You could save up to 25% on transaction costs².

Speak with us now to see if you qualify.

Talk to sales 1-800-515-8366

Monday - Friday, 6 AM to 4 PM PT

Table of contents

Table of contents

Poor construction inventory management ties up working capital, weakens financial reporting, and obscures the true profitability of every project. In a recent QuickBooks survey, 46% of firms said poor financial or resource management is holding them back, and 18% said project costing and price estimates are a common challenge.

This article explains how to tighten material controls in construction, track costs accurately across jobs, and choose the right tools to close the gap between field execution and the balance sheet.

In 2026, effective construction inventory management minimizes the time capital is frozen in stock that has not yet been billed to a project. That frees up working capital you use to fund payroll, cover supplier payments, and fund future bids.

Here are three ways better material control shortens the cash conversion cycle:

1. Eliminates the cost of emergency runs

When crews don't know what materials are on the truck or in the warehouse, they leave billable work to go and get it. The cost goes well beyond the part itself. In field service, Aquant's Benchmark Report found that 14% of truck rolls are unnecessary, and jobs not resolved on the first visit cost 34% more when extra trips, parts, and labor are factored in.

For example, a technician spends 90 minutes fetching a $50 part. But the true cost, including fuel, vehicle wear, and lost billable time, approaches $250.

If you have a fleet of 15 all making similar emergency runs, the costs quickly add up to a material cost variance between your estimate and your actuals. This buried cost erodes the profit predicted at the bid stage.

Reducing these unplanned trips ensures that the labor you pay for is spent on job execution, not procurement.

Track the gap between planned purchase orders and unplanned expense transactions coded to the same material categories. That difference is your reactive purchasing cost, and it belongs in every job margin review.

Track the gap between planned purchase orders and unplanned expense transactions coded to the same material categories. That difference is your reactive purchasing cost, and it belongs in every job margin review.

Real-time visibility into material levels helps finance and procurement teams time bulk purchases to match the specific needs of the current pipeline. This matters in times of price volatility.

For example, AGC's analysis of Bureau of Labor Statistics data found that the producer price index for steel mill products jumped 17% in 2025, the steepest annual rise since 2022. Aluminum and copper also posted double-digit increases. In this environment, the timing of a purchase makes a material difference to job margins.

Integrating inventory levels with the Work in Progress schedule lets procurement see confirmed demand in advance and buy in line with scheduled use. That makes it easier to secure better pricing when the buying window is right and avoid paying inflated "spot" prices on the day the field crew realizes they are short on materials.

Sureties and lenders examine your company’s liquidity on its balance sheet when assessing its risk profile. According to the Construction Executive's surety report, bonding companies typically apply a multiplier of around 10x to net working capital when deciding on the maximum bonding capacity.

That's where material management directly affects the numbers. If materials are expensed on delivery rather than recorded as inventory assets until they are allocated to a job, the balance sheet understates the firm's liquidity, and the surety sets bonding capacity against a lower figure.

Get the classification right consistently, and the firm presents a stronger, more substantiated financial profile in bond and credit reviews over time.

Sureties and lenders examine your company’s liquidity on its balance sheet when assessing its risk profile. According to the Construction Executive's surety report, bonding companies typically apply a multiplier of around 10x to net working capital when deciding on the maximum bonding capacity.

That's where material management directly affects the numbers. If materials are expensed on delivery rather than recorded as inventory assets until they are allocated to a job, the balance sheet understates the firm's liquidity, and the surety sets bonding capacity against a lower figure.

Get the classification right consistently, and the firm presents a stronger, more substantiated financial profile in bond and credit reviews over time.

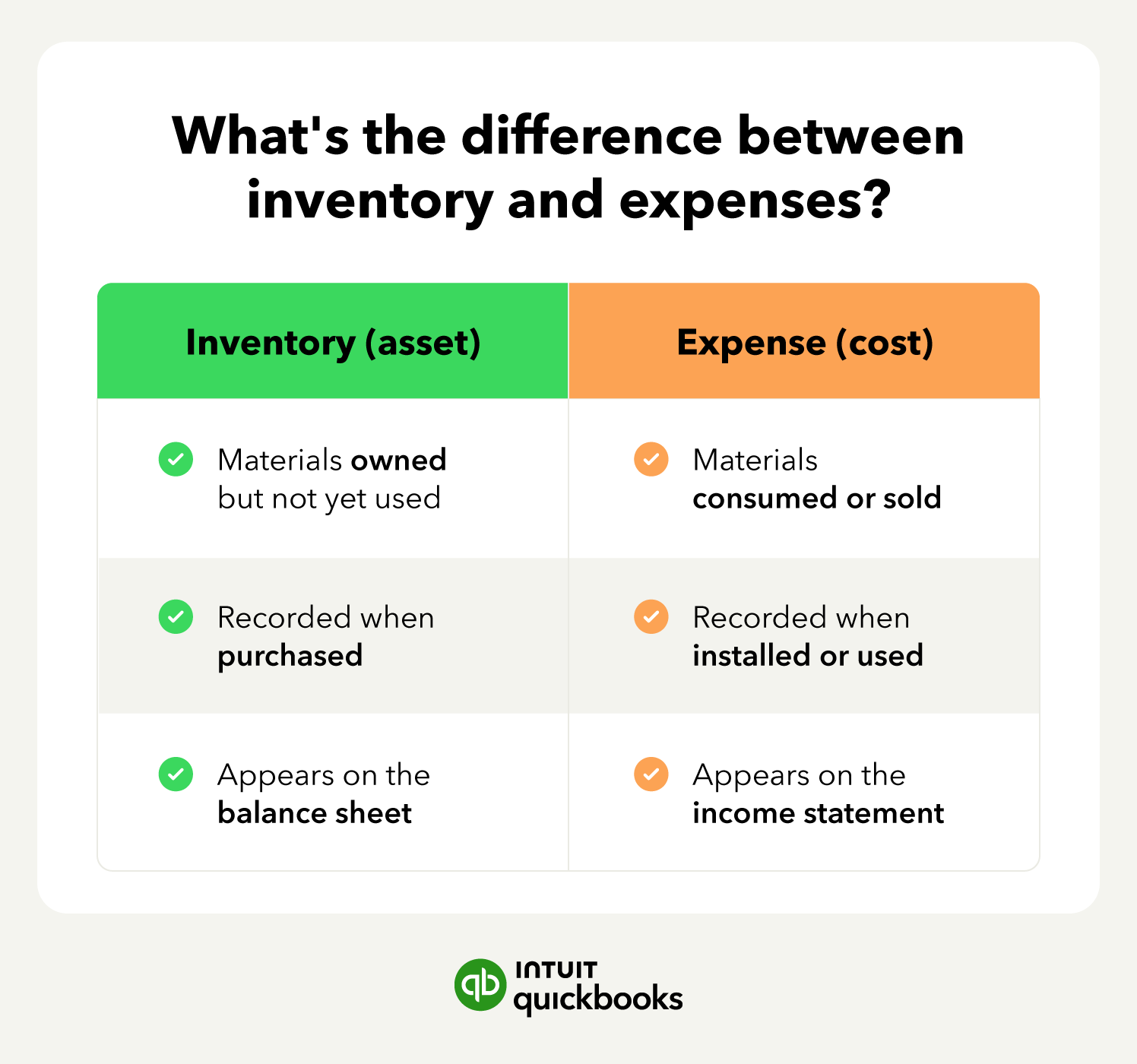

Inventory management in construction depends on the flow of materials from procurement to the job site. High-value stock held in central storage until drawn for a job is usually an asset. Materials purchased for immediate use on a single job are typically direct job expenses.

When the treatment isn't consistent, bonding reviews, project bids, and capital planning are all based on numbers that don't match the actual material flow in the field.

Set a dollar-value threshold to make the rule consistent across jobs. For example, materials above a set amount (for example, $500) that are held in stock until drawn for a job are classified as assets.

Items below that threshold or purchased for immediate consumption on a single job are written off as job costs upon receipt. Without a formal classification policy, job costing varies, and the accounts lose consistency across the portfolio.

A consistent classification rule means you compare the margin across jobs, knowing the material inputs were treated the same way.

Example: A mechanical contractor found that $180,000 in copper fittings and valves had been charged directly to the P&L across 12 active projects, rather than being treated under its inventory policy. A quarterly review against the decision matrix identified the error and corrected the treatment. The correction added $180,000 back to the asset side before the next bond renewal.

Review the threshold annually and align it with the firm's materiality level for audit purposes. If a construction company's bookkeeping fails to consistently distinguish between these two categories, the balance sheet is already less reliable than it needs to be.

An Item Receipt workflow helps construction firms record received materials into inventory rather than pushing the cost straight into project expense at delivery. That gives finance a more accurate view of what is still sitting on the balance sheet versus what has moved through purchasing.

In QuickBooks Online Advanced, the Item receipt feature supports that workflow by updating the quantity on hand when materials arrive, linking the receipt to the purchase order and later to the vendor bill. This ensures the field team has visibility into what has arrived for their project without waiting for the back office to process the final invoice.

Recording materials through an item receipt workflow reduces the noise in margin reviews caused by delivery timing and provides finance with a better basis for cash planning.

Example: A general contractor received $200,000 of structural steel for three concurrent projects but would not install most of it for four to six weeks.

Using Item Receipts, the steel remained on the balance sheet rather than being recorded in the project P&L, so each project's margin reflected actual consumption as the steel was used. That gave finance more accurate cash-planning numbers for the next billing cycle.

Working capital is often wasted when unused materials from a completed project are left in a technician's garage or stored at a finished job site. Without a formal return-to-stock protocol, those materials are never credited back to the original job and are not available for the next estimate. You end up purchasing stock you already own.

A return-to-stock process requires materials to be logged back into inventory, credited to the original job's cost code, and returned to usable stock for future project bids. The result is less repeat purchasing on the next project, and accounts that include every item the business still holds. It’s one of the simplest improvements to job-costing accuracy, and one of the most overlooked.

Materials returned to inventory reduce your repeat-purchasing costs and protect your margin on the next job you bid.

Example: An electrical contractor finishing a tenant build-out had $35,000 of unused conduit, junction boxes, and wire spread across four vans. A formal recovery log identified the materials, credited them back to inventory, and logged them as available for the next estimate. That cut $8,000 off the material order on the following project by using stock the firm already owned.

As a firm takes on more projects, maintaining a clear view of unallocated materials becomes a critical financial control. While field-based tools provide operational support, maintaining a strong financial source of truth within your accounting system ensures that material costs never slip through the cracks.

Firms managing significant material volume across multiple job sites and service vehicles often carry unused stock without knowing it. In construction, this inventory represents cash that has been spent but isn't yet earning a return on a project. It ties up working capital, overstates the value of your available resources, and obscures the actual material requirements for upcoming bids.

Automated tracking earns its place by identifying which materials are sitting idle and which are ready to be reallocated to active jobs. With that data, you make procurement decisions based on actual project needs, field teams stop reordering items already in the fleet, and less capital gets tied up in unused materials over time.

Example: A plumbing contractor with materials spread across 20 service vehicles might find that 14% of their unallocated stock had not been assigned to a job in 12 months. By leveraging automated alerts linked to project usage, the firm could identify excess materials from previous tenant improvements. That gives finance the data to apply those assets to new estimates and stop reordering the same materials for new project starts.

When using specialized field apps for dispatch or project management, the data must feed directly into your general ledger. Without this alignment, the field team and the accounting department see two different cost realities, and neither is accurate for financial reporting.

Ensuring your field workflows feed into QuickBooks Online Advanced reduces that gap. The accounting system remains the single source of truth, providing finance with a current view of total asset value across all project sites and vehicles. When field records and the general ledger are in sync, you have a verified financial position ready for lenders, sureties, and audit reviews.

Example: A hypothetical fire protection contractor found a $140,000 discrepancy between its field app and QuickBooks at quarter-end because on-site material usage wasn't being reported back to the office in real time. Connecting these workflows closed the gap and gave the controller one substantiated job-cost figure for a successful bond renewal.

Once materials are consumed and costs are recorded against the job, they flow into progress billing. A consistent construction invoice template helps keep the billing accurate across projects.

QuickBooks Online Advanced notifies teams when essential job materials are running low, so they reorder before a shortage forces a rushed purchase that blows the project budget.

It also tracks lead times on regular orders, so procurement knows how far ahead to buy to keep the project schedule on track. Last-minute orders carry premium pricing and shipping fees that directly cause margin leakage on the affected job.

Firms investing in construction automation use alert-based reordering to keep more purchases on plan and aligned with the WIP schedule. Procuring materials based on accurate lead-time data avoids the rush premium that erodes the profit predicted at the bid stage.

Example: An HVAC contractor reordered refrigerant and copper tubing based on manual checks at the shop that didn't account for how quickly active jobs were drawing down vehicle stock. Low-stock alerts triggered a reorder two weeks earlier, avoiding a rush premium on three active projects, protecting the net margin of each job.

QuickBooks Online Advanced includes anomaly detection that highlights unusual transactions during invoice review. That means procurement and finance can spot unexpected vendor pricing at the approval stage, before those costs are permanently locked into the job's final actuals.

Without financial controls that check invoices against historical project costs, pricing errors, and gradual markups pass through to the job and silently erode margins across every project using that supplier.

When vendor pricing goes unchecked at invoice entry, the overpayment repeats on every new project start until finance catches it.

Example: A concrete contractor saw projected margins drop over two quarters with no obvious explanation. After applying anomaly detection at the invoice approval stage, procurement identified a pattern of incremental vendor markups on rebar.

Procurement renegotiated the rate and prevented further margin leakage on the remaining phases of those projects.

Getting inventory classification and control right means tighter cash control, more reliable margins, and a balance sheet that reflects assets your company actually owns.

Book a call with a QuickBooks Online Advanced specialist to find out how to improve inventory control and reporting in your construction business.

Call Sales: 1-800-285-4854