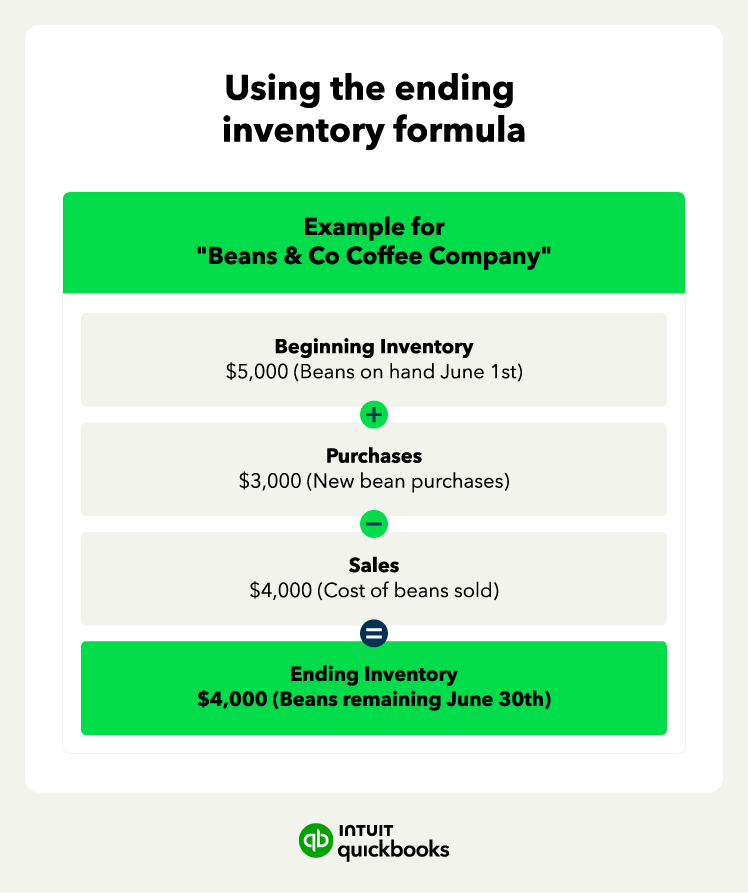

1. First-in, first-out (FIFO) method

The FIFO method assumes that the oldest items in inventory are sold first.

Let’s assume that a retailer called Seaside Candles sells home furnishings, including several product lines of candles. The current inventory of Seaside Candles includes these purchases:

- 500 candles purchased on Dec 1st for $10 each

- 250 candles purchased on Dec 15th for $12 each

- 750 candles purchased on Dec 20th for $13.50 each

If Seaside sells a total of 400 candles on December 25th, the FIFO method values the candles sold at $10 each. Most companies use the FIFO method to value items sold out of inventory. Some firms, however, use the last-in, first-out (LIFO) method.

2. Last-in, first-out (LIFO) method

To understand the LIFO method, think about buying milk at the grocery store.

The oldest gallons of milk are pushed to the front of the refrigerator so that you’re more likely to buy the older product before it expires. To get to the newer milk, you have to reach behind the old products. Getting to the newer milk is the LIFO method.

LIFO assumes that the newest units are sold first. If Seaside uses the LIFO method, the 400 candles sold on December 25th are valued at $13.50 each.

3. Weighted average cost method

To compute the weighted average cost, you add the total dollar amount of purchases and divide the balance by the total number of units purchased.

Here is the total dollar amount of the three purchases of Seaside Candles:

- 500 candles at $10 each = $5,000

- 250 candles at $12 each = $3,000

- 750 candles at $13.50 each = $10,125

The retailer spent $18,125 to purchase 1,500 candles, and the average cost per candle is $12.08. If the business uses the weighted average cost, $12.08 is assigned as the cost of each candle sold.

4. Gross profit method

The gross profit method estimates ending inventory when a physical count isn’t possible, like during a mid-month report or after a loss, such as fire or theft. It’s quick and helpful for temporary reporting but shouldn’t be used for final financial statements.

To use this method, you first estimate your COGS using your gross profit margin, then apply the ending inventory formula.

Estimated COGS = Net Sales × (1 – Gross Profit Margin)

Let’s say Seaside Candles had $5,000 as beginning inventory, $20,000 for net sales for the month, $10,000 of purchases, and a 40% gross profit margin. In this case:

- Estimated COGS = $20,000 × (1 – 0.40) = $12,000

- Ending Inventory = $5,000 + $10,000 – $12,000 = $3,000

This method is useful for quick decision-making, but since it's based on estimates, it's not suitable for audits or tax filings.

5. Retail method

The retail method is used by many retailers to estimate inventory without doing a physical count. It works best for stores that sell many low-cost items with consistent markups.

This method compares the total value of inventory at retail prices to its value at cost, using the cost-to-retail ratio.

- Cost-to-Retail Ratio = Cost of Goods Available for Sale / Retail Value of Goods Available

- Ending Inventory at Retail = Retail Value of Goods Available for Sale – Sales

- Ending Inventory at Cost = Ending Inventory at Retail × Cost-to-Retail Ratio

Let’s say Seaside Candles had $60,000 inventory at cost, $100,000 Inventory at retail, and $40,000 of sales. Putting these in the formulae:

- Cost-to-Retail Ratio = $60,000 / $100,000 = 0.6

- Ending Inventory at Retail = $100,000 – $40,000 = $60,000

- Ending Inventory at Cost = $60,000 × 0.6 = $36,000

This method saves time and is simple to apply if you have consistent pricing, but it becomes less reliable with varied discounts or changing markups.

Use a solution like Intuit Assist that helps you keep track of your financial metrics and apply your chosen method automatically, so you don’t have to track it by hand.