Employer responsibilities for payroll taxes in Pennsylvania

As a Pennsylvania employer, you're responsible for managing a complex array of federal and state payroll taxes, which involves careful calculation, timely withholding, and accurate reporting to various government agencies. Here’s an overview of what you should know.

Registering for payroll taxes

To comply with Pennsylvania state regulations, employers must register for payroll taxes before beginning business operations. This critical first step ensures you're set up to handle requirements like unemployment compensation, state income tax withholding, and wage reporting. Here are the three key steps to get started:

- Get an Employer Identification Number (EIN): Before registering with the state, you’ll need a Federal Employer Identification Number (EIN) from the IRS. This number identifies your business for federal tax purposes. You can apply for an EIN quickly and easily through the IRS website.

- Register with the Pennsylvania Department of Revenue and the Department of Labor & Industry]: Once you have your EIN, register your business with the Commonwealth using the PA-100 Enterprise Registration Form. This unified registration allows you to set up your accounts for Pennsylvania employer withholding tax and unemployment compensation. You can complete this registration online through the Pennsylvania Department of Revenue.

- Report New Hires: Within 20 days of hiring a new employee, you must report them to the Pennsylvania New Hire Reporting Program. This helps support child support enforcement and other state-administered programs.

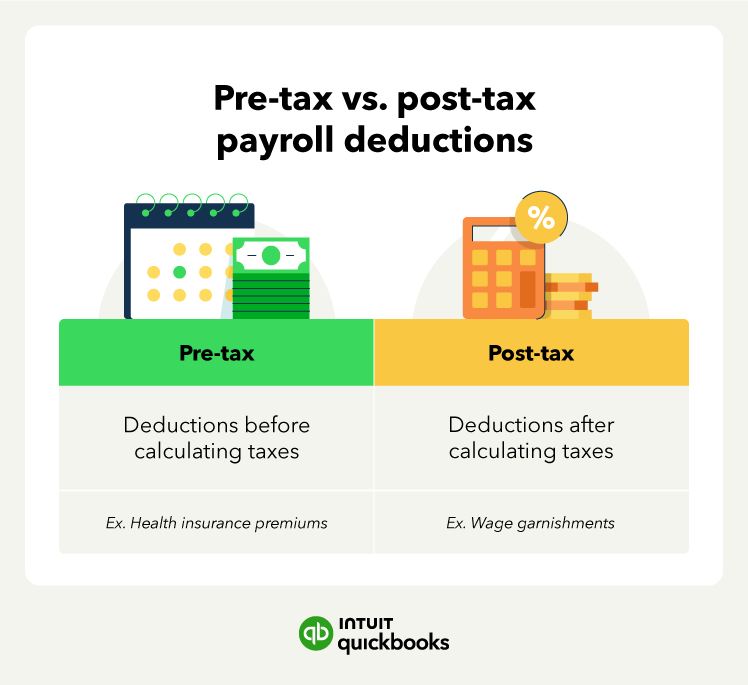

Calculating payroll taxes

Accurately calculating payroll taxes is essential for Pennsylvania employers, not only to ensure employees are paid correctly, but also to avoid costly penalties and interest. Fortunately, you have several reliable options to get it right:

- Check government websites: The Pennsylvania Department of Revenue and the Department of Labor & Industry provide up-to-date tax tables, wage limits, and guidance to help you calculate state income tax withholding and unemployment compensation contributions.

- Payroll software: Some small business software payroll programs have built-in Pennsylvania tax tables that automate calculations, saving you time and minimizing the chance for errors.

- Professional services: If you prefer to outsource payroll, a professional payroll service can handle everything for you.

Whichever method you choose, make sure you stay updated on the current tax rates and wage limits, as these can change every year.

Withholding state payroll taxes

Once you've accurately calculated the correct payroll tax amounts, the next step is to withhold the proper amounts from your employees' wages and remit them to the appropriate Pennsylvania authorities. This includes state income tax, local Earned Income Tax (EIT), and unemployment compensation contributions.

Pennsylvania Personal Income Tax (PIT): You must withhold 3.07% of taxable wages for state income tax from each employee’s paycheck. Withholding should be calculated based on gross compensation and remitted according to the Pennsylvania Department of Revenue’s deposit schedule—either semi-weekly or monthly, depending on your total withholding amount.

- Example: If an employee earns $5,000 in a month, you would withhold: $5,000 × 3.07% = $153.50 in PIT.

Local Earned Income Tax (EIT) and Local Services Tax (LST): Most Pennsylvania municipalities impose a local EIT, typically 1% to 3.8712%, which must be withheld and submitted to a designated local tax collector. You may also need to withhold the Local Services Tax, which can be up to $52 annually, usually deducted in equal amounts per pay period.

- Example: For an employee who lives and works in a municipality with a 1.5% EIT and earns $1,000 per week: $1,000 × 1.5% = $15 withheld per week for EIT.

Unemployment Compensation (UC): As the employer, you're responsible for paying state UC taxes. For 2025, new employers generally pay 3.822% on the first $10,000 of each employee’s wages. Employees also contribute at a rate of 0.07%, which you must withhold from their paychecks.

- Example: If an employee earns $1,000:

- Employee UC contribution = $1,000 × 0.07% = $0.70 withheld

- Employer UC contribution = $1,000 × 3.822% = $38.22 paid by employer

By applying these calculations to each paycheck, you ensure accurate withholdings and compliance with state requirements.

Remitting state payroll taxes

In Pennsylvania, if your business withholds taxes from employee paychecks, you'll need to file tax returns with the state.