You could save up to 25% on transaction costs².

Speak with us now to see if you qualify.

Talk to sales 1-800-515-8366

Monday - Friday, 6 AM to 4 PM PT

Table of contents

Table of contents

Every business has a number on its financial statements that shows whether you're building wealth or standing still. That figure is the “owner’s equity” and it shows the value left in your business after you deduct all of its liabilities from its assets.

The good news is that once you understand how to calculate owner’s equity, you can take action to increase it.

Owner's equity is the financial stake you, as a business owner, have in your business. It’s the value that belongs to you, not your lenders or creditors.

Let’s say you run a landscaping business. You have $80,000 in equipment, vehicles, and cash, as well as $30,000 in outstanding loans. That means your owner’s equity is worth $50,000.

Owner's equity matters because it shows whether your business is building value over time or losing ground. Track it from one period to the next, and you have a useful reference point for deciding whether to take on debt, pull back on spending, or reinvest in growth.

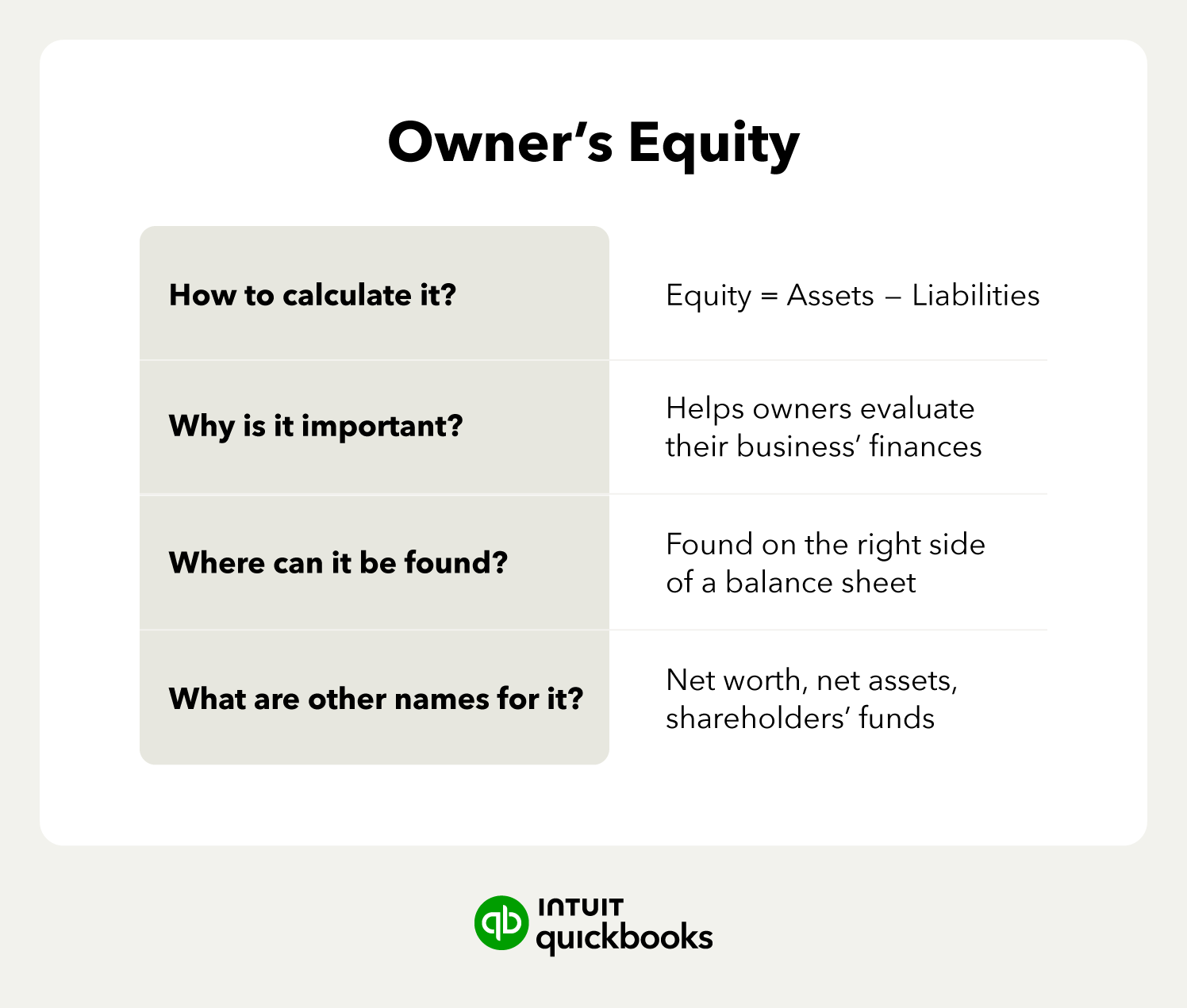

The formula for calculating owner’s equity is:

Here’s how to do it:

For example, say your business has $150,000 in assets and $90,000 in liabilities. That would mean your owner's equity is $60,000.

These figures come directly from your balance sheet, so if your finances are up-to-date and current, working out owner’s equity is straightforward.

You need to know the difference between an asset and a liability to find your owner's equity.

An asset is anything your business owns that has value. A liability is anything your business owes to others.

Here are common examples of each:

Add up everything in the assets column, then subtract everything in the liabilities column to determine owner’s equity.

To make sure you're counting the right things when you calculate your equity, learn the difference between assets and expenses.

For example, a delivery van would be an asset because it retains value and the business owns it outright, but a monthly fuel bill wouldn't be because it's a running cost with no lasting value on the balance sheet.

To make sure you're counting the right things when you calculate your equity, learn the difference between assets and expenses.

For example, a delivery van would be an asset because it retains value and the business owns it outright, but a monthly fuel bill wouldn't be because it's a running cost with no lasting value on the balance sheet.

Here’s how owner’s equity can change over time in small businesses:

A photographer sets up as a sole proprietorship and invests $40,000 of their own money into cameras, lighting, and a laptop. They take out no debt to get started, so they don’t owe anything.

After two years, the photographer decides to borrow $15,000 to buy studio equipment. Their assets increase, but so do their liabilities by the same amount. The $15,000 studio equipment goes in both the assets column and the liabilities column.

Now in Year 5, the studio equipment has paid off in strong bookings. The owner has built up $25,000 in retained earnings that they’ve left in the business rather than withdrawing. The growth in owner’s equity has come entirely from profit staying in the business.

The value of owner’s equity changes over time based on the business's performance.

Here are four ways to increase it:

Higher profits flow into retained earnings, which directly grow equity without you having to invest any additional cash.

The main ways to improve your profit margin include increasing revenue, negotiating discounts with suppliers, and adjusting your pricing.

Even small, consistent improvements to your profit margin add up in your equity over time in a way that one good month rarely does.

Taking less out of the business in the short term builds equity. Every dollar of profit you leave increases the size of your stake in the company.

Reinvesting in assets like equipment or inventory also strengthens the asset side of the accounting equation. While it does not grow equity on its own, it can help you build additional profit that you can retain.

Calculating your retained earnings at the end of each period shows you exactly how much of your profit is staying in the business and building your stake.

Calculating your retained earnings at the end of each period shows you exactly how much of your profit is staying in the business and building your stake.

Paying down debt shrinks the liability side of the equation, which increases equity even if assets stay the same.

That’s because shrinking the liability side of the equation has exactly the same mathematical effect as growing your assets.

New debt is worth taking on only when the revenue it generates clearly outweighs what it costs. Otherwise, it reduces your equity without adding lasting value to the business.

Every draw you take reduces your equity by the same amount. Taking out more than planned on top of your regular salary can quietly erode your stake, even in a profitable year.

Setting a consistent draw tied to your business's actual performance means you're building equity as a habit rather than spending it by default.

A statement of owner's equity is a financial report that shows how your equity changed over a set period. It includes your starting equity, adds any net income, and then subtracts owner draws to determine your closing equity.

While your income statement shows whether the business made a profit, the statement of owner's equity shows what that profit did to your stake.

It's typically prepared at the end of each accounting period, either monthly, quarterly, or annually. The statement connects to your balance sheet, income statement, and cash flow statement, so you can see the full picture of your business's financial standing.

You'll find this statement most useful when you're:

Reviewing your statement of owner's equity each period is one of the easiest ways to track progress toward your long-term growth goals.

Owner's equity provides a snapshot of your business's financial health, but it's only as reliable as the records behind it. Accurately record your assets, liabilities, and draws so you can track how your stake in the company changes over time.

QuickBooks Online automatically updates your balance sheet and other financial statements with every new transaction, so your equity position is always current. And if you ever need help, you can partner with Intuit Experts for accounting and bookkeeping support.

Disclaimer:

*QuickBooks Term Loan and QuickBooks Line of Credit loans are issued by WebBank.

Call Sales: 1-800-285-4854