You could save up to 25% on transaction costs².

Speak with us now to see if you qualify.

Talk to sales 1-800-515-8366

Monday - Friday, 6 AM to 4 PM PT

Table of contents

Table of contents

Registering a limited liability company (LLC) establishes a critical structural foundation for your business, creating a legal separation between your personal assets and your commercial liabilities. Navigating state filing requirements, drafting foundational governing documents, and setting up compliant operational workflows requires careful execution.

Because the setup process involves distinct legal and financial milestones, only 20% of entrepreneurs with side hustles have registered their business, according to the QuickBooks Entrepreneurship in 2026 survey.

By understanding the core compliance requirements of LLC setup, you can confidently navigate the state filing process. Let's take a look at how to navigate the legal milestones of starting an LLC, while building a resilient financial engine for your business.

**Products and features

**QuickBooks Free: Free is currently available at no charge and may be offered for a limited time. Features and availability, are subject to change or discontinuation at any time, with or without notice. If the Free plan is discontinued, we will notify you in advance and provide you with comparable options to transition to another QuickBooks plan that meets your business needs. Certain add-on products may be eligible for use with the Free plan. To utilize any add-on products, you must agree to additional terms and conditions, and limitations and fees for and any selected add-ons will apply.

Terms, conditions, pricing, special features, service and support options are subject to change without notice.

An LLC is a type of business structure that legally separates you, the owner, from your business. It acts a bit like a shell, shielding your personal assets from business debts while retaining pass-through taxation.

When it comes to forming an LLC, you have many options when it comes to ownership, management type, and tax classification. Choosing the best structure for your business can involve a complex process of data gathering and report filing. To simplify the process and avoid costly FinCEN fines, many modern businesses are turning to artificial intelligence.

AI-powered platforms, like QuickBooks Online, do more than just lighten the paperwork and admin load of forming and managing an LLC. The data-driven clarity they offer can transform your organization into a truly forward-thinking business.

Next, let’s take a look at the steps you’ll need to take to set up your LLC.

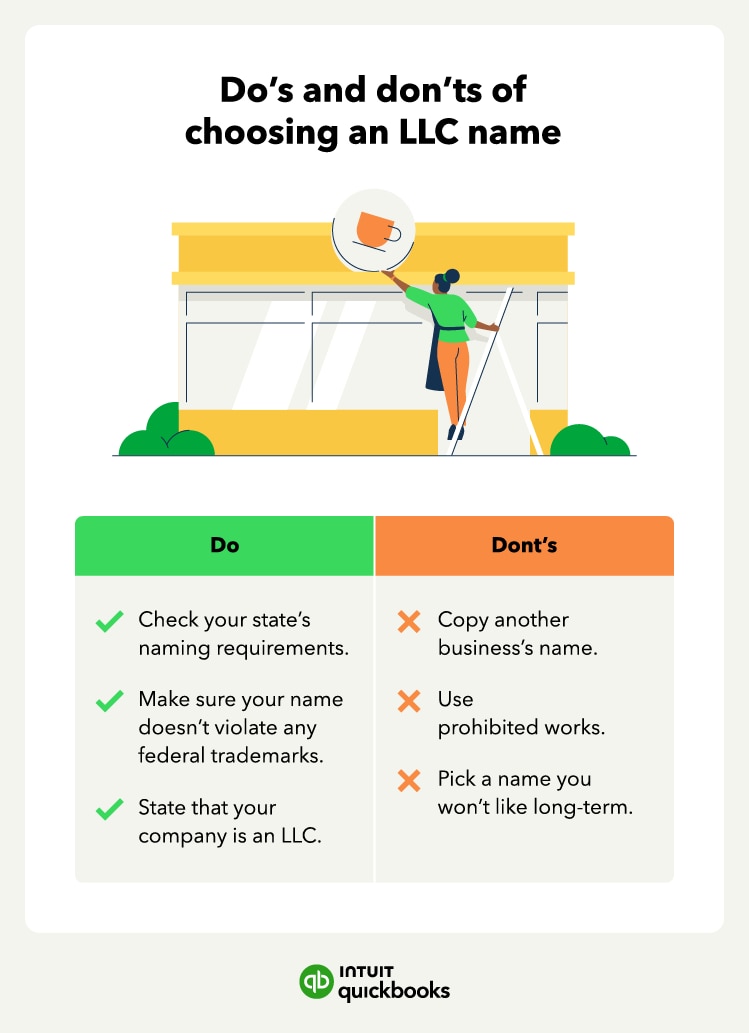

The first step to starting an LLC is to choose a business name and register it with your state. Each state has its own naming rules, usually managed by the LLC or corporations division of the Secretary of State’s office.

While requirements vary, most states follow these general guidelines:

If you’re not ready to file your LLC paperwork, some states let you temporarily reserve a name. You can also register a doing business as (DBA) name, allowing you to operate under a different name for branding and marketing purposes.

While the LLC structure is common in the United States, other countries like the United Kingdom have different legal structures for business formation, such as private limited companies (Ltd.). If you plan to operate internationally, you’ll want to understand the business laws in each country.

Along with the statewide search, ensure that your company name doesn't violate any federal trademarks using the US Patent and Trademark Office website.

Most states require LLCs to designate a registered agent—also known as an agent for service of process—to receive legal documents and official notices on behalf of the business. This can be:

Your registered agent must meet certain state requirements. While your LLC doesn’t need a physical address, the registered agent must have one in the state where the LLC is filed. They must also be at least 18 years old and a resident of that state.

If you hire a company that provides registered agent services, make sure that they are authorized in your state.

While not always necessary for filing with the state, an operating agreement is an essential document for every LLC. It establishes the LLC’s operations and policies, ownership interests, and the rights and responsibilities of its members. This legally binding contract may be required when you register with certain state entities, seek funding from a bank, or try to attract investors.

Prioritizing an operating agreement at the beginning of the formation process can help guide you and other members of your organization through handling business growth, conflicts, or anything else.

Keep in mind that an LLC operating agreement is for internal use; you won’t be required to file it with your state, but your state may explicitly require you to have one.

To ensure your drafted operating agreement matches your business goals and preferred management and tax elections, consider running a review through Intuit Intelligence. The tool can catch discrepancies between the legal paperwork and your financial reality, helping you get the paperwork fixed before finalizing.

For easy access, store your LLC operating agreement with other important business documents, such as your articles of organization.

Every LLC must prepare articles of organization, which state key components of the company, such as:

Once completed, you’ll need to file them with your state. Depending on where you live, the cost to file your articles of organization may vary, with most states ranging from $50 to $150, plus annual fees. There are also fees for optional services like attorney review and registered agents.

Here's a quick summary of how much it costs to start an LLC:

An employer identification number (EIN) is like a Social Security number for your business, which you can apply for by submitting IRS Form SS-4. You’ll need this number when hiring employees, filing taxes, and making business transactions.

If you’re the only owner of your LLC, you may be able to use your Social Security number instead. However, some banks require an EIN to open a business bank account. Having a separate account for your LLC helps keep personal and business finances separate, making it easier to track expenses and manage cash flow.

Another important step in creating an LLC is determining what permits and licenses your LLC needs to operate on a local, state, or federal level.

A lot of the time, your LLC may require a general business or operating license. Depending on where you live, you may have to acquire this license at a city, county, or state level.

Some LLCs may also require additional industry-specific licenses. For example, you may have to acquire a liquor license if you're in the restaurant business.

The sales tax license is usually a requirement for businesses that sell taxable goods or services in states with sales tax. Additionally, if you plan on doing business as a name that differs from your business’s legal name, you’ll need a DBA. As with any other license or permit, DBA requirements can vary depending on where you live.

If you’re unsure what types of permits or licenses your LLC requires, contact your local and/or state government offices for assistance.

Beneficial ownership information (BOI) reports contain limited identifying information, such as legal name and birthdate, for all business owners. This FinCEN requirement is designed to help prevent money laundering and other illegal activities.

Because compliance regulations evolved rapidly following intense legal challenges, founders must maintain a cautious, up-to-date look at their exact filing obligations. Under current 2026 enforcement rules, if you form a standard, non-exempt domestic LLC (such as a single-member or multi-member small business), you are classified as a domestic reporting company and must file a BOI report.

Foreign-based companies registering to do business in the US will also be required to file BOI reports unless they qualify for one of the 23 established exemptions (like being a bank or public utility).

If your entity falls under these criteria, the clock starts ticking immediately upon formation. For any new LLC registered, you must successfully file your initial BOI report within exactly 30 calendar days of receiving formal notice that your entity's registration is effective. Failing to meet this window carries severe statutory consequences

Utilizing a comprehensive accounting ecosystem like QuickBooks Online ensures that the underlying entity records, legal names, tax identifiers, and structural ownership data are systematically organized in a secure, central repository.

After starting your LLC, staying compliant with your state’s requirements is important. Each state has its own rules, so check your state’s official business filing website for specific details.

For example, some states require an annual report with updated LLC information, and you may need to pay an annual fee to keep your LLC active.

You’ll also need to file the appropriate tax forms for your LLC. These structures don’t have a fixed tax classification, so:

We compare single vs multi-member LLCs in greater detail later in the post.

You can also elect to be taxed as an S-corp or C-corp by filing the necessary forms with the IRS. Staying on top of these filings helps ensure your LLC remains in good standing. Learn more about the difference between an S-corp and an LLC.

Use accounting software to deliver key data and reports that can help during tax season.

When forming your LLC, there are three important decisions you need to make:

Knowing the answers to these questions can help you set up your LLC the right way from day one, helping you avoid costly legal and accounting fees later. To ensure your choices align with your business plans, QuickBooks’ Intuit Assist can analyze your goals and suggest which combination of ownership, management style, and tax classification is right for you.

The first part of structuring your LLC is to determine membership and ownership. If you are a sole proprietor creating an LLC for liability protection, then the simplest process is to name yourself as the only owner. Other options include having your LLC owned by a trust or another corporation for strategic asset protection.

On the other hand, if your business is a partnership or you hold the company jointly with others, each individual's ownership stake must be documented.

Ownership and management are two very different matters. When it comes to operating the business, you’ll need to decide if management is all hands on deck (all owners participate) or whether certain owners will be considered passive investors (not participating in management).

Alternatively, you can choose an outside executive (non-owner) to manage the business.

Within bookkeeping software, like QuickBooks Online, you can further define your management structure using roles and permissions to ensure the right people have access to the information they need without compromising your overall security.

Both management structure and ownership information will also need to be included in the articles of organization you file with your state authority.

By default, LLCs are not viewed as a taxable entity by the IRS. Instead, owners are required to report profits on their personal returns, a form of pass-through taxation.

However, you can file an IRS election to have your LLC taxed as an S-Corp. This structure requires you to pay yourself a salary subject to payroll taxes, but allows you to withdraw remaining profits as equity distributions that are exempt from self-employment tax

If you plan to raise venture capital, however, you must avoid the S-Corp election.

IRS regulations limit S-Corps to 100 shareholders, prohibit institutional or corporate investors, and prohibit multiple classes of stock. These strict caps completely block you from issuing the convertible preferred equity that institutional venture funds demand to secure their liquidation and governance rights. Startups seeking outside investors typically choose a C-Corporation structure from day zero to accommodate those complex equity layers.

Evaluating these tax classification options and choosing the best fit before filing prevents expensive legal restructuring later.

Now that you’ve learned how to start an LLC, it’s time for you to get your business up and running. With accounting software like QuickBooks, you can easily track expenses, manage payments, and run custom accounting reports. QuickBooks now offers a free accounting solution, QuickBooks Free which can be a good starting point for those businesses that are not ready for more advanced features. Make informed decisions and get the information you need come tax season with QuickBooks Online.

Call Sales: 1-800-285-4854