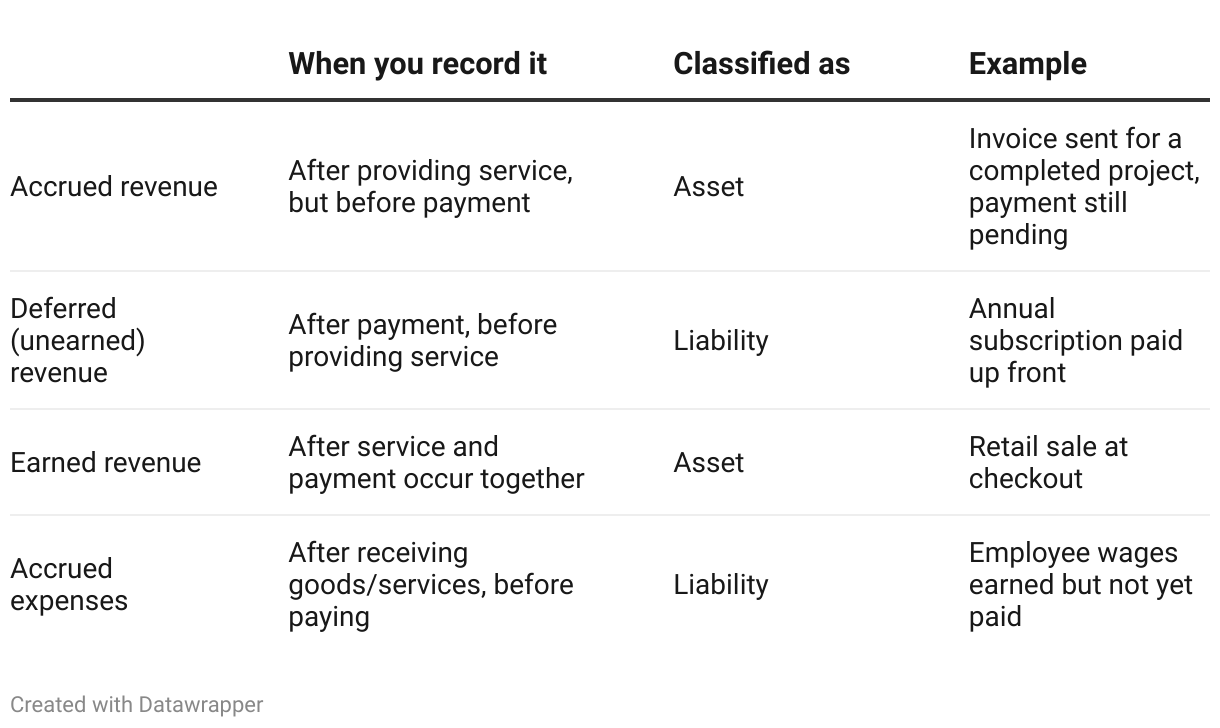

Accrued revenue vs. deferred revenue

You earn deferred revenue when customers pay for a service before you provide it. Accrued revenue uses the reversed process where payment follows a service.

So, while you recognize accrued revenue before receiving cash, you recognize deferred revenue afterward. Other differences include:

- Deferred revenue is a liability because you still need to earn it

- You can spread deferred revenue across multiple entries.

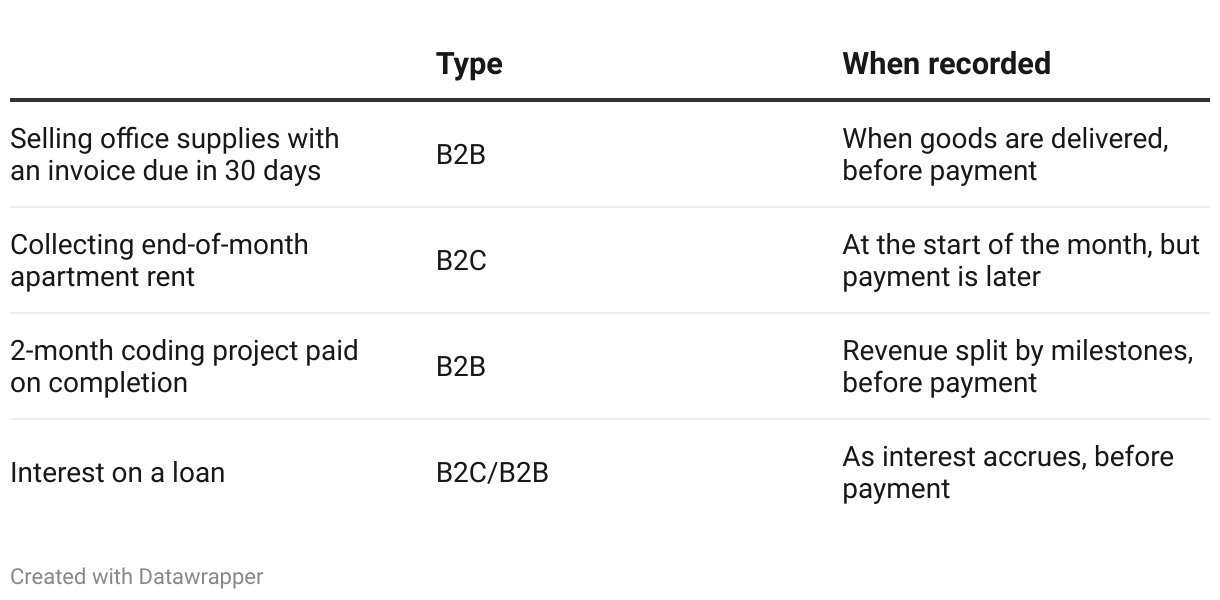

Example: A subscription service uses deferred revenue. Customers pay up-front for months or a year of access to a service. After a transaction goes through, the subscription begins.

Earned revenue vs. accrued revenue

Earned revenue refers to the money you get for providing a good or service. Unlike accrued revenue, you make earned revenue right after the transaction ends. Earned revenue is more common in retail and e-commerce.

- Earned revenue is an asset

- You record it after providing a service, the same time you earn the revenue

Example: Retail storefronts base their business model on earned revenue. When a customer chooses to leave with your product, they pay you at the same time you provide the good. With earned revenue, the monetary transaction and exchange of goods occur at once.

Unearned revenue vs. accrued revenue

Unearned revenue and accrued revenue work in opposite ways. You recognize unearned revenue when you receive payment for a service or product you haven’t provided yet.

On the flip side, you record accrued revenue when you’ve provided the service but haven’t received payment.

Unearned revenue is a liability because you still owe the service or product to your customer. As you fulfill the obligation over time, you gradually move this amount from unearned to earned revenue.

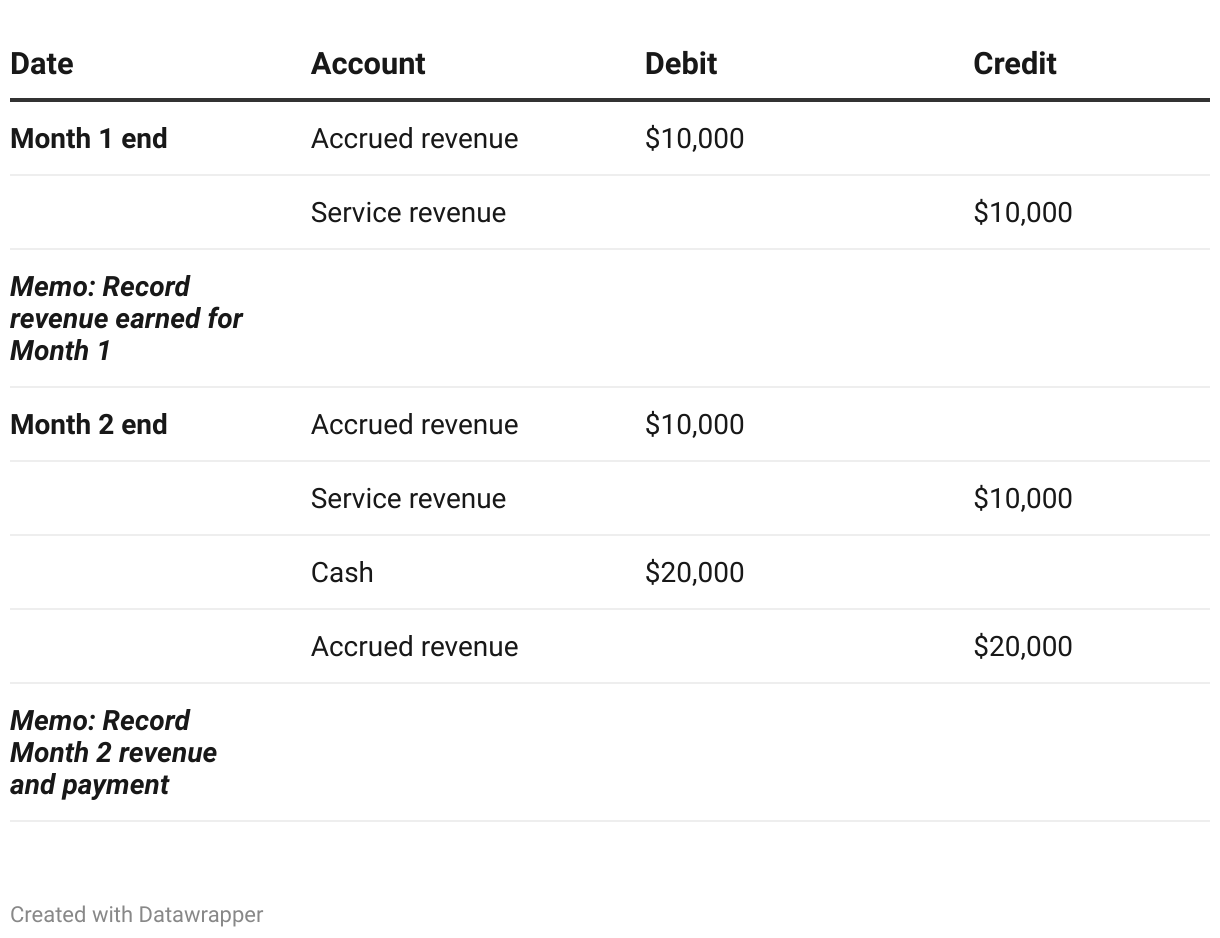

Example: If a customer pays for a one-year magazine subscription upfront, you record the payment as unearned revenue. As they receive an issue each month, you transfer a portion to earned revenue.

Accrued expenses vs. accrued revenue

Similar to accrued revenue, you record accrued expenses after incurring them. Unlike accrued revenue, an accrued expense refers to money a company owes, not income it’s due to receive. For example, purchasing goods from a supplier is an accrued expense until you pay the invoice.

- Accrued expenses are liabilities

- You record them upon incurring a charge and pay them later.

Example: Employee wages, bonuses, and commissions also count as accrued expenses. Because wages accrue in the period they occur but reach employees later, they're an accrued expense the company owes.

If you're still unsure how to manage the different revenue and expense types, consider using payment services to streamline accrual accounting in your business.