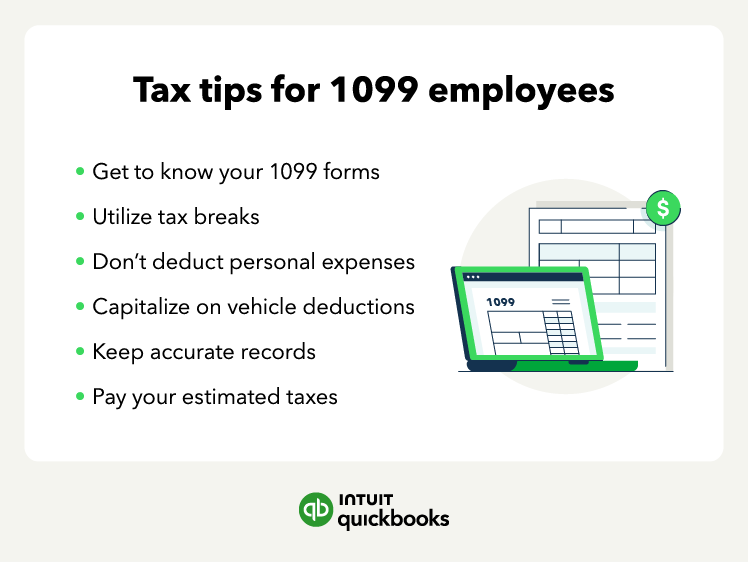

3 things to know if you receive a 1099

Getting a 1099 form means you’re considered self-employed for tax purposes, even if you only do contract work part-time.

In other words, you’re responsible for managing your own taxes, tracking your income, and taking advantage of deductions that employees can’t. Here are three essentials every 1099 worker should know before filing.

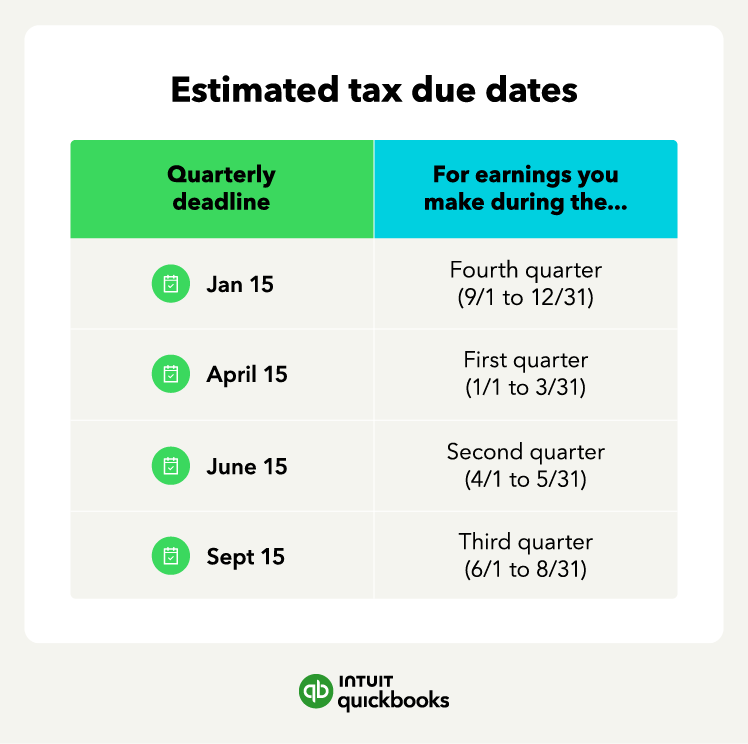

1. It's helpful to set aside 20–30% of your income for taxes

Setting money aside as you earn it helps avoid penalties and cash flow stress when tax deadlines arrive. The exact amount depends on your tax bracket and deductible expenses, but saving a portion of every payment ensures you’re prepared for quarterly estimates.

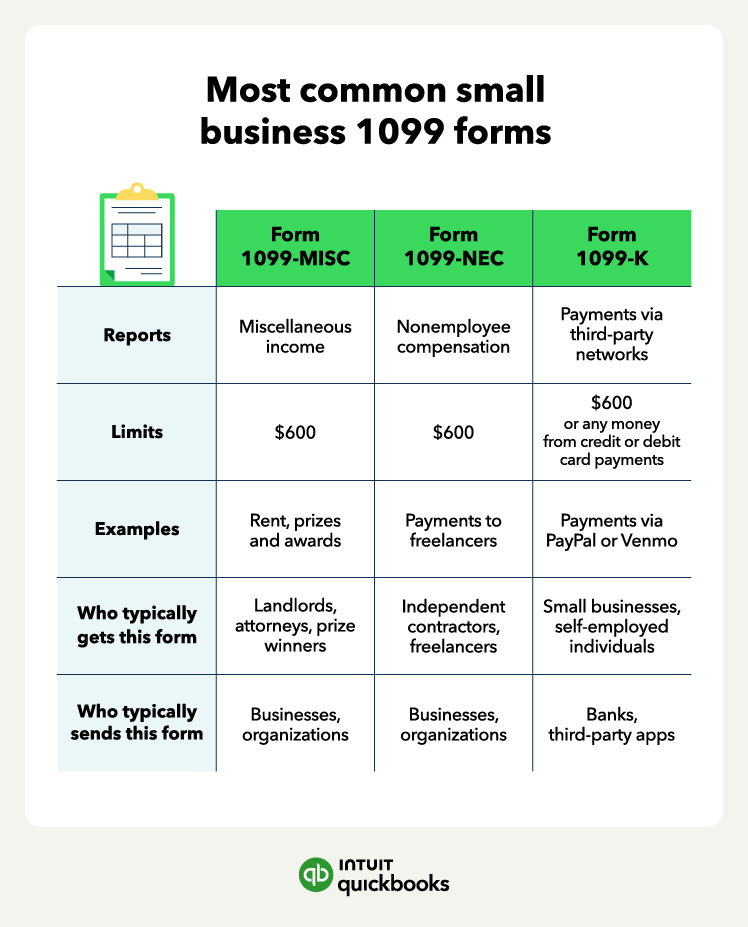

2. 1099 income taxes can be lowered with deductions

Vehicle expenses, home office costs, and equipment purchases can all reduce your taxable income when documented properly. Review IRS guidelines each year to make sure you’re claiming every deduction available for self-employed individuals.

3. You may still receive a tax refund

If you have withholdings or business expenses that reduce your taxable income, you could qualify for a refund—even as a self-employed worker. Accurate recordkeeping and on-time estimated payments can increase your chances of getting money back at filing time.