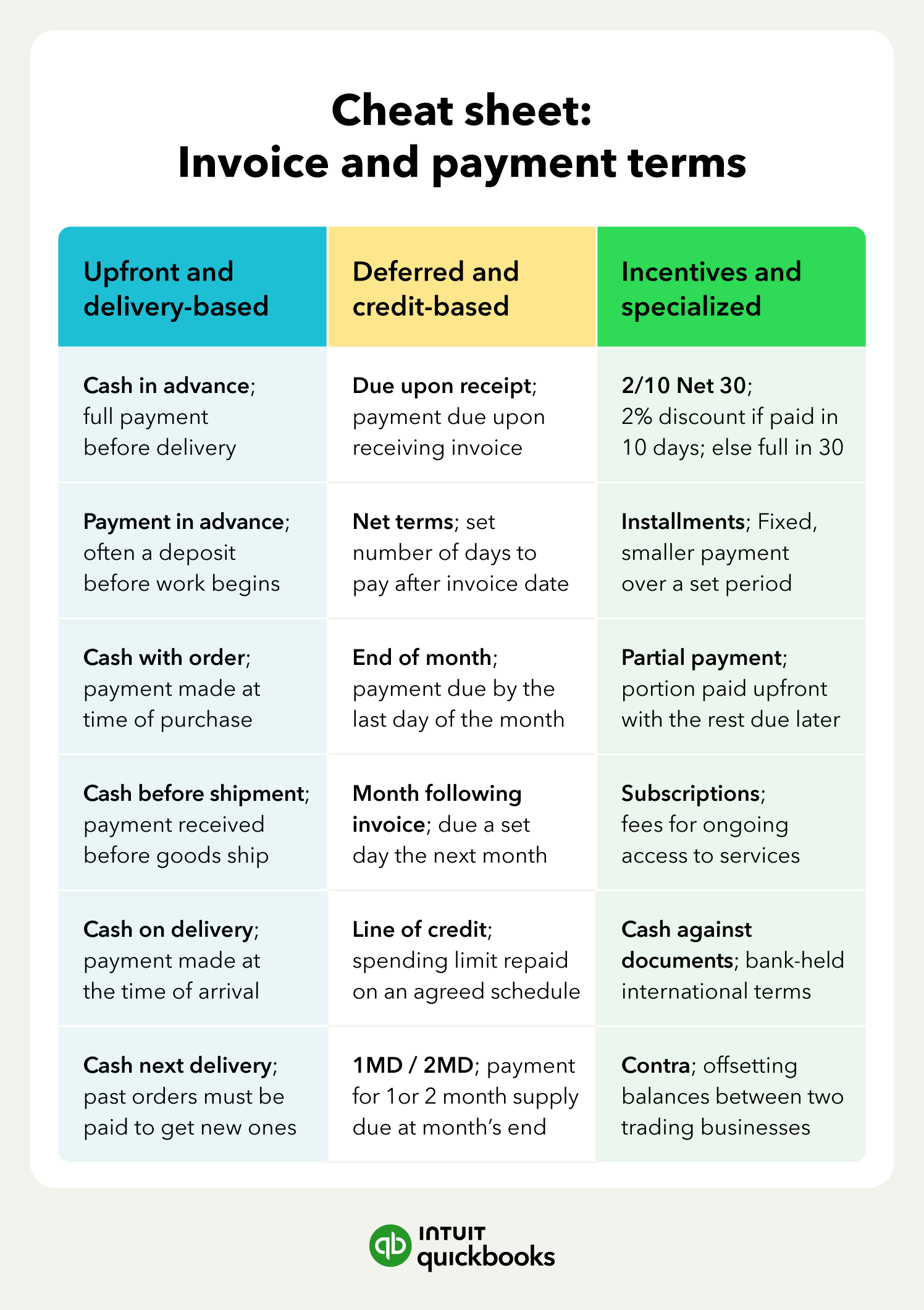

Master your payment strategy for long-term success

Choosing the right payment terms is a strategic move that protects your time, stabilizes your cash flow, and sets a professional tone for every client relationship. When your expectations are clear from the start, you spend less time chasing down payments and more time on the work that grows your business.

Managing these details is much easier with the right tools in place. Invoicing software like QuickBooks Online automates the heavy lifting by applying your specific terms to every bill and sending automatic reminders to forgetful clients.

This automation helps you keep your books balanced and your revenue predictable enough to lead your business with confidence.

Disclaimers

QuickBooks Live Expert Assisted requires QuickBooks Online subscription. Additional terms, conditions, limitations, and fees apply.

Product Information:

QuickBooks Card Reader: Data access subject to cellular/internet provider network availability and occasional downtime due to system and server maintenance. Product registration and QuickBooks Payments account required. Terms, conditions, and features subject to change.

QuickBooks Payments: QuickBooks Payments account subject to eligibility criteria, credit, and application approval. Subscription to QuickBooks Online required. Money movement services are provided by Intuit Payments Inc., licensed as a Money Transmitter by the New York State Department of Financial Services.

QuickBooks Money is a standalone Intuit offering that includes QuickBooks Payments and QuickBooks Checking. Intuit accounts are subject to eligibility criteria, credit, and application approval. Baking services provided by the QuickBooks VisaⓇ Debit Card is issued by Green Dot Bank, Member FDIC, pursuant to license from Visa U.S.A., Inc. Visa is a registered trademark of Visa International Service Association. QuickBooks Checking Deposit Account Agreement Apples. Banking services and debit card opening are subject to identity verification and approval by Green Dot Bank. Money movement services are provided by Intuit Payments Inc., licensed as a Money Transmitter by the New York State Department of Financial Services.

For more information about Intuit Payments' money transmission licenses, please visit https://www.intuit.com/legal/licenses/payment-licenses/.

Based on U.S. Intuit Assist Beta customers using outstanding invoice notifications and AI-drafted invoice reminder features, compared to customers sending standard invoice reminders to the same customers, from January 2024 to August 2024. Not available in QuickBooks Online Advanced.