5 advantages of limited liability partnerships

Forming a limited liability partnership (LLP) offers several compelling advantages, particularly for professionals seeking to collaborate while mitigating personal risk. Here's a look at the key benefits:

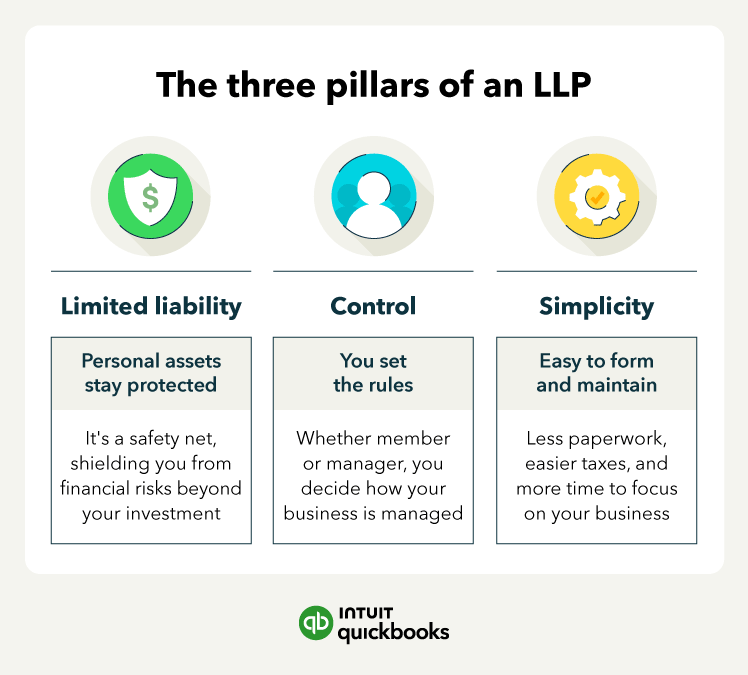

1. Protection through limited liability

One of the primary draws of an LLP is the significant liability protection it offers. Partners are generally shielded from personal responsibility for the business's debts and, crucially, for the negligence, malpractice, or misconduct of other partners. This shields their personal assets (like homes, cars, and savings) from lawsuits or creditor claims arising from their colleagues' actions or overall business liabilities they didn't directly cause. Liability is typically confined to a partner's own actions and their investment in the firm.

2. Simplified pass-through taxation

LLPs are typically treated as "pass-through" entities for tax purposes, which simplifies tax obligations considerably. The business itself does not pay corporate income tax. Instead, the partnership's profits and losses are "passed through" directly to the individual partners, who then report their share on their personal income tax returns and pay taxes at their individual rates. This structure avoids the "double taxation" often faced by traditional C corporations, where profits are taxed first at the corporate level and again when distributed to owners as dividends.

3. Collaborative management flexibility

Unlike some other business structures, an LLP allows for significant flexibility in how the business is managed. Generally, all partners in an LLP have the right to participate actively in the management and decision-making processes of the business. This facilitates collaborative control and a shared approach to running the firm, contrasting sharply with limited partnerships (LPs) where limited partners are typically passive investors with no management rights.

4. Enhanced professional credibility

Operating as an LLP can enhance a firm's professional image and credibility, especially in fields like law, accounting, architecture, and medicine where this structure is common and well-regarded. Adopting the LLP structure can signal a commitment to professional standards and stability, potentially building greater trust with clients, suppliers, and financial institutions. In some jurisdictions or professions, it may even be the standard or preferred entity type.

5. Customizable internal structure

LLPs offer partners considerable freedom in defining their internal operating rules and governance. Through a comprehensive partnership agreement, partners can tailor the structure to their specific needs. This agreement can precisely outline capital contributions, profit and loss distribution methods, partner responsibilities, voting rights, procedures for admitting new partners, and protocols for partner departures or dispute resolution, creating a bespoke operational framework.

Consider the long-term implications of management structure. An LP's rigid separation of management and investment can create internal friction if the business direction shifts. An LLP's collaborative model might offer more adaptability in the long run.

Consider the long-term implications of management structure. An LP's rigid separation of management and investment can create internal friction if the business direction shifts. An LLP's collaborative model might offer more adaptability in the long run.

Don’t forget to check for available web domain names and social media handles— securing these assets now prevents future headaches and ensures consistent branding as your business grows.

Don’t forget to check for available web domain names and social media handles— securing these assets now prevents future headaches and ensures consistent branding as your business grows.