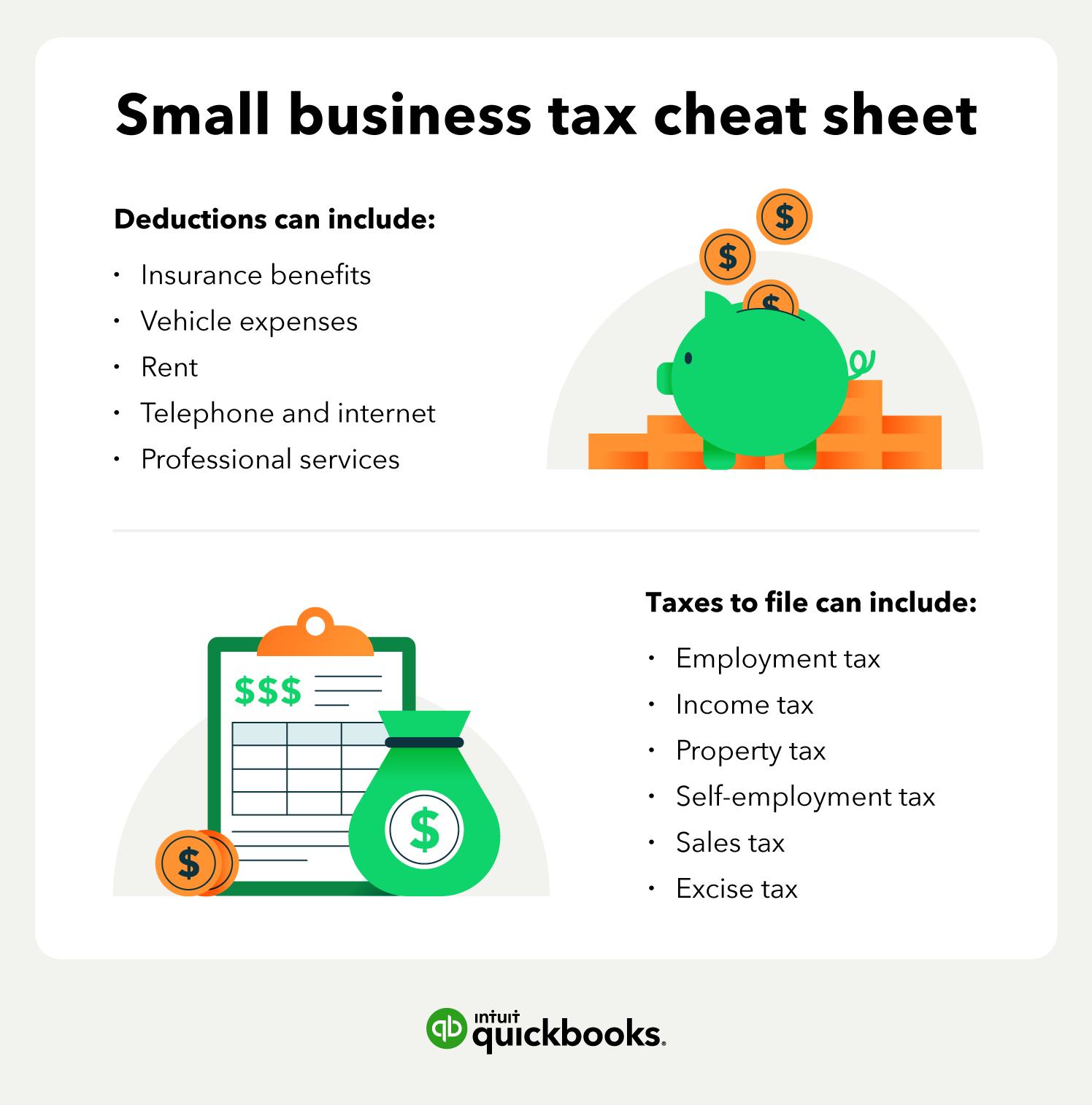

Types of business taxes in Florida

As an employer in Florida, you may be responsible for reporting and paying other business taxes in addition to withholding payroll taxes from your employees' paychecks. From federal to state and local levels, understanding the different tax programs and their impact on your business’s finances is important.

This includes staying on top of pay transparency requirements in Florida to keep your business complaint and establish fair workplace practices. Also, when making new hires, there's a lot of key info and legal areas to stay on top of, so be sure to check out the Florida new employee paperwork.

Federal taxes

You'll be responsible for federal taxes in whatever state you open a business in. Unfortunately, there are dozens of federal tax forms with unique due dates and requirements. Using an accountant or small business accounting software can be helpful in avoiding mistakes that can lead to overpayment or penalties.

As a business owner, you have both personal and business tax filing obligations. Here’s what you need to know:

Personal tax filing

Federal income tax returns:

Every individual is required to file and pay federal personal income tax. This forms the foundation of your overall tax responsibility.

Business tax filing

Business owners have additional filing requirements, depending on the business structure:

- Sole proprietorship: Income and expenses are reported on your personal tax return using Schedule C (Form 1040).

- Partnership: A partnership must file an information return (Form 1065) to report income, deductions, and other relevant details, while each partner reports their share of income on their personal return.

- Corporation: A corporation files a corporate tax return (Form 1120), paying taxes on its profits.

- S Corporation: An S corporation files an informational return (Form 1120S). Its income, losses, and deductions pass through to shareholders, who report them on their personal returns.

- Limited Liability Companies (LLCs): LLCs are not classified separately for federal tax purposes and are taxed based on their ownership structure. Single-member LLCs default to sole proprietorship taxation or may elect corporate taxation, while multi-member LLCs default to partnership taxation or may elect corporate taxation.

Self-employment tax

If you work for yourself and earn more than $400 a year, you pay toward Social Security and Medicare programs through a self-employment tax. The Social Security system provides retirement benefits, disability benefits, survivor benefits, and hospital insurance (Medicare) benefits.

Employment taxes

As an employer, you are responsible for withholding and depositing federal income tax and the employee contribution to Social Security and Medicare taxes. You must also pay the employer portion of Medicare and Social Security and pay federal unemployment tax (FUTA).

State taxes

There is no state income tax, but it does collect several types of taxes to fund its government, such as excise taxes, franchise taxes, property taxes, and others.

Florida corporate income tax

In Florida, corporations are subject to a 5.5% corporate income tax. However, each corporation can deduct a $50,000 exemption from its taxable income, meaning only income above $50,000 is taxed. It is actually a single corporate income/franchise tax imposed on corporations for the privilege of conducting business, deriving income, or existing within Florida.

This tax applies to corporations, including entities that are taxed federally as corporations. All corporations subject to Florida corporate income tax are required to file a return, regardless of their taxable income level.

What is the corporate tax rate?

The standard corporate income tax rate for C corporations in Florida is 5.5% on any profits over $50,000, but qualifying exemptions can reduce this rate significantly.

How is the corporate income tax calculated?

Florida’s corporate income tax is 5.5% on taxable income over $50,000. Taxable income is determined by adjusting federal taxable income using a three-factor apportionment formula (25% payroll, 25% property, 50% sales). After applying the $50,000 exemption, the remaining taxable income is taxed at 5.5%, with potential credits reducing the final tax liability.

Who may be liable for the corporate income tax in Florida?

The following entities must file a corporate income tax return; however, only those with taxable income exceeding $50,000 will actually owe tax.

- Corporations (including tax-exempt organizations) doing business, earning income, or existing in Florida.

- Banks and savings associations operating in Florida.

- Foreign corporations that are part of a Florida partnership or joint venture.

- LLCs taxed as corporations for federal tax purposes.

- LLCs taxed as partnerships if any owner is a corporation (corporate owner must file).

- Single-member LLCs owned by corporations (income reported on the corporate return).

- Homeowner and condominium associations filing Federal Form 1120.

- Political organizations filing Federal Form 1120-POL.

- S corporations paying federal tax on Form 1120S, Line 23c.

- Tax-exempt organizations with unrelated business income for federal tax purposes.

Businesses that have nexus in Florida—meaning a sufficient connection to the state through physical presence, employees, property, or business activities—are subject to this requirement.

See the Florida Department of Revenue for additional information.