Advantages of using bridge loans

Business bridge loans fill cash flow gaps, allowing companies to navigate lean periods, pursue growth opportunities, or make strategic investments.

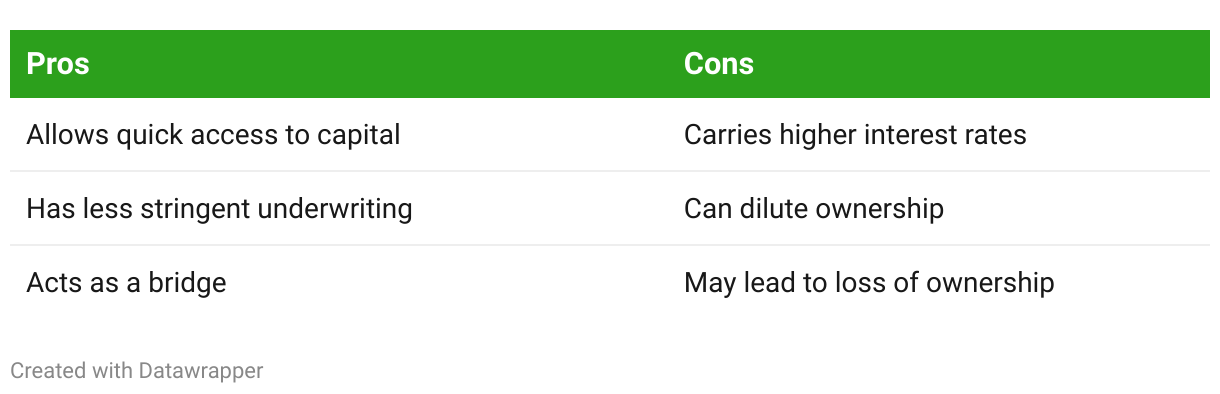

The biggest advantages for businesses include:

- Quick access to capital: Businesses can take advantage of time-sensitive opportunities or cover unexpected expenses.

- Less stringent underwriting: Compared to traditional bank loans, bridge loans have less rigid requirements, making them accessible to businesses with less-than-perfect credit.

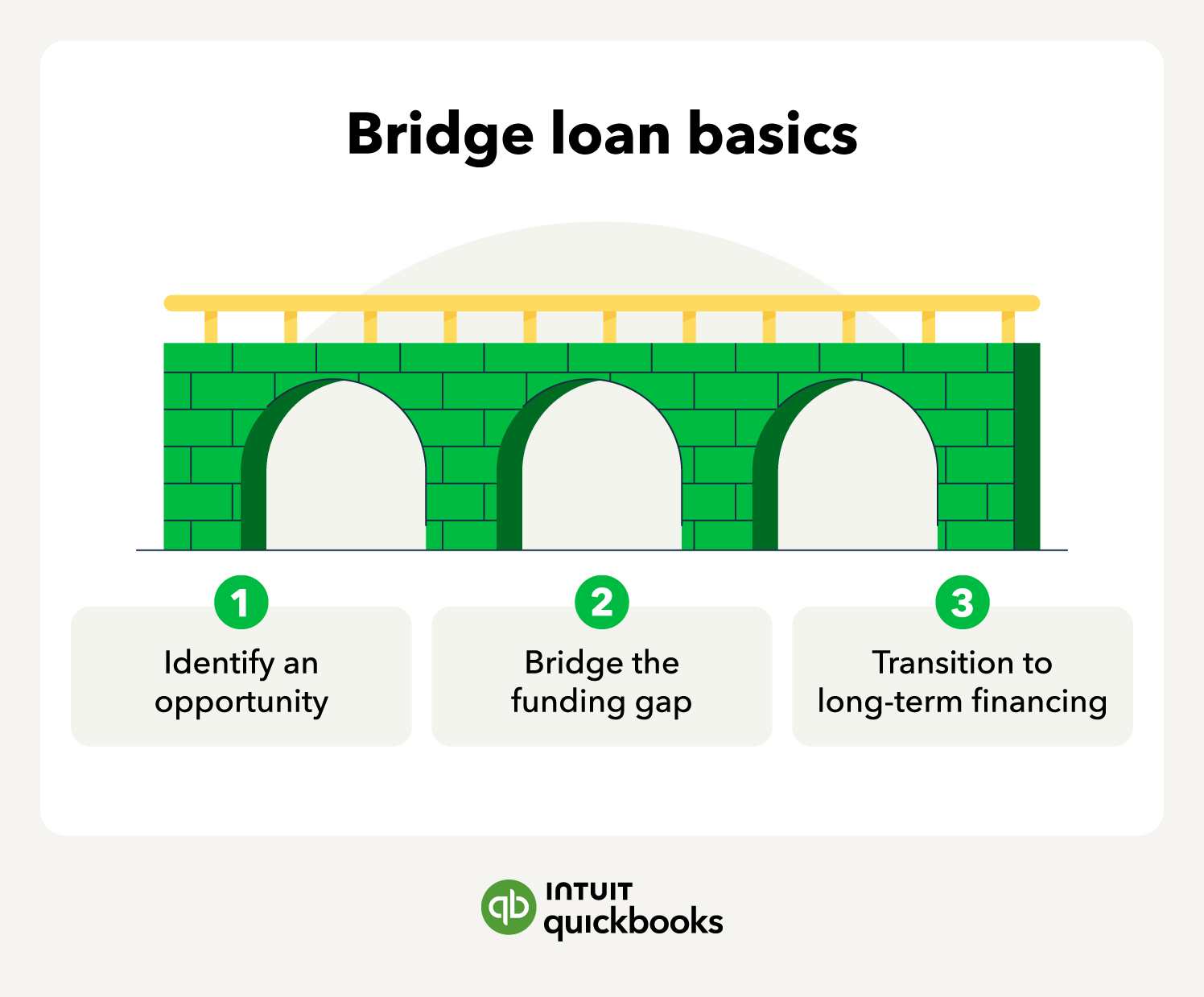

- Provides a bridge: These loans can help businesses maintain operations and cash flow during transitional periods, such as when waiting for a larger loan or investment.

Bridge loans are short-term and typically require repayment within a year. This can create financial pressure for businesses if long-term financing is not secured within the expected timeline. A bridge loan can also help an SMB act fast on time-sensitive deals.

Example: A machine shop owner spots a CNC line at an excellent price during a receivership sale. (A CNC line is a set of machines that cut and shape metal parts with high precision.)

The seller needs payment within five days, but the bank can’t move that fast. So the machine shop owner takes out a six-month bridge loan, buys the equipment, and repays the loan by refinancing with a standard equipment finance facility. By acting quickly, the shop expands production capacity, wins new contracts, and increases revenue.

Disadvantages of using bridge loans

Business bridge loans can be a risky financial strategy. The main drawbacks include:

- Higher interest rates: Debt bridge funding often comes with higher rates due to its short-term nature.

- Dilution: Bridge loans may require issuing equity or convertible securities, which can dilute existing shareholders’ ownership stakes.

- Possible loss of ownership: There is a risk of default if the business can’t secure long-term financing and repay the loan on time, resulting in the loss of ownership or key assets.

For example, consider a home-goods store that signs a lease and takes out a nine-month bridge loan to fund the deposit and permits. The plan is to open by month six and pay off the loan with the first three months of sales. However, inspections and contractor delays push the opening to month nine.

With no revenue, there isn’t enough cash to make the final payment. The owner pays for an extension and refinances on tighter terms, raising the total cost. The extra fees and higher interest eat into profits for months after opening.

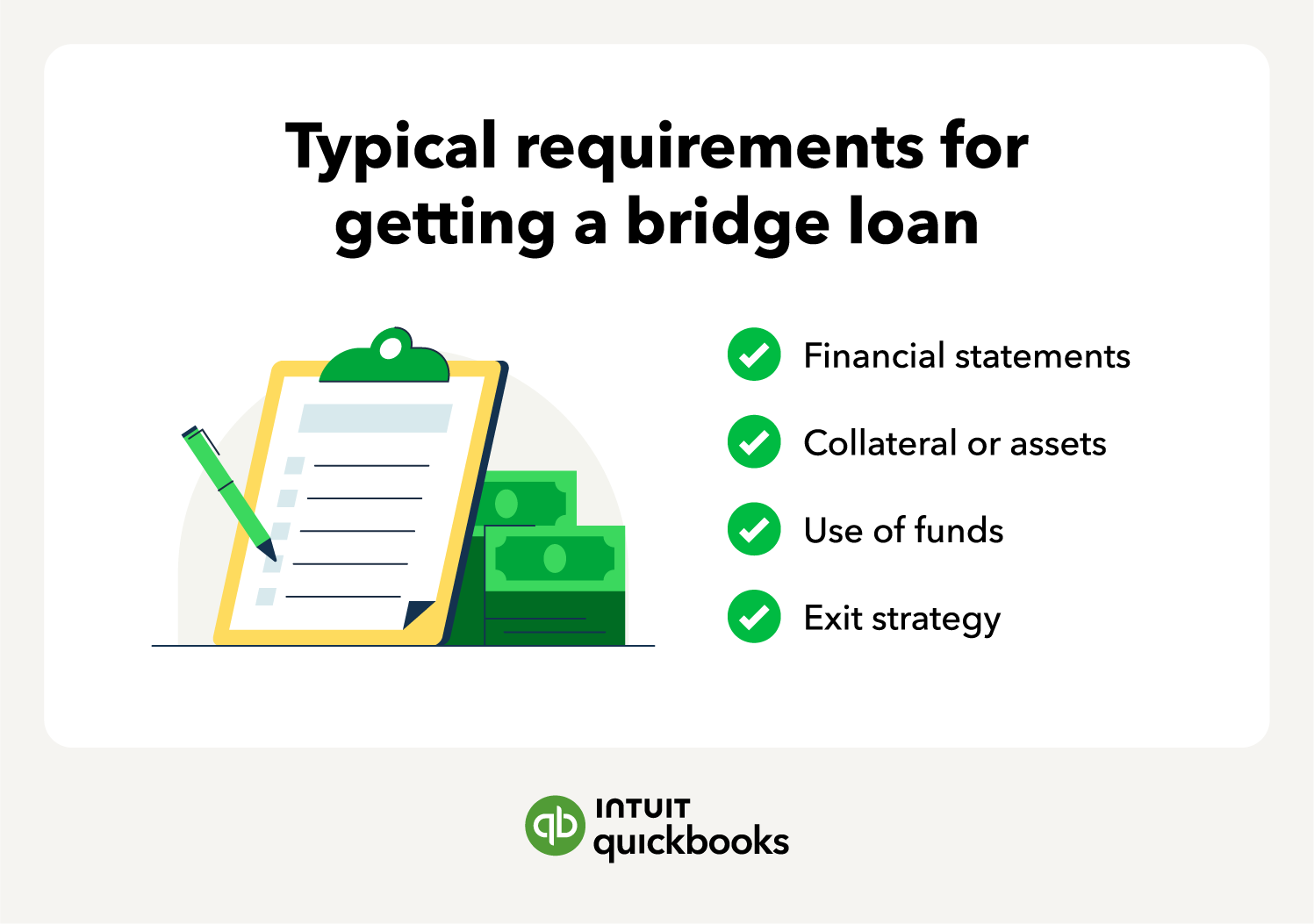

Business owners may need to provide a personal guarantee, making them personally liable for the loan if the business can't repay it. A personal guarantee is a legal promise you make to repay the outstanding balance on a loan if your business can’t. Depending on the agreement, this may give lenders the right to seize personal assets, such as savings and property.

Business owners may need to provide a personal guarantee, making them personally liable for the loan if the business can't repay it. A personal guarantee is a legal promise you make to repay the outstanding balance on a loan if your business can’t. Depending on the agreement, this may give lenders the right to seize personal assets, such as savings and property.