Still, why does the Chinese government care so much about building solid logistics infrastructure?

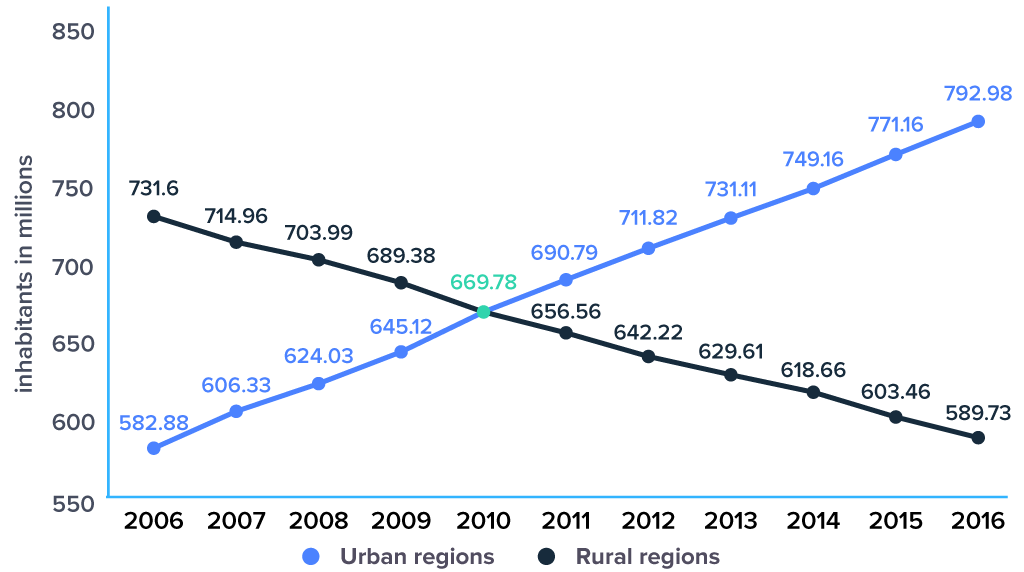

If you have a country whose growth has been fueled by export-driven manufacturing through consolidated populations (i.e., urbanization), per-capita GDP increases while competitiveness declines. In that setting, internal markets must also be accelerated such that your entire economy — and, therefore, quality of life and GDP — doesn’t decelerate.

Accelerating internal markets means accelerating consumerism: not just more and better ways to purchase consumer goods online but more, better, and above all faster ways to receive those goods offline.

According to Reda Hamedoun, World Bank’s Senior Transport Specialist:

“China’s logistics sector has grown over 20 percent a year and is now the largest logistics market in the world. However, China lacks a well-developed logistics network. Connectivity, technology penetration and modern warehousing have been lagging.”

Those “lagging” elements are quickly being brought up to speed.

Already a policy document released by the China’s State Council in October 2015 revealed that the Chinese government has made a deliberate strategy to invest in the Chinese express delivery system. China aims to nearly quadruple the revenues of its express delivery market by 2020, in a move to boost consumption and services

Stanford Business’ white paper, “U.S.-to-China B2C E-Commerce: Improving Logistics to Grow Trade,” explains:

“Unlike the United States, where a few key players (e.g., FedEx, UPS) dominate the express shipping market, China’s domestic express delivery market is very crowded, with seven major players in the mainland (state-owned China Postal Express and six private companies).”

In addition, estimates place the total number of domestic shipping competitors in the thousands. Private firms — most notably, Shentong Express and S.F. Express — have cut into traditional leaders. While China Post EMS is still the largest firm in the Chinese delivery, the company’s market share fell 10% in 2015 from nearly 60% in 2007.

Why? Because, as Stanford Business points out, “China Post Express Mail Service (EMS), the state-run postal organization, is often viewed as a less attractive alternative to privately owned companies, due to its slower speed of delivery and lower quality of service.”

Densely populated cities like New York, London, and Los Angeles, are catching up with same-day delivery. Meanwhile, China has mastered same-hour delivery.

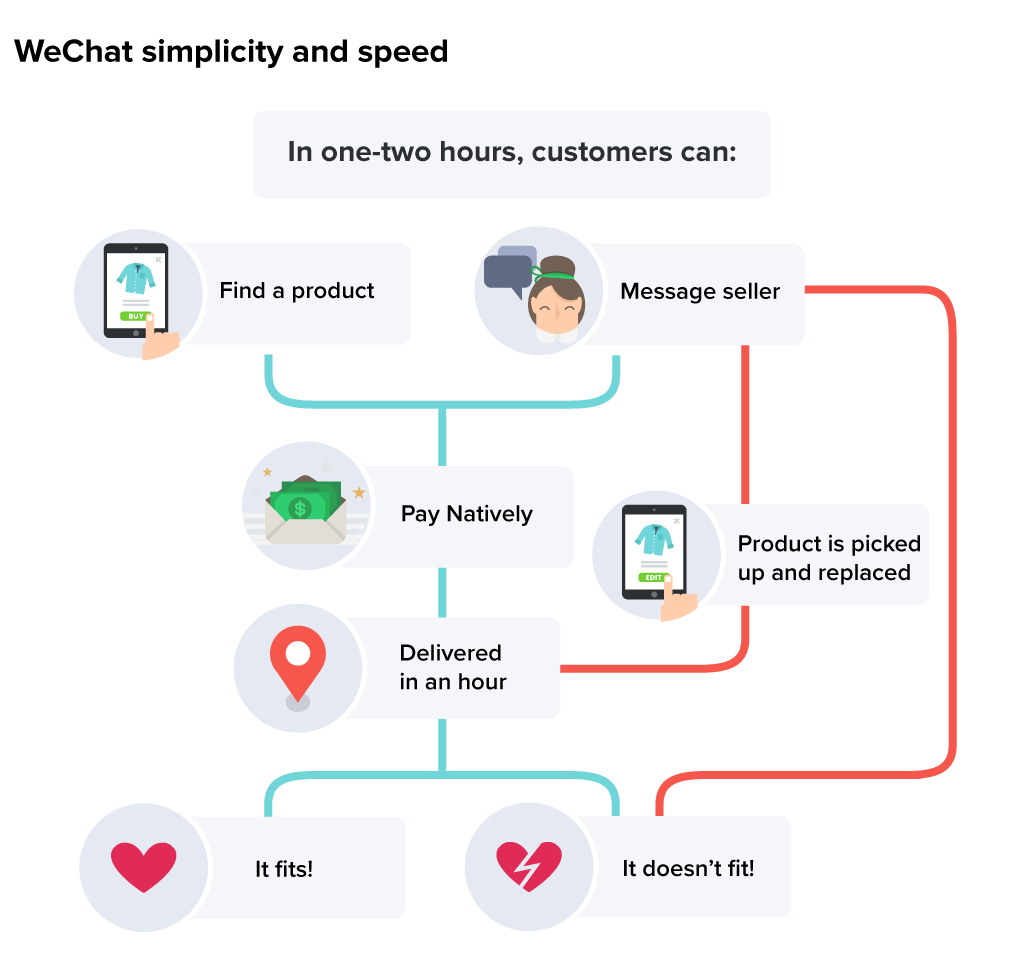

Moreover, you can’t discount the fact — explored above — that from the consumer’s perspective, all this done on WeChat, WePay, or some equivalent. Customers find a shop, converse with the owner or a bot representative, and place their order without doing anything more than click a button.

For fungible products, purchases turn up within an hour. If something doesn’t fit, you return the product using the same socially integrated platform and ten minutes later someones picks it up with an exchange.