You could save up to 25% on transaction costs².

Speak with us now to see if you qualify.

Talk to sales 1-800-515-8366

Monday - Friday, 6 AM to 4 PM PT

Table of contents

Table of contents

Taking on more work is a sign your construction business is growing—but it also introduces new financial pressure. Costs hit faster, timelines overlap, and small gaps in visibility can quickly impact margins. One job may be ahead while another falls behind or uses more cash, making it harder to stay balanced. What worked for a few jobs doesn’t hold up the same way as volume increases.

Managing multiple projects successfully comes down to having the right structure in place. With standardized processes, reliable financial data, and clear oversight, you can stay on top of performance, protect profitability, and make better decisions as you grow.

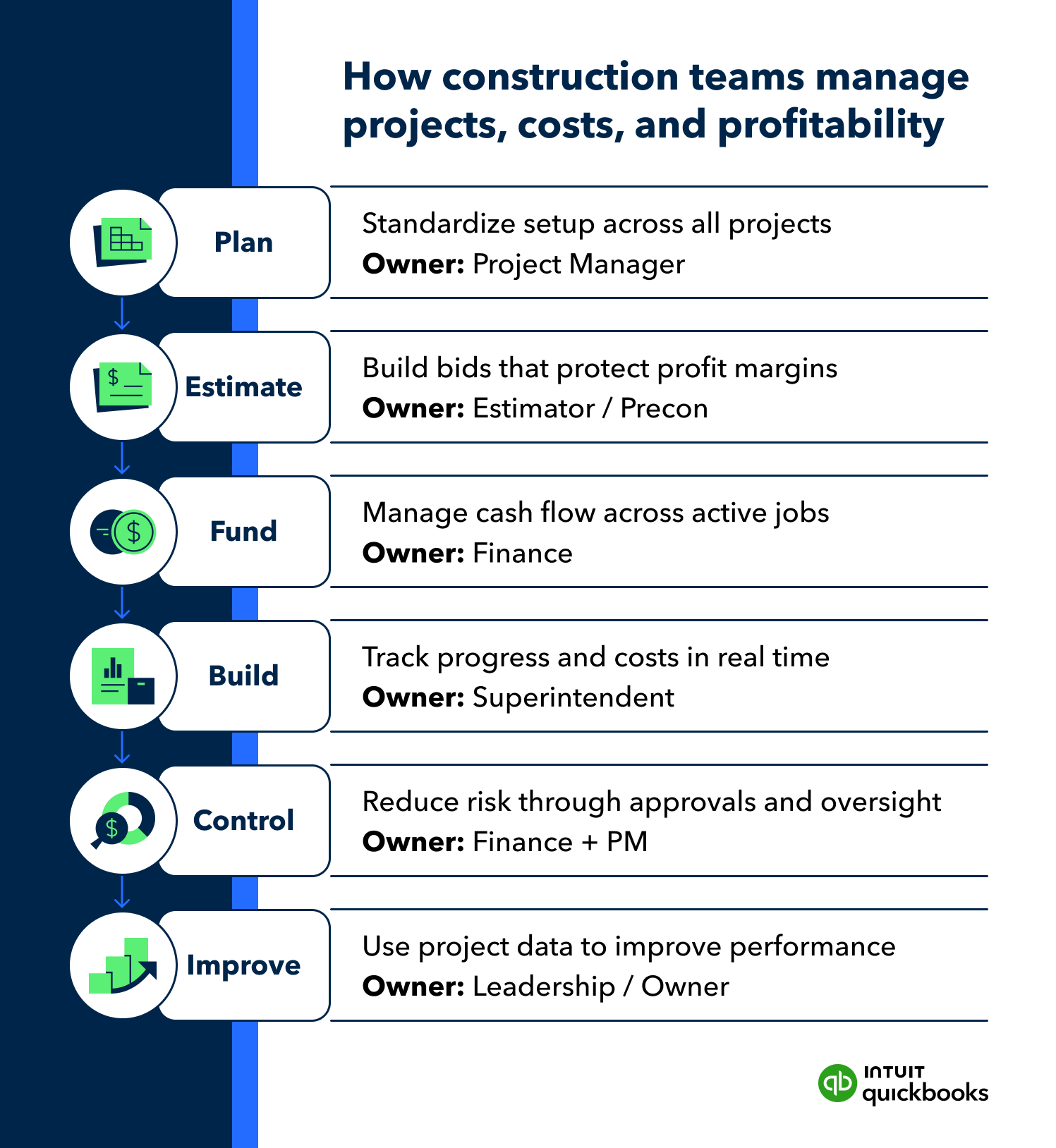

Before getting into specific workflows, it helps to step back and look at how strong construction teams structure the entire process. Managing multiple jobs successfully comes down to aligning planning, financial oversight, and execution from the start—so each project follows a consistent path, and performance stays visible at every stage.

The framework below outlines how construction firms manage multiple active projects without losing control as they grow:

Managing a handful of jobs is one thing. Managing ten, fifteen, or more at the same time introduces a different level of financial complexity. Costs move in parallel, timelines overlap, and small gaps in visibility can quickly turn into margin pressure or cash constraints.

For construction business owners and finance leaders, the challenge is staying ahead of performance across every project—not just reacting after the fact.

Here are some of the most common issues that come up at this stage:

Overlapping projects often mean paying for labor and materials before payments are collected. Delays in billing or retainage can stretch that gap and put pressure on working capital. Cash tied up in one project can limit your ability to fund others, especially when timelines don’t line up.

Costs spread throughout systems or tracked inconsistently make it difficult to see which jobs are actually performing well. Without timely job-level insight, overruns can go unnoticed until margins are already impacted.

Different project managers often follow different workflows for tracking expenses, submitting invoices, or reporting progress. That inconsistency leads to uneven data and slows down reporting.

Relying on delayed updates limits the ability to adjust mid-project. When data lags, decisions around staffing, purchasing, or timelines are often made too late to protect profitability.

Standardizing how each job is structured—job costs, billing schedules, and roles—creates consistent data. That consistency allows teams to review jobs side by side, monitor cash flow, and see where issues are starting to build.

As more jobs run simultaneously, an inconsistent setup can start to show up in the numbers. One project tracks subcontractors one way, another handles billing differently, and reporting stops lining up. A consistent structure across every project keeps financial data aligned and easier to act on.

Start by putting a uniform framework in place for how each job is set up and managed:

Construction projects generate costs from multiple sources—crew labor, subcontractors, materials, equipment, and staged billing. Keeping all of that in one place ensures nothing slips through the cracks, even as more jobs run simultaneously.

Different job types may vary, but your cost structure shouldn’t. Consistent categories make it possible to compare jobs and spot trends.

Construction projects move fast, and unclear ownership can slow things down, especially when multiple teams are working at once. Financial accountability should be set before work begins to keep decisions moving and prevent gaps in oversight.

Spreadsheets, texts, and separate tools make it harder to trust the numbers. A centralized system keeps everything in sync.

Stronger bidding starts with better financial inputs. As project volume grows, relying on rough estimates or outdated assumptions increases the risk of underpricing and margin loss. A more structured approach to forecasting helps ensure every project starts on a solid financial footing.

Using historical project data leads to more accurate bids and fewer surprises during execution. It also captures cost patterns that emerge as project volume increases.

Benchmarking improves bidding consistency and reduces guesswork when estimating several jobs at once.

Defining margin expectations upfront helps guide pricing decisions and project selection.

Disciplined bidding protects capacity and keeps resources focused on profitable work.

Managing multiple jobs successfully depends on timing as much as totals. Cash can look strong on paper while still falling short in practice if payments and expenses don’t line up due to varying project timelines. Cash from one project often supports costs on another, and without a full view of all active jobs, it’s easy to miss emerging risk.

Gaps between inflows and outflows need to be tracked closely. You need to know when money is coming in, when it’s going out, and how those timelines differ from one job to the next.

Coordinating payment timing helps reduce strain on working capital. It also keeps cash moving between jobs more predictable as projects progress at different speeds.

Ongoing visibility into cash helps prevent one job from draining resources needed for another. It also highlights where cash is tied up in work that hasn’t been billed yet.

Early visibility into cash gaps gives you time to pivot before they impact operations.

Financial data and project status visibility allow you to identify overruns early and protect your margins for each active job. It also highlights how projects are performing relative to each other, including which ones are using a disproportionate share of time, cost, or resources. Without timely reporting, critical adjustments often happen too late—after costs have already exceeded the budget.

Regular cost comparisons help keep projects in scope with original estimates and prevent small gaps from growing.

Progress and spend need to be evaluated together to understand true job performance.

Early signals give you room to respond before profitability is affected.

A current view of your active jobs reveals where time, cost, and resources are starting to drift, so teams can rebalance effort where it’s needed most.

Strong financial controls can reduce common construction business errors. They can protect margins and help ensure appropriate tracking and approval of every dollar.

As project volume increases, informal processes create more exposure. More transactions, more vendors, and more team members involved in spending can introduce gaps without clear oversight. When several jobs are active, those gaps can affect more than one project at a time. Structured controls help maintain accuracy and accountability.

Dividing financial responsibilities reduces the risk of errors and unauthorized activity.

Defined approval processes help control costs and prevent unplanned budget increases.

Standardized billing practices improve cash flow and reduce delays or disputes, especially when projects bill at varying points in time.

Stronger controls help catch issues early and maintain trust in your financial data.

Project-level data helps you focus on the work that drives profit and shows how jobs are performing relative to each other. Gain insights into resource-straining jobs and make more informed decisions about which jobs to pursue.

As more projects move through your pipeline, patterns start to emerge. The key is using that data intentionally—so past performance shapes future bids, staffing, and project selection.

Profitability often varies by project type, client, or scope, even if revenue looks similar.

Not all projects are worth pursuing, especially if they consistently lead to cost overruns or delays.

Historical trends help refine future estimates and reduce bidding uncertainty.

Data helps determine how much work your team can take on without impacting performance.

Managing multiple construction jobs simultaneously requires more structure than spreadsheets, manual tracking, or disconnected systems can support. Gaps in visibility, inconsistent processes, and delayed reporting can put pressure on margins and cash flow.

The steps below focus on practical changes you can put in place quickly, then build on over time to strengthen oversight, improve consistency, and support better financial decisions.

Managing more projects requires a system that brings financial data, workflows, and decision-making into one place. QuickBooks Online Advanced plus the construction module gives you visibility into job costs, phase-based budgets, and connected billing—so you can run tighter jobs and protect margins from day one.

QuickBooks Online Advanced with the construction module gives you the structure to manage growth with confidence and maintain control from bid to closeout.

Call Sales: 1-800-285-4854