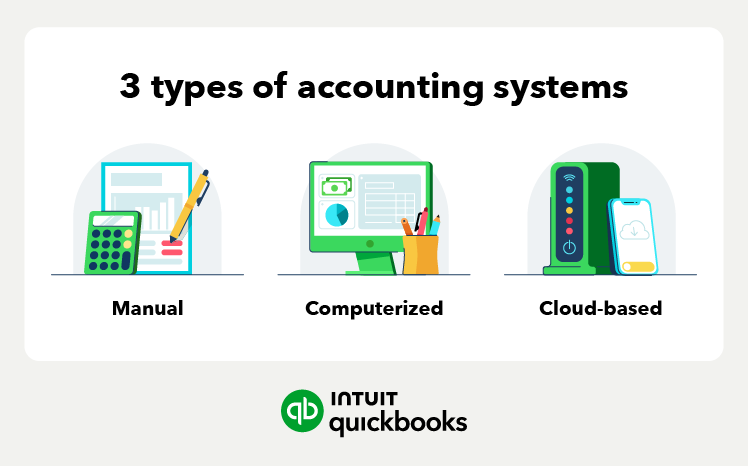

Manual

A manual accounting system is a pen-and-paper form of accounting. It involves recording transactions in a general ledger. Manual accounting is one of the oldest forms of bookkeeping, and it doesn’t require a computer, accounting software, or a complex system.

These systems use a physical (aka a general ledger). That ledger holds all the financial transactions, usually in chronological order. You will then add any new transactions to the ledger.

Running a manual system means keeping track of physical invoices and receipts. You’ll use them to enter transactions into the ledger and verify that transactions are accurate.

Manual accounting is straightforward, but it can also be time-consuming and less accurate than using software.

Computerized

Thanks to accounting software, computerized accounting systems have become more popular than manual systems. They help improve the efficiency of bookkeepers and business owners while improving accuracy.

A computerized accounting system is software that automates the bookkeeping process—from recording transactions to financial reporting. This type of software is also customizable. With computerized systems, transactions are quickly recorded and stored.

Additionally, such systems can allow you to automate various accounting tasks, such as processing payroll or managing accounts payable.