You could save up to 25% on transaction costs².

Speak with us now to see if you qualify.

Talk to sales 1-800-515-8366

Monday - Friday, 6 AM to 4 PM PT

Table of contents

Table of contents

When your small business needs quick funding, a merchant cash advance (MCA) can seem like an easy yes. And it’s understandable since financing can help keep a business moving. In fact, the 2025 Intuit QuickBooks Small Business Financing Report found that businesses using financing are almost twice as likely to be in a growth phase than those relying on personal funds (54% vs. 28%).

When you’re facing a cash flow gap or an urgent expense, MCAs can offer fast access to capital with minimal paperwork, which is why they’re so tempting. However, speed and convenience often come at a cost. Before you sign, it’s important to understand the repayment structure, the total cost, and the potential impact on your day-to-day cash flow.

This guide explains how merchant cash advances work, when they may make sense, and what alternatives to consider first.

A merchant cash advance (MCA) is a lump sum of capital provided to a business in exchange for a percentage of future credit card sales or daily bank deposits. Despite its name, an MCA isn't technically a loan. It's a sale of your future receivables.

Here's the key distinction: Instead of borrowing money that you repay with interest over a set term, you're selling a portion of your future revenue at a discount. The MCA provider gives you cash upfront, and you repay them through automatic deductions from your daily sales until the advance, plus fees, is fully repaid. Because it’s a commercial transaction rather than a loan, it falls outside many of the regulations that govern traditional lending.

The MCA process is relatively straightforward and typically moves much faster than traditional financing options. Because the provider is purchasing future sales rather than lending money based on creditworthiness, the focus is heavily on your business's revenue streams.

Applying for a merchant cash advance usually involves a few specific stages designed to be quick and efficient. Here’s a step-by-step guide on how the application process typically works:

You submit basic business information and recent bank or credit card processing statements. The provider needs to verify your cash flow to determine how much they can advance you.

The provider reviews your average monthly revenue. They’re looking for consistency in your credit card sales or bank deposits to ensure you can support the daily repayment schedule.

You receive an offer based on your sales volume. This offer will detail the advance amount, the factor rate (the cost of the capital), and the repayment percentage. In some states, the provider must also disclose standardized cost information so you can compare the offer to a traditional loan or line of credit.

If approved, funds can hit your account within 24-48 hours. This speed is the primary selling point for businesses in urgent need of liquidity.

Most MCA providers require minimal documentation compared to traditional lenders. They're primarily interested in your sales history rather than your credit score or collateral, making this an accessible option for businesses with less-than-perfect credit. However, approval criteria and disclosures can vary depending on state law.

Repayment happens automatically, which reduces the administrative burden but impacts daily cash flow. Providers typically use one of two methods:

Understanding MCA terminology helps you evaluate offers accurately and compare them against other financing options.

Instead of an annual percentage rate (APR), MCAs use a factor rate, typically ranging from 1.1 to 1.5. This number multiplies your advance amount to determine your total repayment obligation.

Example: If you receive a $50,000 advance with a 1.3 factor rate:

The holdback is the portion of your daily sales or revenue that goes toward repayment. This is the slice of the pie the provider claims daily. Common holdback rates range from 10% to 20%.

Example: With a 15% holdback rate and $5,000 in daily credit card sales:

For ACH-based MCAs, the retrieval rate determines your fixed daily or weekly payment amount. Providers calculate this based on your average revenue and desired repayment timeline to ensure they recoup the advance within a specific window, often 3 to 18 months.

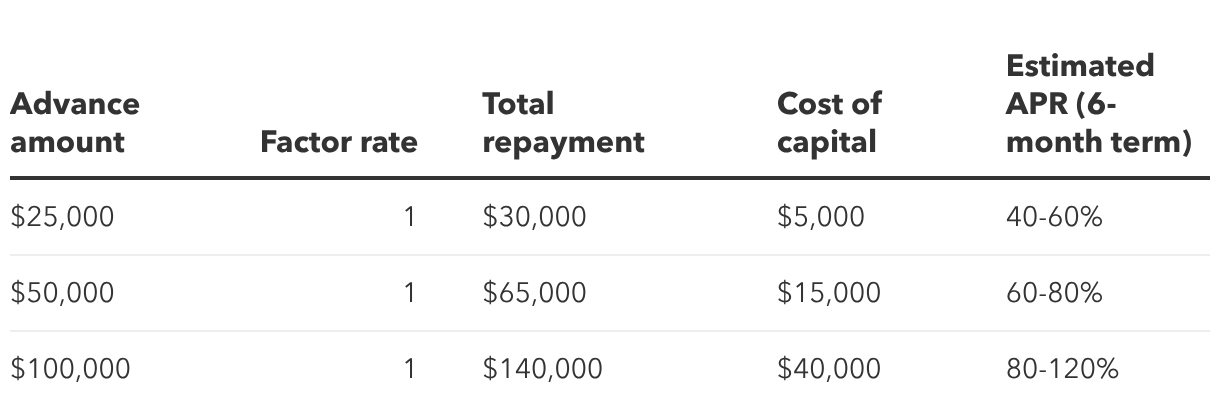

MCAs are among the more expensive forms of business financing. Understanding the true cost is key to determining if the potential return on investment (ROI) justifies the expense.

While factor rates seem simple, they can be deceiving. A 1.3 factor rate doesn't equal 30% interest because you're repaying the advance over months, not a full year. When you calculate the annual percentage rate (APR), which is the standard for comparing loan costs, MCA costs typically range from 40% to 350% annually, depending on your factor rate, repayment speed, and fees.

The following table illustrates how different factor rates impact total costs (illustrative example; actual costs vary):

Beyond the factor rate, some MCA providers charge extra fees that increase the total cost of funding. Be sure to ask about:

Despite their high costs, MCAs offer several benefits that make them appealing to certain businesses facing specific constraints.

For businesses that can’t wait weeks for a bank loan, the speed of an MCA is a big advantage.

When repayment is tied to credit card sales, your payments automatically adjust to your cash flow. During slow periods, you pay less, which can help preserve working capital when you need it most. This flexibility prevents the stress of a fixed monthly payment during a seasonal slump.

MCAs are unsecured, meaning you don't need to pledge business assets like equipment or real estate. However, keep in mind that you will typically need to sign a personal guarantee, which makes you personally liable if the business can’t pay.

The convenience of MCAs comes with some drawbacks that can impact your business's financial health long-term.

The biggest disadvantage is cost. MCAs are substantially more expensive than almost any other financing option, including business credit cards and short-term loans. The effective APR can easily reach triple digits, making it hard to generate a positive return on investment from the funds.

Automatic daily deductions can strain cash flow, especially if sales don't meet projections. This constant drain on revenue can make it difficult to cover operating expenses like rent, payroll, and inventory replenishment.

Some businesses fall into a pattern of taking out new MCAs to cover the payments on existing ones, which is a cycle that’s difficult to break. This stacking of advances can quickly lead to serious financial trouble and threaten the business's viability.

Because MCAs are structured as sales of future receivables rather than loans, they are generally not subject to the disclosures and protections that apply to consumer credit. Some states — including California, New York, Virginia, Utah, Georgia, and Connecticut — have commercial financing disclosure laws that may require MCA providers to disclose standardized cost information.

MCAs may be considered in specific situations where fast funding is essential and the business expects the borrowed funds to generate sufficient revenue to cover the high cost of repayment.

A merchant cash advance might make sense if you fit the following criteria:

MCAs are generally not suitable if you find yourself in these situations:

Be wary of providers who exhibit these behaviors:

If you move forward with an MCA, follow these guidelines to minimize risk:

Before accepting the advance, calculate exactly how the daily deductions will impact your cash flow. Ensure you can still cover payroll, rent, utilities, inventory, and other debt obligations, even after the daily MCA payment is deducted.

Only use MCA funds for investments that will generate quick returns. Good uses include purchasing inventory for a busy season, funding marketing campaigns with proven ROI, buying equipment that immediately increases productivity, or making emergency repairs that are preventing you from operating.

Taking out multiple MCAs simultaneously (stacking) multiplies your daily payment obligations and dramatically increases the risk of default. Resist the temptation to accept additional advances until you've completely repaid the first one.

Before signing, have a clear strategy for avoiding the need for another MCA once this one is repaid. Consider building an emergency fund or establishing a business line of credit for future needs to avoid the high costs of emergency capital.

A merchant cash advance can be a helpful option when you need money fast and don’t have time to wait on a traditional approval process. But that speed usually comes at a steep cost. The same features that make MCAs easy to access can also make them one of the most expensive ways for a small business to get financing.

Before you sign, take a close look at the full price tag, not just the amount you’re receiving upfront. Make sure the daily (or frequent) payments realistically fit your cash flow, and compare other options first. If you do move forward with an MCA, use it with intention: cover short-term needs that can help generate revenue quickly, so you’re not stuck paying a high cost without a clear payoff.

For many small businesses, options like small business loans, SBA loans, or a business line of credit tend to offer better long-term value. Still, if speed is truly the priority and other financing isn’t available, understanding how MCAs work can help you choose with clear eyes and protect what you’re building.

Disclaimer:

*QuickBooks Term Loan and QuickBooks Line of Credit loans are issued by WebBank.

Call Sales: 1-800-285-4854