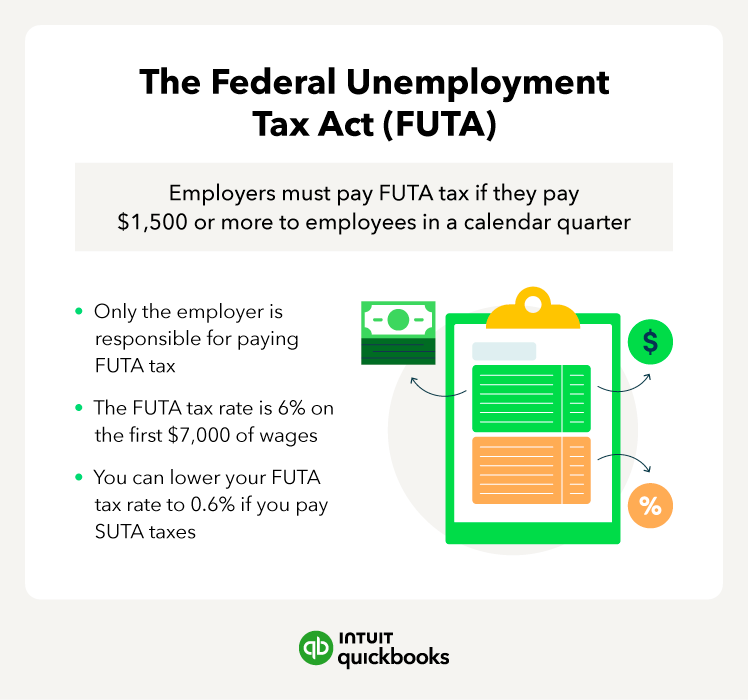

How to calculate FUTA taxes

Calculating FUTA taxes is a straightforward process. If everyone at your company earns more than $7,000 per year, the basic equation for determining FUTA tax is as follows:

$7,000 x 0.06 x Number of employees = FUTA tax liability

For example, let’s say you run a company with 20 employees, each of whom earns $50,000 per year.

Since everyone makes over $7,000 per year—and FUTA tax only applies to the first $7,000—we can calculate your company’s FUTA payroll liability with the following formula:

$7,000 x 0.06 x 20 = $8,400

Your company’s FUTA tax liability is $8,400. Depending on the state your business is in, you may also owe state unemployment taxes and get a credit to lower your FUTA tax rate.

Your equation will differ if you have one or more employees who make less than $7,000.

Let’s say you run a company with 10 employees—eight employees earn $40,000, one earns $6,500, and one earns $4,000.

Here’s how to calculate your FUTA taxes if you have a mixture of employees making above and $7,000 a year:

1. Calculate your liability for eight employees making over $7,000, which is $7,000 x 0.06 x 8 = $3,360.

2. Calculate your liability for your employee making $6,500, which is $6,500 x 0.06 = $390.

3. Calculate your liability for your employee making $4,000, which is $4,000 x 0.06 = $240.

4. Add up each to get your total liability of $3,990.

Depending on the state your business or employees are in, you may also owe state unemployment taxes.