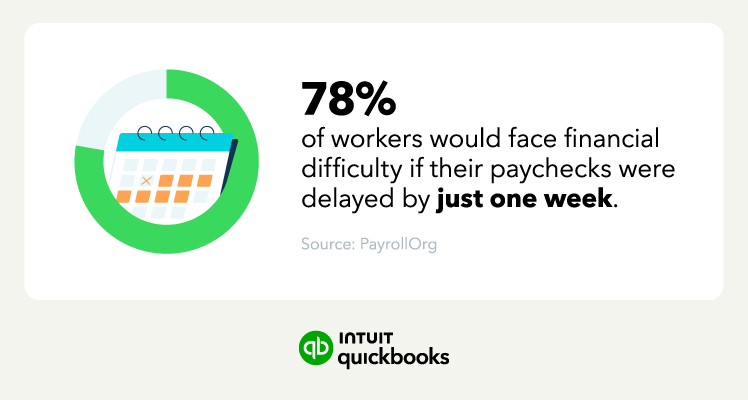

Running payroll in-house means you have to calculate staff wages and withholdings and file quarterly and year-end returns on time, every time. Getting it right matters because more than half of US workers would consider quitting their jobs if they kept getting paid late or incorrectly.

This administrative burden can be a hurdle; recent QuickBooks data shows that while nearly 78% of small business owners want to grow, only 45% are actually reporting growth. This gap suggests that many businesses need more help achieving their goals—starting with reclaiming time lost to back-office tasks.

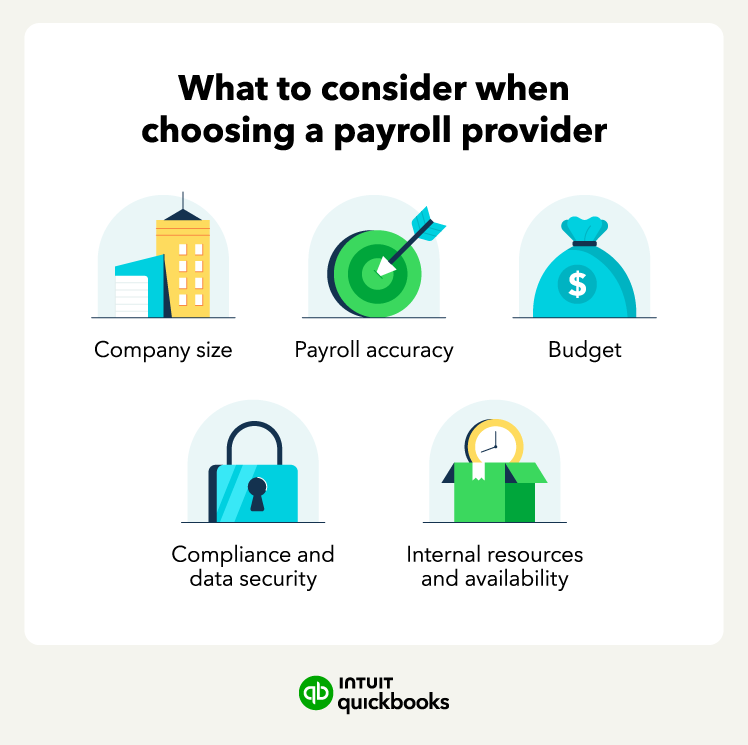

While outsourcing can relieve the workload, it costs money, and there are other trade-offs. Below, find out how in house payroll processing vs. outsourcing compares, the cost of each approach, and how to decide which is better for your business.

Jump to: