You could save up to 25% on transaction costs².

Speak with us now to see if you qualify.

Talk to sales 1-800-515-8366

Monday - Friday, 6 AM to 4 PM PT

Table of contents

Table of contents

Cost remains the biggest barrier for 47% of people starting a business in 2026, yet many founders overlook thousands of dollars in potential tax savings sitting right in their own homes. While Americans estimate they need $28,000 to launch, the actual median cost is $12,000. And the home office deduction helps bridge that gap by turning housing overhead into a tax break.

If you’re a freelancer, contractor, or small business owner, your home office acts as a strategic financial asset. This guide explains how to navigate the 2026 tax rules, the strict IRS eligibility tests, the impact of the One Big Beautiful Bill tax changes, and the step-by-step process for calculating your total deduction.

Before you start measuring your desk, you must pass the threshold of IRS eligibility. The home office tax deduction is taken on Schedule C of your Form 1040 and requires the use of Form 8829 to calculate the deduction. The government looks for two specific factors to determine if your home office is a legitimate business expense.

The exclusive and regular use test

The IRS requires two main criteria to determine if a specific area of your home qualifies for a business tax deduction. To meet the criteria, you must demonstrate that a portion of your residence is used for business both exclusively (no personal use) and regularly (consistent, non-incidental use).

Exclusive use means that a specific portion of your home is used solely for your trade or business. If you work from your kitchen table, you cannot claim the kitchen as a home office because you also use it for dining.

The space must be a separately identifiable area. This does not necessarily require four walls and a door; a dedicated corner of a room partitioned by a bookshelf or a rug can qualify, provided no personal activities occur within those boundaries.

For your home business to qualify, this means:

Regular use means you use the space for business continuously. Incidental or occasional work in a spare bedroom does not meet the standard. The IRS looks for a pattern of use that suggests the space is a vital, everyday component of your business operations.

Examples:

Take photos of your dedicated workspace to document its use exclusively for business. These visuals can be helpful if you're ever audited.

Take photos of your dedicated workspace to document its use exclusively for business. These visuals can be helpful if you're ever audited.

Your home office must be the primary location where you conduct the most important activities of your business. If you are a consultant who meets clients at their offices but spends your evenings at home doing billing, bookkeeping, and project planning, your home office qualifies as your principal place of business.

The key is that your home office is essential to the overall operation and management of your business.

Examples:

Keep a detailed business calendar that shows the regular use of your home office for business activities. Include client meetings, project work, and any other tasks that demonstrate it's your primary place of business.

The 2026 tax updates brought about by the One Big Beautiful Bill have specific implications for home-based workers. While the fundamental structure of the home office deduction stayed intact, the bill modified how related expenses interact with other deductions.

One major change involves the State and Local Tax (SALT) cap increase to $40,400 for 2026. For those using the actual expenses method, the ability to deduct a portion of property taxes as a business expense can serve as a workaround to the standard SALT limits.

Additionally, the bill updated the depreciation schedules for home-based assets, making it more important than ever to choose the correct calculation method during the first year of business.

While the home office deduction can be a valuable tax break, it's not available to everyone. Here are some common situations where you wouldn't be eligible:

If you work for an employer and receive a W-2, you generally cannot claim the home office deduction, even if you work from home regularly. This deduction is primarily intended for self-employed individuals and small business owners who use their homes as places of business.

If your home-based activities are primarily a hobby rather than a for-profit business venture, you won't qualify. The IRS requires that your activities be conducted with the intent to make a profit. Factors they consider include whether you keep business records, advertise your services, and have a separate business bank account.

If the space you're claiming is used for both business and personal activities, it doesn't qualify. The exclusive use rule requires that the space be used only for conducting business. For example, if you use a spare bedroom as both an office and a guest room, you can't claim the deduction.

Carefully review the IRS guidelines to determine your eligibility. If you're unsure whether you qualify, it's always a good idea to consult with a tax professional.

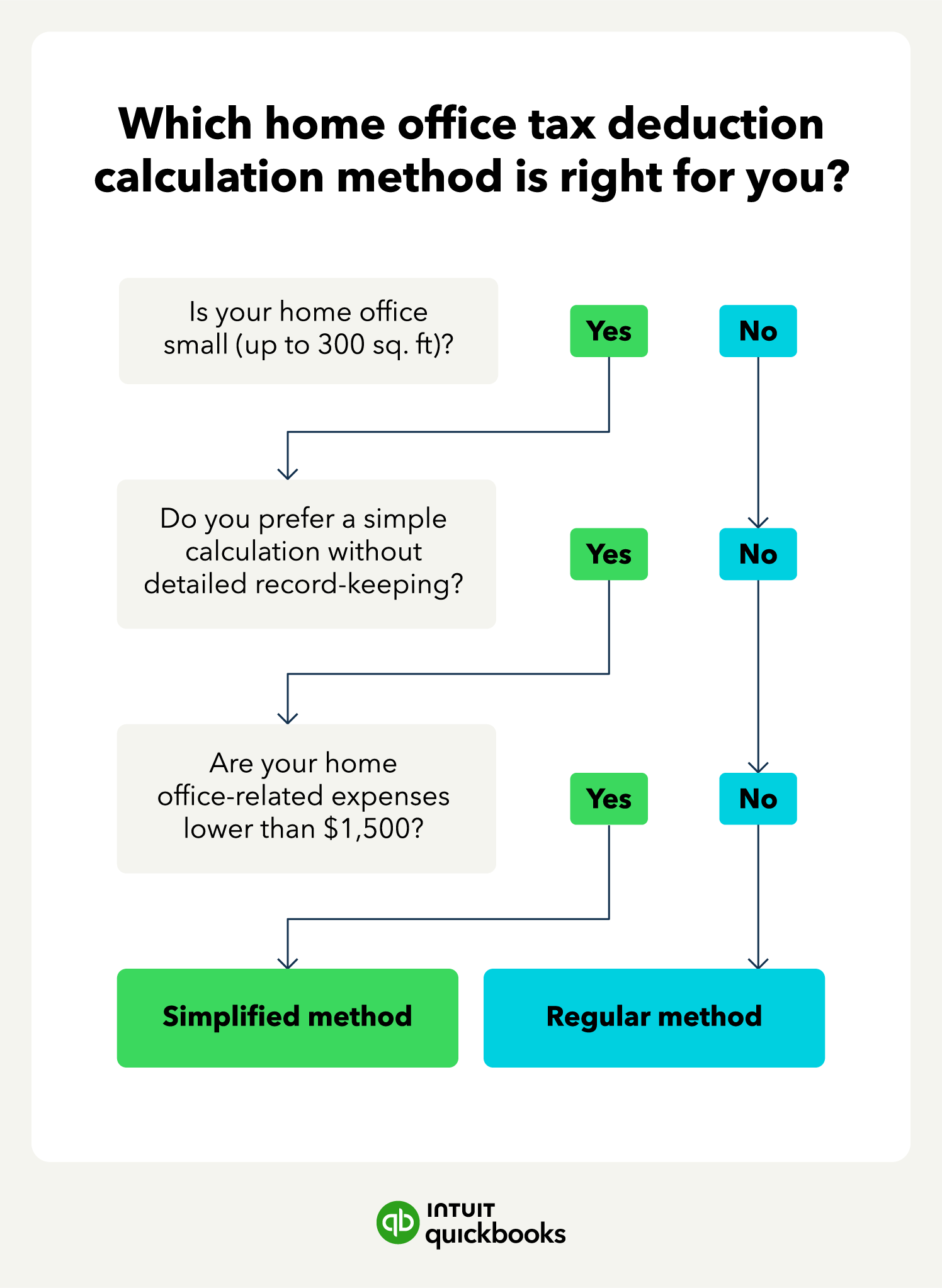

When calculating your work-from-home office tax deduction, you have two options to choose from: the simplified method or the regular method. Here’s a quick overview of how both calculations work according to the IRS.

This method is popular among those with smaller home offices (under 300 square feet) who prefer to avoid complex calculations.

One of the main advantages of this method is that you don't have to calculate depreciation on your home. With the regular method, you depreciate the portion of your home used for business, which can get complicated.

The simplified method eliminates this step, making your tax calculations much easier. You also avoid the potential recapture of depreciation when you sell your home.

If your home office space is 300 square feet or less, the simplified method will likely be the quickest and easiest way to claim your deduction.

The regular method can potentially result in a larger tax deduction, especially if you have a larger home office or significant home-related expenses.

Here's how it works:

The regular method requires meticulous record-keeping. You'll need to track all your home-related expenses and maintain documentation to support your deductions. This includes receipts, invoices, and bank statements.

If you choose the regular method, your software will generate Form 8829 to detail your home costs. If you choose the simplified method, you skip Form 8829 entirely and enter your deduction directly on Schedule C.

Always keep a copy of your square footage calculations in your permanent tax file, regardless of which form you use.

Most home office costs fall into two categories: direct and indirect. Understanding the difference is vital because it determines whether you deduct 100% of the cost or only a small percentage based on your office size.

Direct vs. indirect expenses

Direct expenses solely benefit your workspace. If you buy a desk for your office or pay a contractor to paint only that room, you can typically deduct 100% of that cost.

Indirect expenses benefit your entire home. Costs like your mortgage interest, electricity, and roof repairs are shared. You can only deduct the business percentage of these costs (e.g., if your office is 10% of your home, you deduct 10% of your electric bill).

Here’s a look at some examples of expenses that fit each category:

If you own your home and use the actual expenses method, the IRS requires you to depreciate the business portion of your home over a 39-year recovery period.

This treats your office as a business asset that wears out over time. While this increases your deduction now, keep in mind that you may have to pay recapture tax on that depreciation when you sell the home. Many homeowners opt for the simplified method specifically to avoid this future tax complication.

After you select which method will work best for your business, here's a step-by-step breakdown of how to calculate your deduction.

To calculate how much of a home office tax deduction you qualify for, use the simplified method:

Square footage of home office * $5 = Home office deduction

Let's say your home office is a 100-square-foot room used exclusively for business. Using the simplified method, your calculation would be:

100 square feet * $5/square foot = $500

In this example, your home office deduction would be $500.

The simplified method has a maximum deduction of $1,500. This means you cannot write off more than 300 square feet of home office space, even if your actual workspace is larger.

Here's how to determine your deduction using the regular method:

(Home office square footage / Total home square footage) * Indirect Expenses + Direct Expenses = Home office deduction

If your office is 200 square feet and your home is 2,000 square feet, your business percentage is 10%.

You then apply that 10% to your indirect expenses. These are costs that benefit the whole house, such as electricity, water, and home insurance. Direct expenses (like painting the office or installing a dedicated business phone line) are 100 % deductible.

Use a spreadsheet or accounting software to track your expenses and calculate your deduction. This will help you stay organized and ensure accuracy.

Use a spreadsheet or accounting software to track your expenses and calculate your deduction. This will help you stay organized and ensure accuracy.

Whatever deduction you’re looking for, run the numbers to see which method would benefit you most. If the paperwork becomes too burdensome, expense-tracking software like QuickBooks Self-Employed can help you perform the calculations and make the right decision.

Out of all of the small business tax deductions, qualifying for the home office tax deduction can potentially result in the largest amount of savings this tax year.

With two calculation methods to choose from and online accounting tools at your disposal, managing tax deductions for your home office can be made more manageable. As always, consult a tax professional to understand your options.

Call Sales: 1-800-285-4854