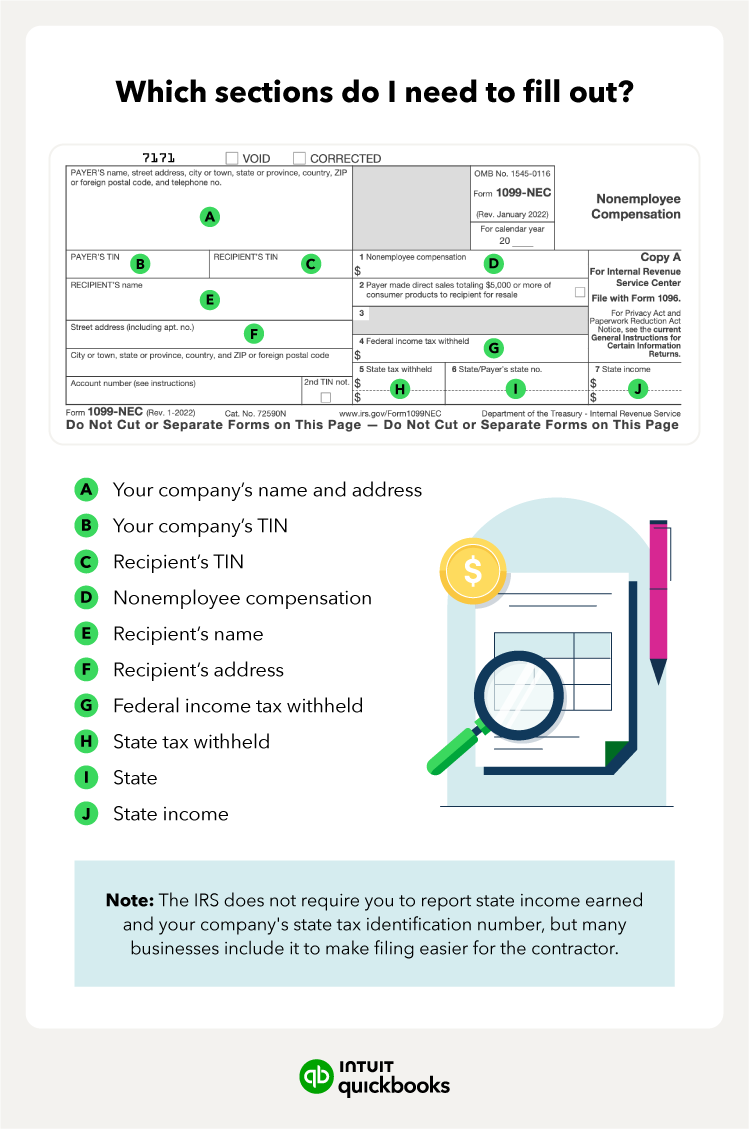

Tax season can be a bit more complex for freelancers and small businesses that hire independent contractors. Instead of the familiar W-2 forms, you'll be dealing with 1099 forms. More specifically, the 1099-NEC. This form is essential for reporting payments you’ve made to nonemployees—getting it right is crucial.

This guide will cover everything you need to know about the 1099-NEC, from identifying which workers qualify as independent contractors to correctly filling out and submitting the form. We'll even cover how to file online and what to do if you make a mistake.