Nonprofit corporation

Nonprofit corporation: Mission-driven, tax-exempt status

Best for: Charities, educational institutions, religious organizations

Risk: Must meet strict compliance and reporting requirements

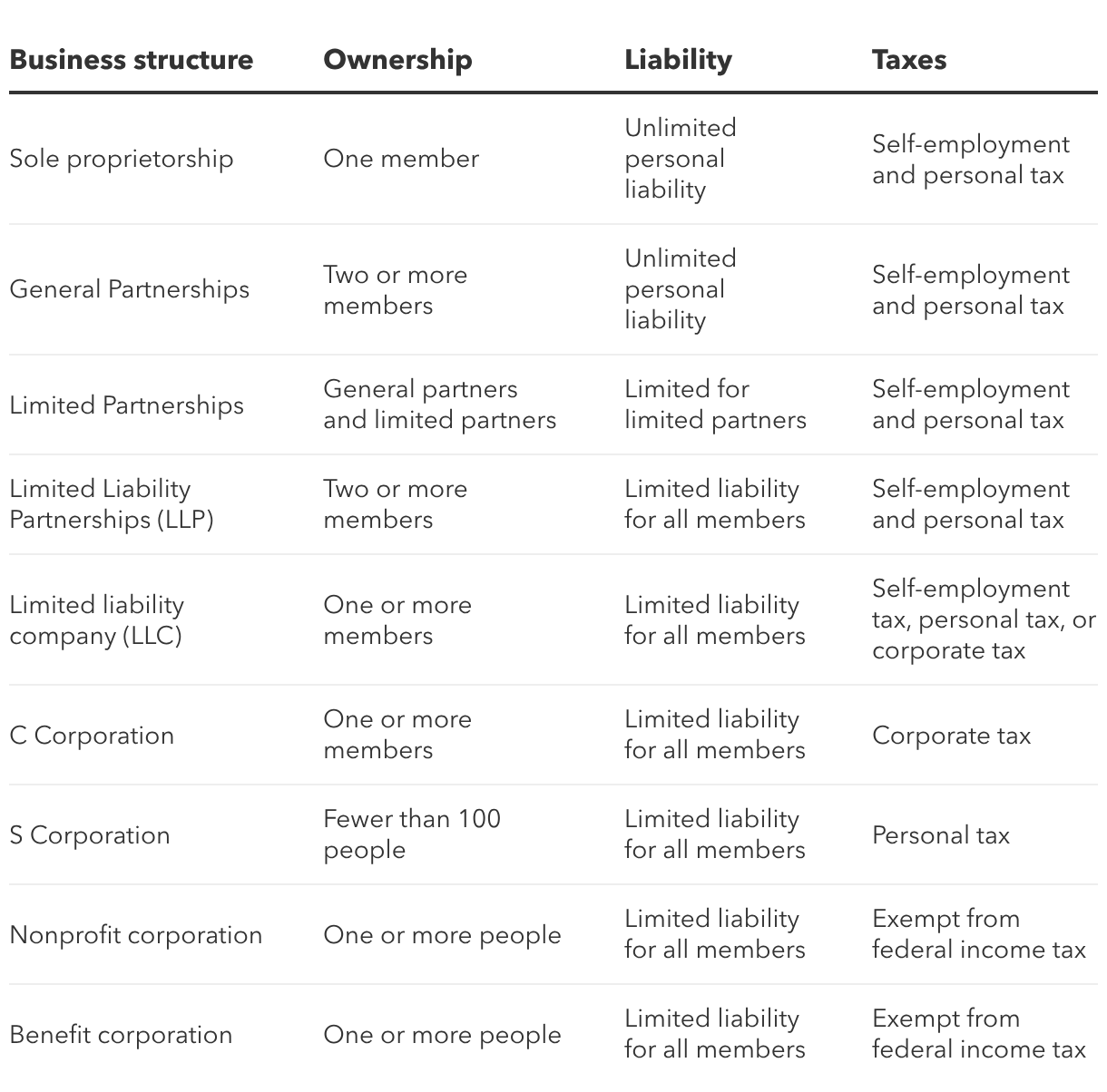

A nonprofit corporation is a legal entity formed to pursue a charitable, educational, religious, or other public benefit purpose without distributing profits to shareholders. These organizations rely on donations, grants, and earned income to sustain their operations.

Nonprofits are exempt from federal income tax and may qualify for state and local tax exemptions, but they must adhere to strict nonprofit accounting guidelines regarding their mission and financial practices.

Governance is typically structured around a board of directors, which oversees the organization's operations and ensures alignment with its mission. While nonprofits can generate revenue through various activities, they have to reinvest any surplus funds back into their core purpose.

Benefit corporation

In a nutshell: Profit with a purpose

Best for: Businesses with social or environmental missions

Risk: Additional reporting requirements

A benefit corporation is a for-profit entity legally required to consider its impact on employees, customers, and the environment. While still earning profits, it prioritizes social and environmental responsibility.

Benefit corporations prioritize their social or environmental mission. They are often certified by independent organizations to verify their commitment to public benefit. This legal structure appeals to socially conscious investors and consumers who seek to support businesses that align with their values.