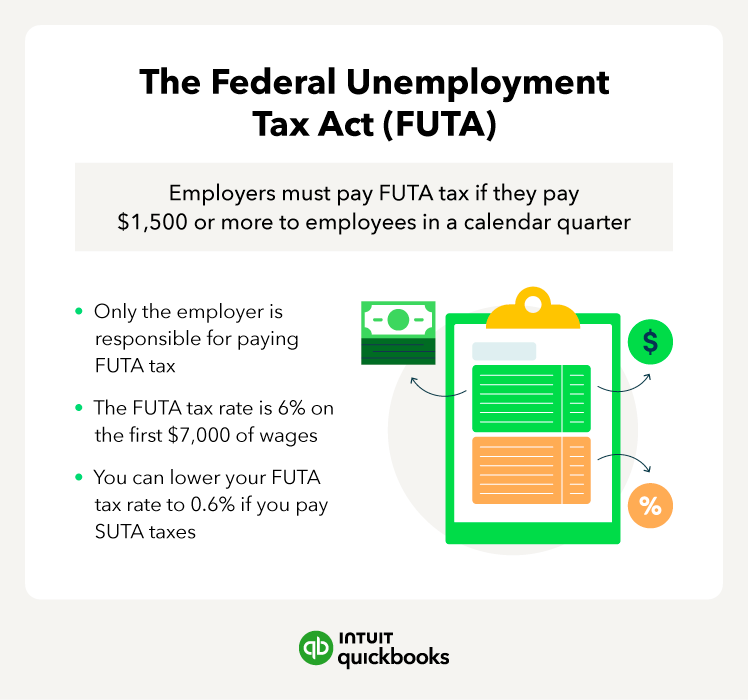

According to QuickBooks’ Entrepreneurship in 2025 report, 54% of people said they're thinking of starting a business. But with the excitement comes the responsibility of understanding tax obligations and important dates, including the Federal Unemployment Tax Act (FUTA).

When you lose your job, you might rely on unemployment benefits to provide temporary income support while you search for a new job or explore new opportunities. These benefits are funded by a payroll tax called the Federal Unemployment Tax, which is paid by employers.

Below, we'll cover what FUTA is, why it's important, and how to calculate it. We'll even give you some tips on how to effectively manage FUTA taxes as a small business owner.

Jump to:

- What is FUTA?

- What is the FUTA tax rate for 2026?

- FUTA vs. SUTA taxes

- FUTA vs. FICA

- Who has to pay FUTA tax?

- Who is exempt from paying FUTA tax?

- How to calculate FUTA taxes

- How do you file and pay FUTA taxes?

- FUTA tax deadlines for 2026

- Best practices for meeting your FUTA obligations

- Find peace of mind come tax time