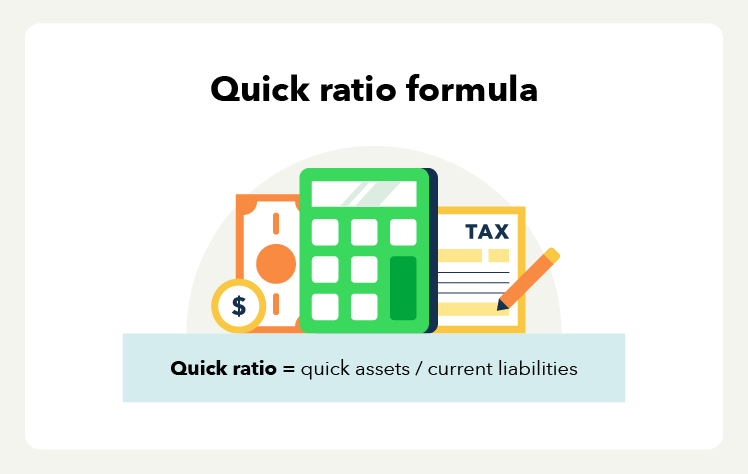

The quick ratio formula is quick assets divided by current liabilities. It’s also known as the acid-test ratio and is worth learning—no matter your industry. The quick ratio helps you track your liquidity, which is your ability to pay bills in the short term. Using the quick ratio can help you avoid cash flow problems and maintain good relationships with your creditors and suppliers.

This article will explain how to calculate the quick ratio and provide tips on improving liquidity. Here’s what we’ll dive into:

- What is the quick ratio?

- Quick ratio example

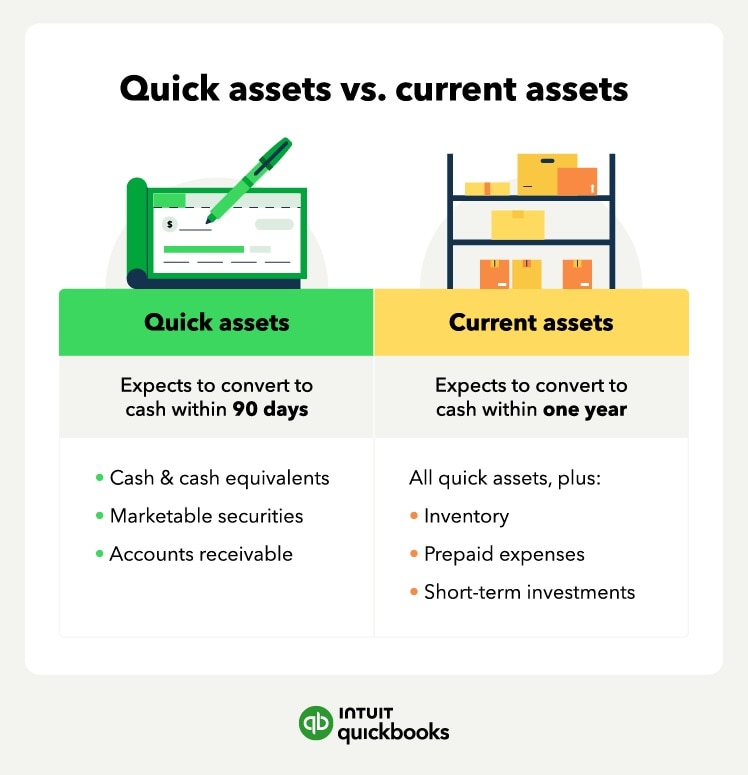

- Components of the quick ratio

- Quick ratio vs. current ratio

- Why is the quick ratio important?

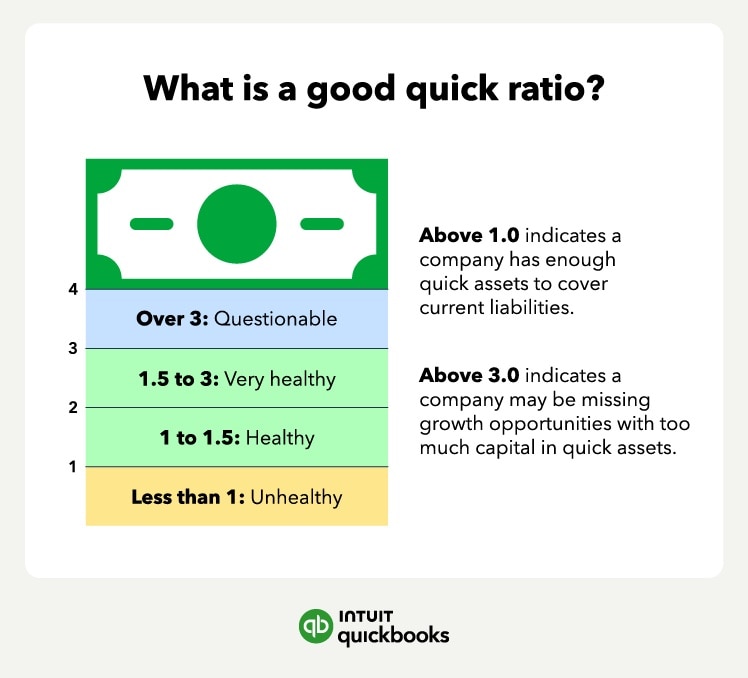

- What is a good quick ratio?

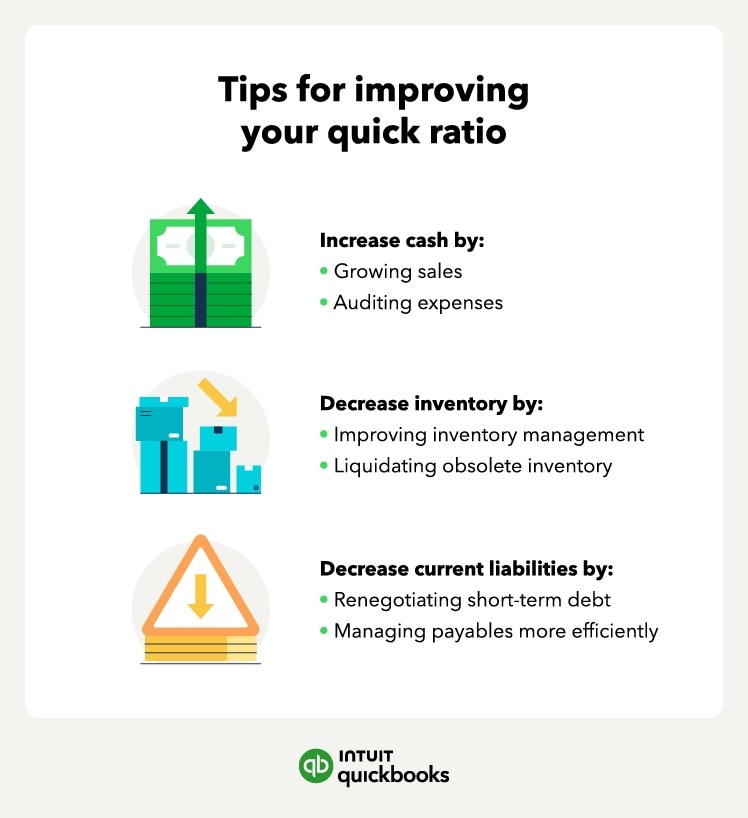

- How do you improve your quick ratio

- Your toolkit for managing liquidity

The higher the quick ratio, the more financially stable a company tends to be, as you can use the quick ratio for better business decision-making.