You could save up to 25% on transaction costs².

Speak with us now to see if you qualify.

Talk to sales 1-800-515-8366

Monday - Friday, 6 AM to 4 PM PT

Table of contents

Table of contents

Most businesses reach a point where self-funding can only take you so far. Whether you’re expanding, investing in inventory, hiring employees, or smoothing out cash flow, the right financing can help you move faster with less stress. In the 2025 Intuit QuickBooks Small Business Financing Report, small businesses using business financing were almost twice as likely to be in a growth phase (54%) compared with those relying on personal funds (28%).

In most cases, you’ll be choosing between equity financing and debt financing. Both bring in capital, but they work differently, and the long-term impact on your business can be just as important as the amount you raise.

Let’s break down how each option works, what you’re trading off, and how to decide what makes sense for your next step.

Equity financing and debt financing both help you raise capital, but they work in different ways.

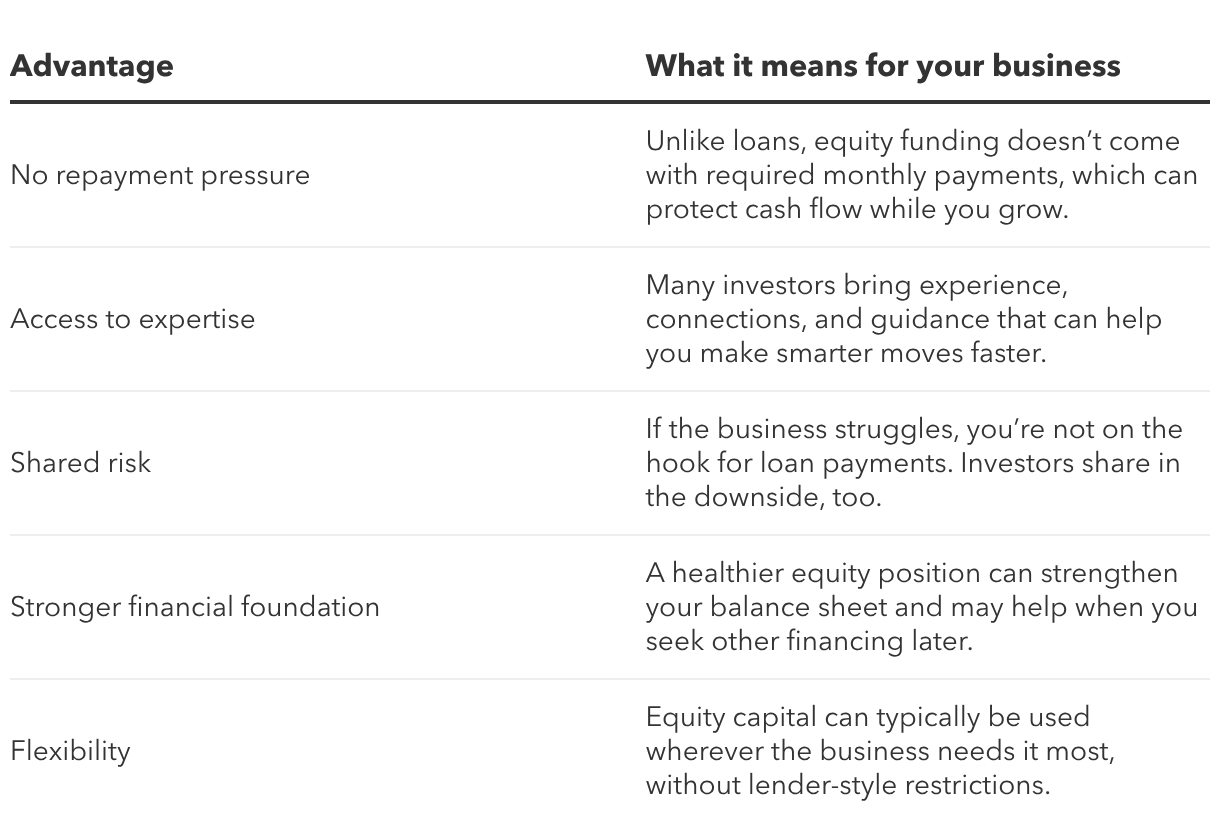

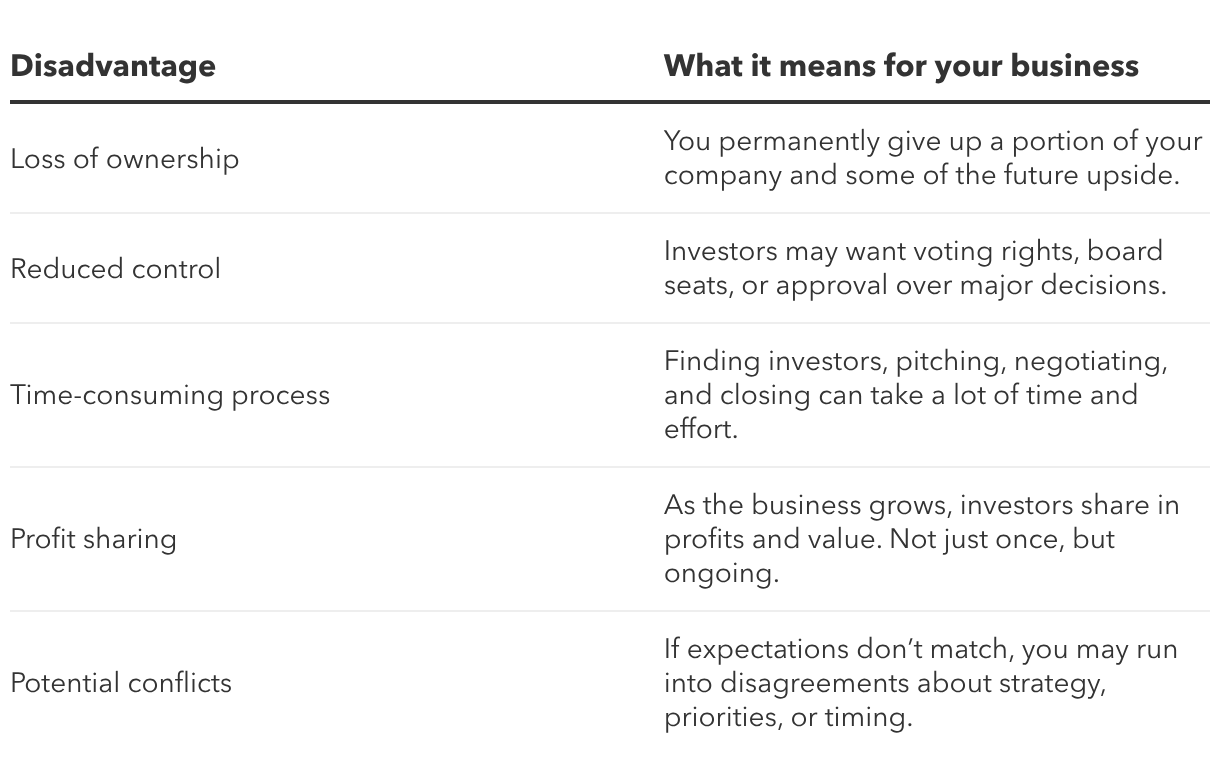

Equity financing means you raise capital by selling a piece of your company to investors. You don’t have set loan payments, which can take pressure off your monthly cash flow. The flip side is that you’re giving up part of your ownership, and some investors may want a say in big decisions as the business grows.

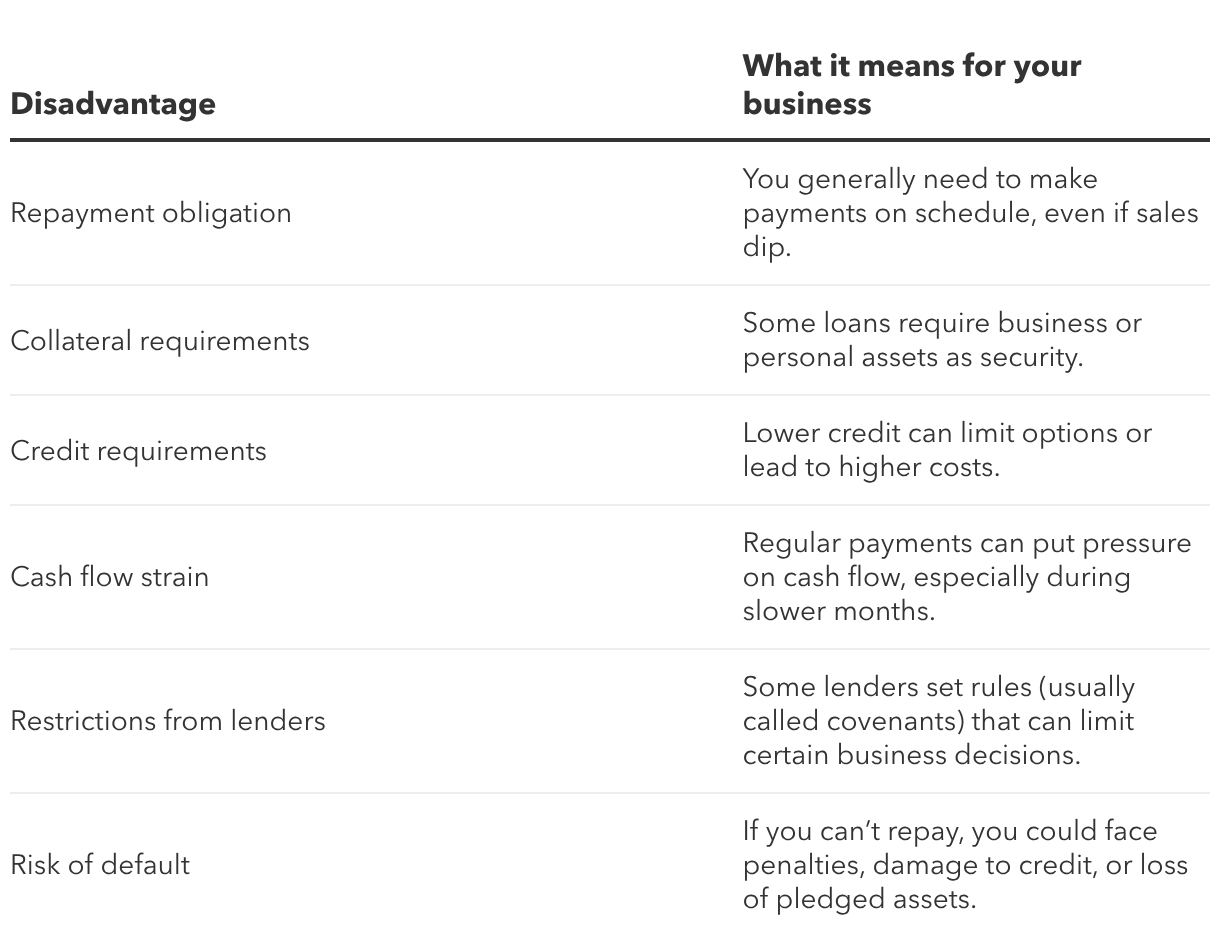

Debt financing means you borrow money and pay it back over time, usually with interest. You generally keep full ownership, which can be a big plus if control is important to you. But you’re also committing to regular payments, so it’s important to be confident your cash flow can handle them, even during slower months.

To help you visualize how these two methods compare, here’s a breakdown of their primary characteristics:

Equity financing is often considered the go-to for companies with high growth potential but limited tangible assets or cash flow to service a loan. It comes in several forms, each suited to different stages of a business's lifecycle.

Here are some of the common types of equity financing:

Choosing equity financing can offer several potential benefits:

However, equity financing also presents notable challenges:

Debt financing includes various borrowing arrangements that allow businesses to access capital while maintaining ownership.

There are a few common types of debt financing, and each one works a little differently:

Debt financing offers distinct benefits for the right businesses:

Debt financing can also come with some disadvantages:

Choosing between equity and debt financing depends on what your business looks like today, and where you’re trying to go next. There isn’t one best option for every owner. The right choice is the one that fits your goals, your cash flow, and the level of control you want to keep.

If you’re early in your journey, getting approved for a traditional loan can be tough. Newer businesses typically don’t have years of revenue history, strong business credit, or collateral to back a loan. In those cases, equity financing may be more realistic because investors are betting on your idea and your potential, not just your past numbers.

If you’re more established and bringing in steady revenue, debt financing may be a better fit. When you have consistent cash flow and a solid track record, borrowing can help you grow while keeping full ownership of your business.

Equity financing often makes sense for businesses pursuing rapid growth. If you’re trying to scale quickly and you’re willing to prioritize growth over short-term profitability, investors may be a good match because they understand the risk and are looking for long-term returns.

Debt financing is typically a better match for steady, planned growth. If you’re expanding in a way that’s easy to connect to revenue, like opening a second location, or adding inventory, a loan can help you move forward without giving up equity.

With equity financing, investors share the risk. If the business doesn’t work out, you generally don’t owe them repayment the way you would with a loan.

With debt financing, the risk sits more heavily on you. You’re expected to make payments on schedule, even if sales slow down. That’s why debt tends to work best when you’re confident your business can generate enough cash flow to cover the payments on a consistent basis.

Bigger, long-term projects can sometimes point toward equity. If you need a large amount of funding (and it may take time before the investment pays off), equity can provide capital without adding monthly repayment pressure right away.

For smaller, more defined needs, debt financing is often simpler. If you’re funding something specific, like inventory, a renovation, or a major purchase, borrowing can help you cover the cost without giving up a long-term share of your business.

Many businesses don’t choose just one path. They use a mix of equity and debt over time, leaning on each option when it makes the most sense.

One common approach is to start with equity financing in the early days. If you’re still building, testing, or proving your model, avoiding monthly loan payments can give you more breathing room. Then, as the business becomes more predictable and revenue is steadier, you may shift toward debt financing to fund the next stage of growth without giving up more ownership.

Other businesses use both at the same time to stay flexible. The key is balance: borrowing enough to support growth without putting too much pressure on cash flow, while also setting clear expectations with investors about how the business will operate and scale.

If you’re weighing equity financing vs. debt financing, it helps to step back and be honest about what you need and what you’re willing to trade for it. These questions can help you narrow it down:

The best choice is the one that fits your business today and supports where you’re trying to go next. If you’re unsure, you may want to talk with an accountant, financial advisor, or attorney so you understand the details before you commit.

Equity and debt financing can both help you grow. They just do it in different ways.

With equity financing, you raise money by sharing ownership. You’re not taking on loan payments, but you may give up some control and a portion of future upside. With debt financing, you borrow money and pay it back over time, usually with interest. You keep ownership, but you’re committing to regular payments that need to fit your cash flow.

The more clearly you understand the benefits and tradeoffs, the easier it can be to choose a path that supports your next step and your long-term vision.

Ready to explore funding options? A term loan or line of credit through QuickBooks may help you find financing that fits your business.

Disclaimer:

*QuickBooks Term Loan and QuickBooks Line of Credit loans are issued by WebBank.

Call Sales: 1-800-285-4854