Free money for your Florida business is real. It is also rarer than the internet makes it sound. This guide maps the major Florida small business grants and loans open in 2026, with current award amounts and application windows, so you spend your time on programs you can actually win.

There's a reason to get funding right, whatever form it takes. According to the Intuit QuickBooks Small Business Financing Report, small businesses that use business financing rather than personal funds are nearly twice as likely to be in an active growth phase. Yet most solo owners still fund the business out of their own pocket: 29% lean on personal credit cards and 28% on personal savings. Grants and well-chosen loans are how you break that pattern. As Jannese Torres, host of Intuit QuickBooks' Mind the Business podcast, put it on "How to Raise Capital and Find Funding For Your Small Business": "I think grants are probably the most accessible for folks, especially people who don't necessarily have a network of people that they can leverage as investors... when it comes to funding your business without having to take on debt, grants are really really key."

When we say funding here, we mean both grants, the money you never repay, and loans, the money you borrow on defined terms. Most Florida businesses end up using some of each, so this guide covers the full stack.

If you run a shop or service business in Miami or Orlando and keep hearing about free government money, this shows you which programs are real and which windows are open right now. If you're a woman or minority founder, several programs below were built specifically for you. If you farm or operate in a rural county, your best options look different from everyone else's. And if you're building technology near UCF or USF, there's a $150,000 matching program with your name on it.

By the end, you'll know which 2026 programs fit your business, when to apply, what winning means for your taxes, and exactly what to do if the grant doesn't come through. Let's start with the decision that shapes everything else: money you keep versus money you borrow.

Jump to:

- Grants vs. loans: Understanding your funding options

- What to consider before applying

- Florida grant deadlines: the 2026 grant window tracker

- 9 Florida small business grants for 2026

- Eligibility requirements for grants in Florida

- 4 Federal small business grants

- Additional grant resources for Florida business

- How to get a business grant in Florida: Application process

- Are business grants taxable in Florida?

- How to spot grant scams and pay-to-apply middlemen

- Florida small business loans

- How to get a business loan in Florida: Application process

- What to do if you don't win a grant

- Florida small business funding resources and support

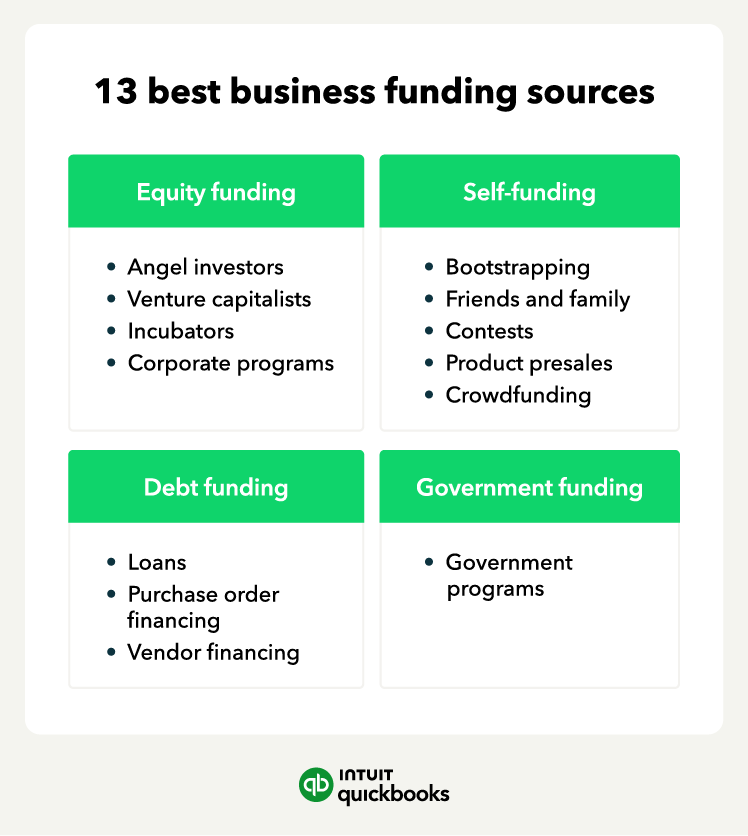

- Other ways to fund your small business in Florida

- How QuickBooks helps Florida businesses put funding to work