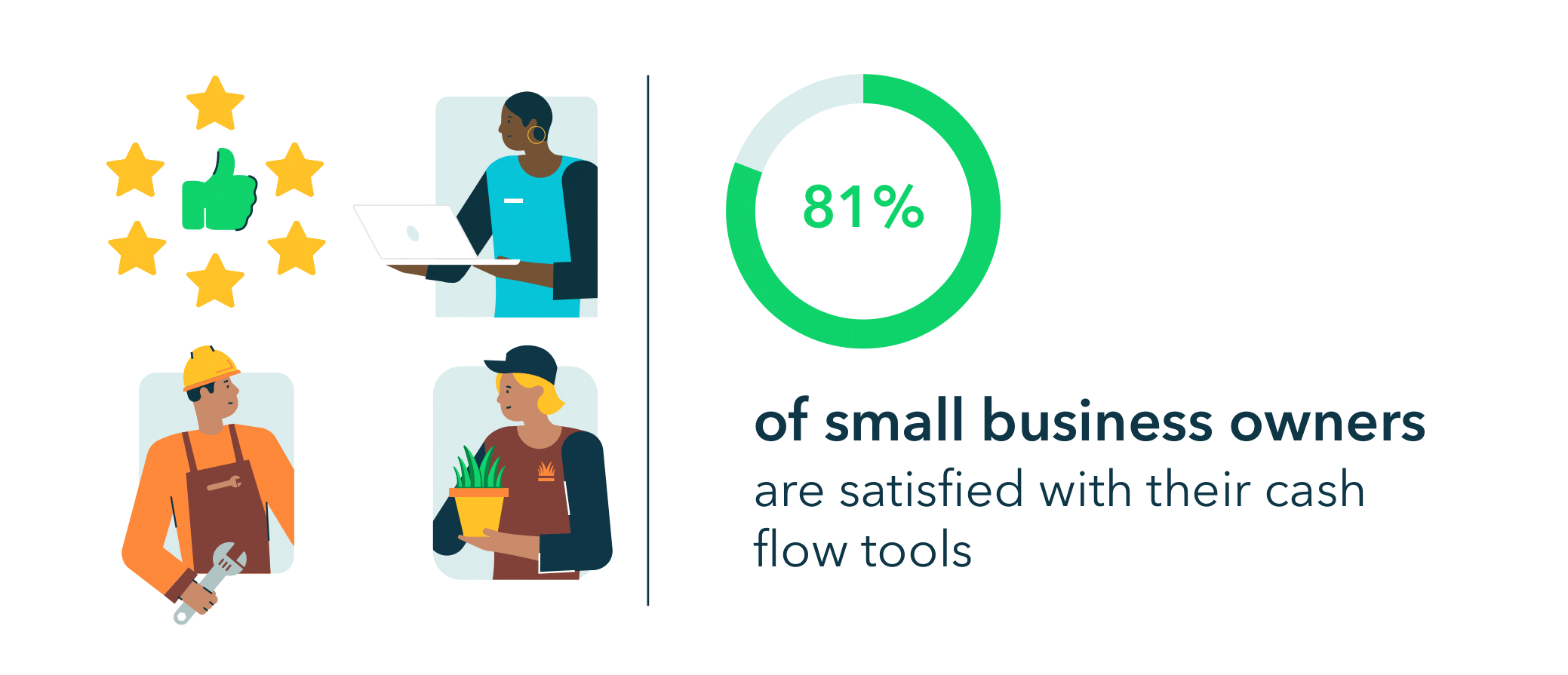

Planning for the future

Even before the coronavirus pandemic, small business owners were anticipating a recession. In 2019, nearly three in four small business owners (71%) believed there would be an economic recession in the coming two years.

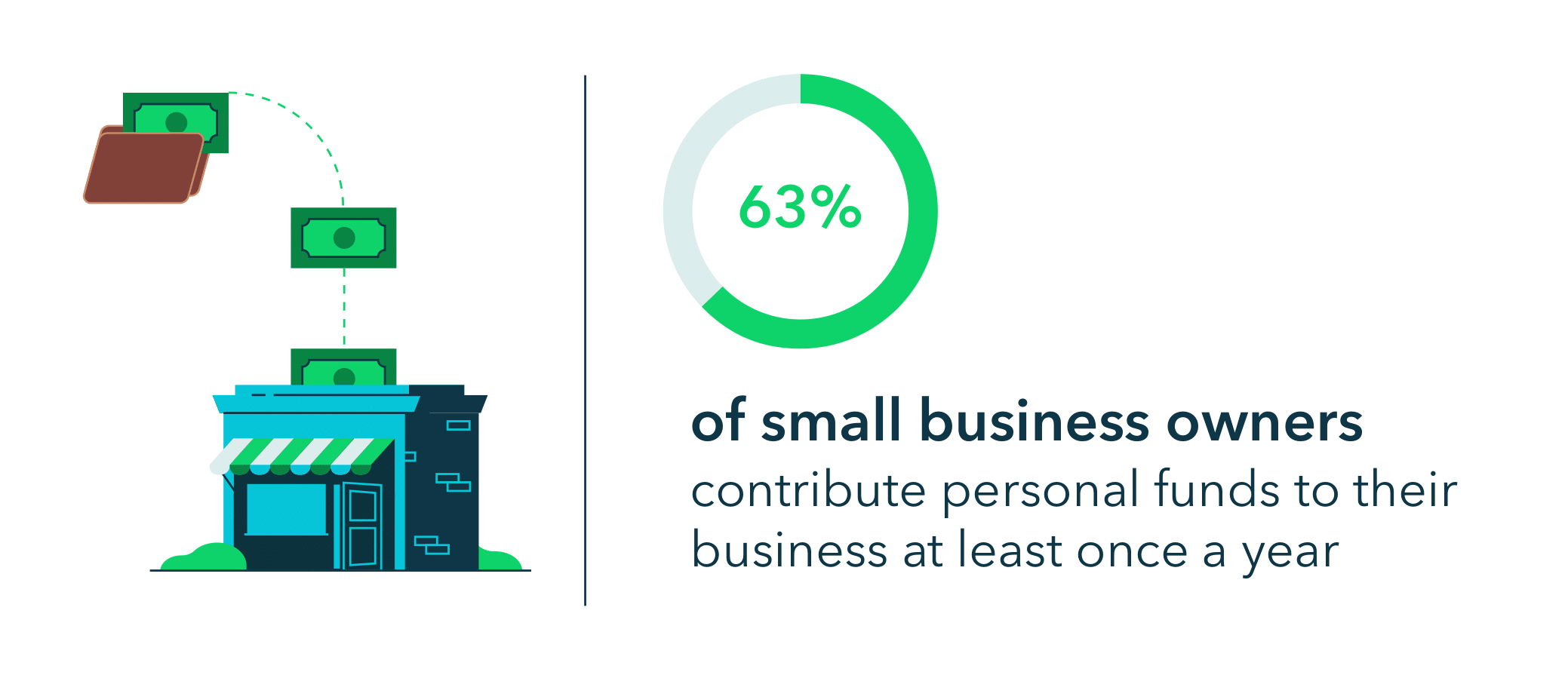

A study released in April 2021 by the U.S. federal reserve found that the pandemic has resulted in the permanent closure of around 200,000 U.S. more businesses than average historical levels during its first year. Without the funds to sustain themselves through fluctuations in sales volume, or the insight to plan for those fluctuations, businesses are at risk.

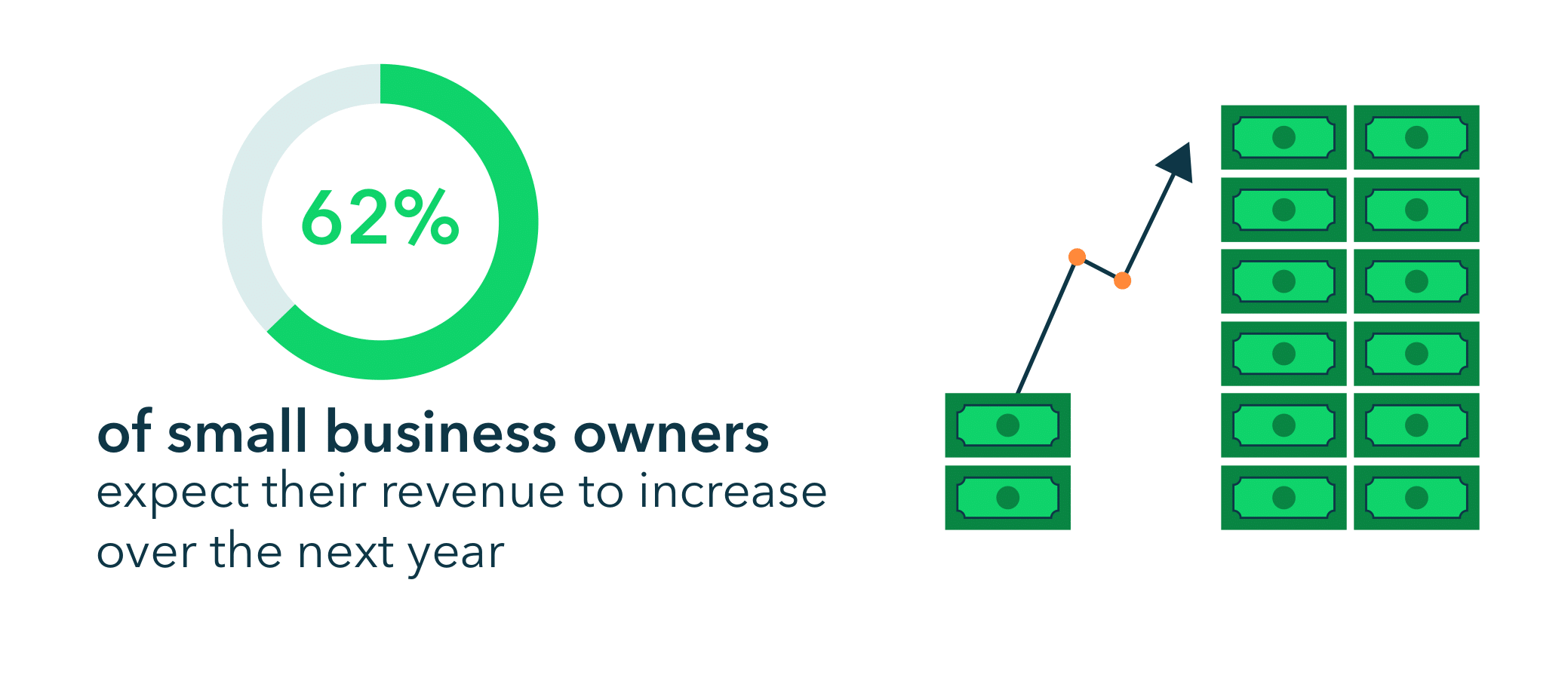

Despite the challenges they have weathered, the majority of small business owners are optimistic about their financial futures. Additional research conducted by QuickBooks shows that even some of the businesses most impacted by the COVID-19 pandemic are back to their pre-pandemic levels.

Businesses are rapidly evolving to meet market demands by testing new business models, developing new products, and offering customers new channels and methods to make purchases. In the U.S., 86% of small businesses have developed new products and services as a result of the coronavirus, according to our research in 2020.