You could save up to 25% on transaction costs².

Speak with us now to see if you qualify.

Talk to sales 1-800-515-8366

Monday - Friday, 6 AM to 4 PM PT

Table of contents

Table of contents

Key takeaways:

Running a growing business means keeping a lot moving at once. Labor law compliance can make that even harder, especially as you hire in new states, manage a larger team, and keep up with changing rules.

In 2026, employers are navigating a mix of federal, state, and local requirements that affect payroll taxes, employee classification, wage laws, recordkeeping, and other core HR processes. For growing businesses, this creates real risk when teams rely on manual workflows, disconnected systems, or limited in‑house compliance support.

In this guide, we’ll look at the labor law changes shaping 2026, where growing businesses face the most compliance risk, and how connected payroll and HR tools can help you move forward with more confidence.

Businesses face tougher labor law compliance demands in 2026 because they must track more rules across more jurisdictions with less room for error. Federal, state, and local changes can all affect payroll taxes, employee classification, wage requirements, and recordkeeping. As these employment law updates continue, growing businesses need to move quickly and stay accurate.

Growth adds another layer of complexity. When businesses hire across state lines, they must comply with different wage laws, tax rules, filing requirements, and workplace policies. A process that works in one state may fall short in another. That is one reason payroll compliance in 2026 has become a bigger priority for mid-market employers.

Most businesses don’t lack effort. They lack time, visibility, and in-house compliance expertise. HR and finance teams already manage full workloads, and manual tracking makes it harder to keep up with changing requirements. In 2026, that’s the real challenge: regulations keep changing, and growing businesses need better systems and support to keep pace with confidence.

Take a look at some of the key changes shaping labor laws in 2026:

The takeaway? Labor law changes can affect more than one part of your business at once. For growing businesses, that makes it even more important to keep up with changes across states, employee types, and compliance requirements.

As your business grows, compliance gets harder to manage manually. More employees, more locations, and more moving parts can create gaps that lead to mistakes. Here are some of the biggest risk areas for growing businesses.

Hiring across multiple states can make compliance much more complex. Employers may need to follow different tax rules, wage laws, leave requirements, and reporting standards at the same time. A policy that works in one state may not meet requirements in another, which makes it harder to stay consistent across your workforce.

Payroll tax compliance is another major risk area. As you add locations, the number of tax accounts, filing calendars, and deposit schedules multiplies. Small missteps, like using the wrong tax rate in one state or missing a local filing deadline, can quietly snowball into penalties, interest, and extra scrutiny from tax agencies. The more disconnected your systems are, the more your team is relying on memory and manual checks to avoid those mistakes.

Classification mistakes can create serious compliance risks. Employers need to decide whether a worker is an employee or an independent contractor, and whether an employee qualifies as exempt or nonexempt. Those decisions affect overtime pay, benefits, taxes, and other legal protections. When rules change, a role that once seemed clear may need a closer review. Without clear guidelines and strong documentation, businesses can increase their risk of a misclassification claim.

Disconnected systems can make compliance harder to manage. When time tracking, HR, and payroll data live in different places, teams may struggle to keep complete, audit-ready employee records. Missing timesheets, unclear leave records, or unsigned policy acknowledgments can all create problems during an audit or investigation. When records are incomplete, employers often have a harder time supporting their decisions.

Core federal laws, such as the Fair Labor Standards Act, also require employers to retain specific payroll and time records for set periods, so disorganized systems can make basic recordkeeping requirements harder to meet.

Many mid-market businesses don’t have a clear way to track regulatory changes. Teams may piece together updates from emails, articles, webinars, and internal conversations. That makes it harder to turn new information into action. If policies, training, and payroll processes do not keep pace, businesses can expose themselves to avoidable compliance issues.

When a business falls out of compliance, the costs can add up fast. Payroll tax penalties may include late-filing penalties, late-payment charges, and interest on unpaid amounts.

In more serious cases, the IRS can use the Trust Fund Recovery Penalty (TFRP) to hold you personally responsible. It can treat owners, officers, and payroll decision‑makers as personally liable for the full amount of unpaid trust‑fund taxes. For example, if your business fails to remit $50,000 in payroll taxes, you can face a $50,000 personal penalty on top of what the business owes.

The risk doesn’t stop with tax filings. Labor law violations tied to worker classification, overtime, wages, or recordkeeping can also lead to back pay, legal exposure, and audits. A single mistake can affect multiple pay periods, employees, or locations, which can make the cost much harder to contain.

Non-compliance can also disrupt day-to-day operations. Teams may need to stop what they’re doing to correct payroll, review records, respond to notices, and update internal processes. Over time, those issues can create more admin work, pull focus away from growth, and turn small compliance gaps into much larger financial risk.

Do you need HR advisory services for your business? If you are adding headcount, opening new locations, or updating policies more often, the answer is usually yes. HR advisory gives you direct access to trained professionals who help you interpret and apply complex employment laws, so you are not left guessing what a new rule really means for your team.

HR advisory services provide compliance support when the rules become complex. When federal agencies update their view on independent contractors, or a state changes how paid leave accrues, advisors help you sort out what that means for your classifications, pay practices, and policies. Instead of trying to decode legal language on your own, you get clear, actionable advice based on your actual workforce and workflows.

Compliance doesn’t start and end with payroll. HR advisors support you from the moment you draft a job description to the moment you offboard an employee. They can weigh in on employee onboarding checklists, required notices, documentation standards, performance management, and termination procedures. As your company grows, this helps you keep HR processes consistent and fair, while staying aligned with the latest requirements in the states where you operate.

Most businesses don’t have time to monitor every legislative update and agency announcement. HR advisory services track those changes for you and flag the relevant ones. Instead of reacting after a notice arrives, you can adjust your policies and practices before new rules take effect.

Automation can calculate taxes, run payroll, and centralize data, but it cannot answer every judgment call. HR advisory can add a human layer of support for HR and finance teams when they need help applying policies or responding to more complex situations. Together, software and advisory support give you both the efficiency of automation and the confidence of expert guidance.

Even with the best intentions, administrative mistakes happen. That’s where tax penalty protection comes into play. What is tax penalty protection in payroll? It’s a financial safety net that covers certain payroll tax penalties caused by filing errors.

Here are some of the key benefits of this HR compliance protection:

What is an integrated payroll system? It’s a platform that brings payroll, HR, time tracking, and employee data together in one place, rather than scattering them across separate tools. When you use integrated HR systems, you give your team a clearer picture of what is happening and reduce the day‑to‑day friction that can lead to errors.

Here are the key benefits of payroll compliance integration:

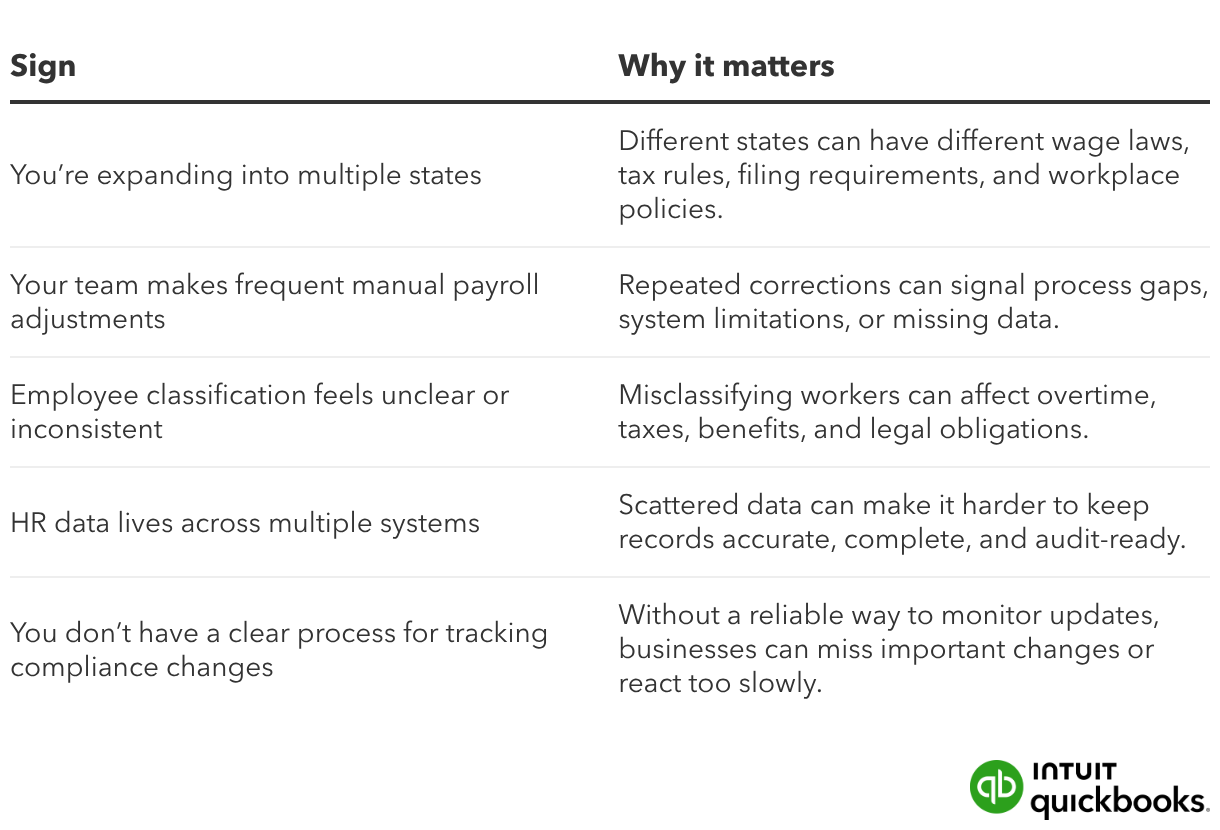

How do you know if your business has compliance issues? Some warning signs are easier to spot than others. This HR compliance checklist can help you identify common signs before they turn into bigger problems.

If more than one of these payroll risk signs sounds familiar, it may be time to review your processes and look for gaps in your compliance workflow.

What software helps with HR compliance? Growing businesses often need tools and support that work together. QuickBooks Workforce Elite helps bring payroll, HR, time, and employee data into one connected system, so teams can manage compliance with more clarity and less manual effort.

Here’s how it helps:

As your business grows, staying compliant gets more complicated. Each new hire, location, and policy adds another layer of rules to track. When you rely on manual processes or disconnected systems, those layers turn into blind spots, and that’s where risk creeps in.

This is why labor law compliance matters so much for growing companies. With a stronger HR compliance strategy, your business can reduce risk, improve consistency, and stay better prepared as rules continue to change. Integrated payroll and HR systems, along with advisory support and added protection, can also help you manage that complexity with more confidence.

Learn how QuickBooks Workforce Elite can help support your growing team.

Call Sales: 1-800-285-4854