You could save up to 25% on transaction costs².

Speak with us now to see if you qualify.

Talk to sales 1-800-515-8366

Monday - Friday, 6 AM to 4 PM PT

Table of contents

Table of contents

Match your accounting records to your bank statements once a week, and you may be storing up trouble. In that intervening week, bank and loan fees could have been charged, a subscription you forgot to cancel could have been renewed, and a customer's deposit check could have bounced.

You think you have $10,000 in the bank, but it’s closer to $5,000. This can become a cash flow problem if you've got to cover payroll, rent, or a supplier invoice that same week.

Below, find out about bank reconciliations, why they’re important, and how to stay on top of them for your business.

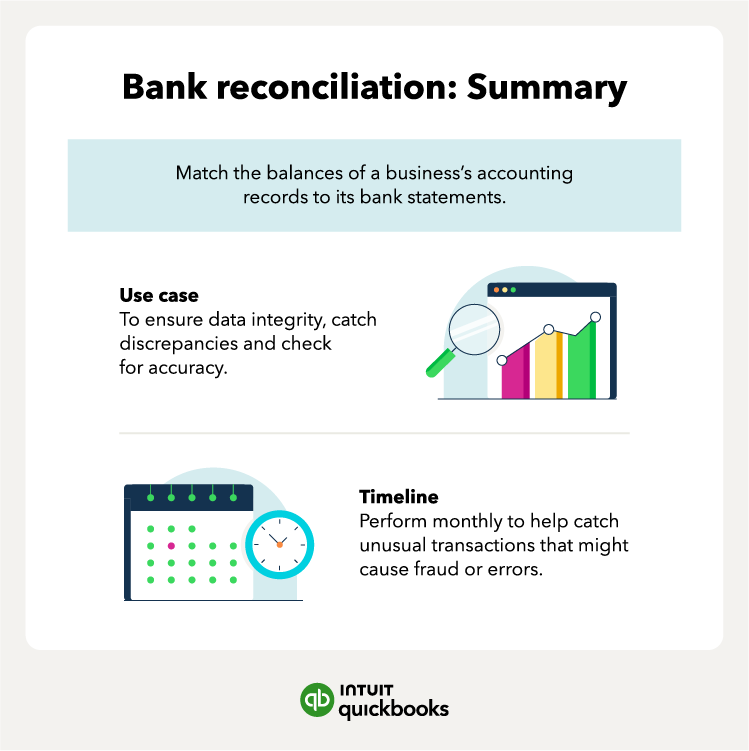

A bank reconciliation statement is a record that compares the money in your internal financial records to the money in your bank account, so you can see what's different and how to fix it.

The goal of using this document is to identify and resolve any discrepancies, such as a payment entered for the wrong amount and a deposit that the bank hasn't processed yet. That way, you have an accurate picture of your company's cash position.

Bank reconciliation is a financial health check for your small business finances. Here are five reasons it matters:

Without reconciliation, errors pile up, fraud goes unnoticed, and the reports you depend on become unreliable.

Contact your bank right away if you spot a transaction you don’t recognize when reconciling your accounts. The sooner you let them know, the more likely you are to recover the money.

Prepare properly for your reconciliation, and it shouldn't take that much time to complete. Here's how to do a bank reconciliation in six steps:

Before you get started, pull together all your bank statements for the period, your accounting records or software register, and any supporting documents like receipts or check stubs.

Make sure you have the opening and closing balances for the period on hand before you start. Your opening balance should match the closing balance from your last completed reconciliation. Your closing balance is the final balance shown on this period’s bank statement.

Go through your bank statement line by line, matching each transaction to an entry in your accounting records. Check off each transaction that appears in both places and investigate any that only appear in one.

Outstanding transactions are entries in your books that haven't appeared on the bank statement yet, as a result of processing delays or timing differences. Examples of outstanding transactions include:

These are normal, nothing to worry about, and usually just timing differences.

Anything that doesn't match and isn't a timing difference needs further looking into.

Here's what to look for:

Once you know something isn’t matching, update your accounting records. You'll either need to add something you missed, like interest the bank paid you, or subtract deductions you hadn't recorded, like a bank fee or a bounced check charge.

Make these changes in your accounting software, and not on the bank statement.

Your adjusted bank balance is your bank statement total after you account for outstanding transactions from Step 3. Your adjusted book balance is your records total after the corrections you made in Step 5. Check that these two figures are equal.

If they don't match, go back through Steps 2 to 5 to find what you missed.

Regular bank reconciliation means you can rely on the figures in your accounts. That’s important because it means:

Here's a simple three-step bank reconciliation example for a small retail business reconciling its checking account for March.

Start by comparing your book balance with the balance on your bank statement.

Now, adjust the bank balance for transactions you've already entered that haven't cleared the bank yet.

Then, adjust your book balance for anything the bank has charged or credited that isn't in your books yet.

Both adjusted balances now match at $12,250.00, so the shop owner has completed the reconciliation.

Reconciliation is an important part of running a business, but with the right approach, it won’t take too much time for you to complete.

Follow these four tips for a quick and accurate turnaround:

Reconcile at least once a month. If your business handles a lot of transactions, do it every week.

The longer you leave it, the more transactions pile up and the harder it is to remember exactly why there's a difference between your records and the bank.

Accounting software like QuickBooks Online takes a lot of the manual work out of reconciliation. It matches many transactions automatically and asks for suggestions when it doesn’t, or when it spots a discrepancy.

QuickBooks Online’s AI makes reconciliation even faster, a big help for businesses that handle a lot of transactions each month.

Connect your bank account to QuickBooks, and reconciliation can take minutes. Use a bank reconciliation template for any accounts not yet connected to your accounting software.

It’s important to file your bank statements, receipts, and supporting documents as they come in. Otherwise, you’ll spend a lot of time hunting for them later, and you may not find everything you need.

Set up a simple physical or digital folder structure organized by month and account.

Bank feeds, which sync your bank account directly with QuickBooks, reduce manual data entry. Automated rules can categorize recurring transactions, greatly speeding up the process.

Automation and AI save you time, but you should check the results. Someone still needs to confirm everything looks right because you know your business better than anyone.

A lack of regular bank reconciliation means you miss both smaller errors, like a missed bank fee, and bigger ones that affect your business, like a payment you’re relying on not clearing. Automatic reconciliation frees up your time, gives you confidence in the accuracy of your financial statements, and puts you in control of your cash.

QuickBooks Online accounting software reconciles your accounts automatically every time there’s a new transaction and spots problems faster.

Call Sales: 1-800-285-4854