When you’re exploring financing options for your business, one of the first questions that often comes up is whether lenders will review your personal credit score. For many small business owners, especially those seeking a business loan or line of credit, the answer depends on several factors, including your business structure, how long you’ve been operating, and your overall financial history.

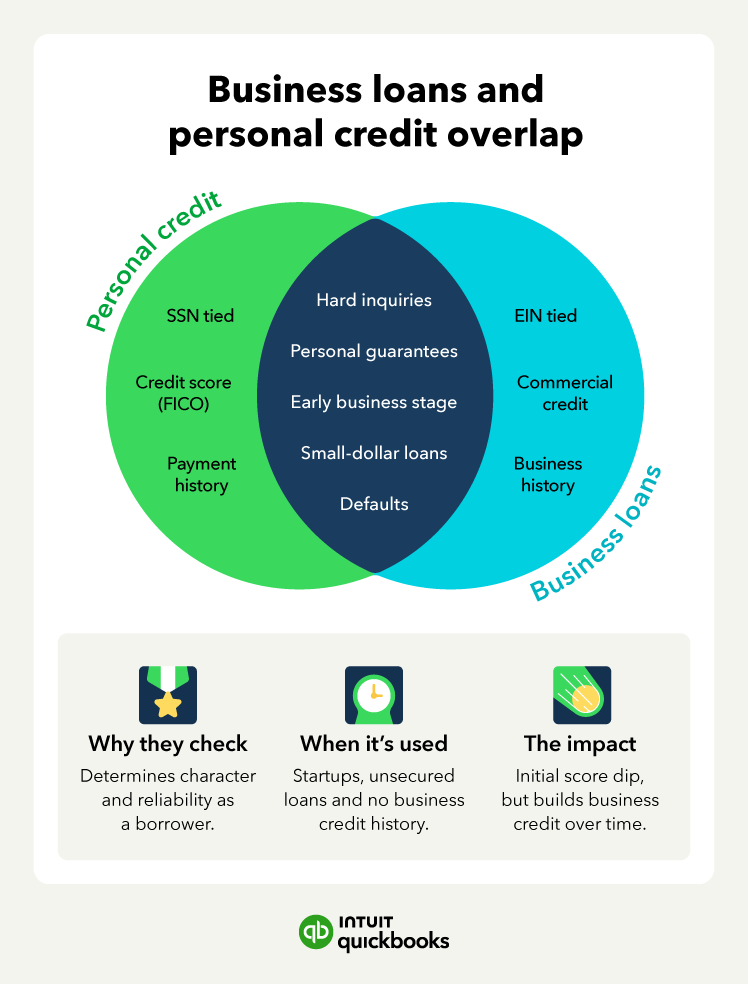

Personal credit and business credit are closely connected, particularly in the early stages of a business. While your company may have its own revenue, expenses, and cash flow, lenders often look to the owner’s financial profile to fill in gaps when business data is limited. Understanding how personal credit and business credit interact can help you prepare before applying and reduce surprises during the lending process.

Access to capital remains top of mind for many owners. According to the 2025 Intuit QuickBooks Small Business Financing Report, 65% of small businesses plan to invest in their growth. As businesses look to expand, hire, or stabilize cash flow, understanding lending requirements, including credit considerations, becomes an important part of financial planning.

- The short answer: Most business loans do involve personal credit

- Why lenders check personal credit for business loans

- Do QuickBooks Capital loans use personal credit?

- Types of business loans and how credit is evaluated

- When business credit matters more than personal credit

- How to protect your personal credit when borrowing for business

- Alternatives if your personal credit needs improvement

- The bottom line