How LLCs are taxed

One of the biggest advantages of an LLC is tax flexibility. The IRS allows an LLC to choose how it wants to be taxed, which can lead to potential tax savings.

Single-member LLC: pass-through taxation to Schedule C

By default, the IRS treats a single-member LLC as a "disregarded entity." This means the LLC itself doesn't pay taxes or file a separate tax return. Instead, the business's income and expenses "pass through" to the owner's personal tax return.

You report this information on Schedule C (Form 1040), the same form used by sole proprietors. The net profit is then added to your other personal income and taxed at your individual income tax rate.

Multi-member LLC: partnership taxation on Form 1065

A multi-member LLC is automatically taxed as a partnership. The LLC files an informational tax return (Form 1065) to report its income, deductions, gains, and losses.

However, the LLC itself doesn’t pay taxes. Instead, it issues a Schedule K-1 to each member, detailing their share of the profits or losses. Each member then reports this information on their personal tax return (Form 1040).

Self-employment taxes for LLC members

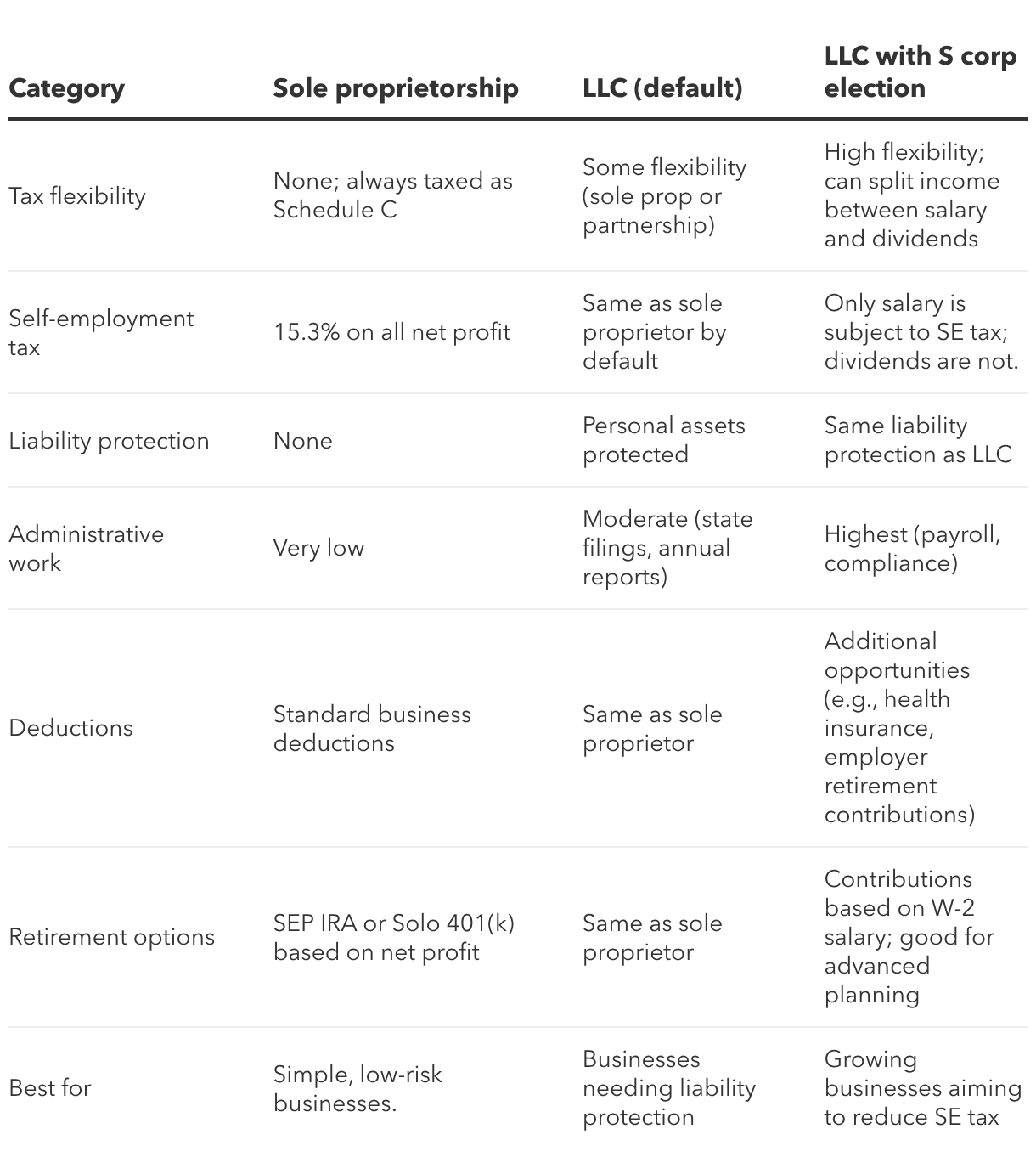

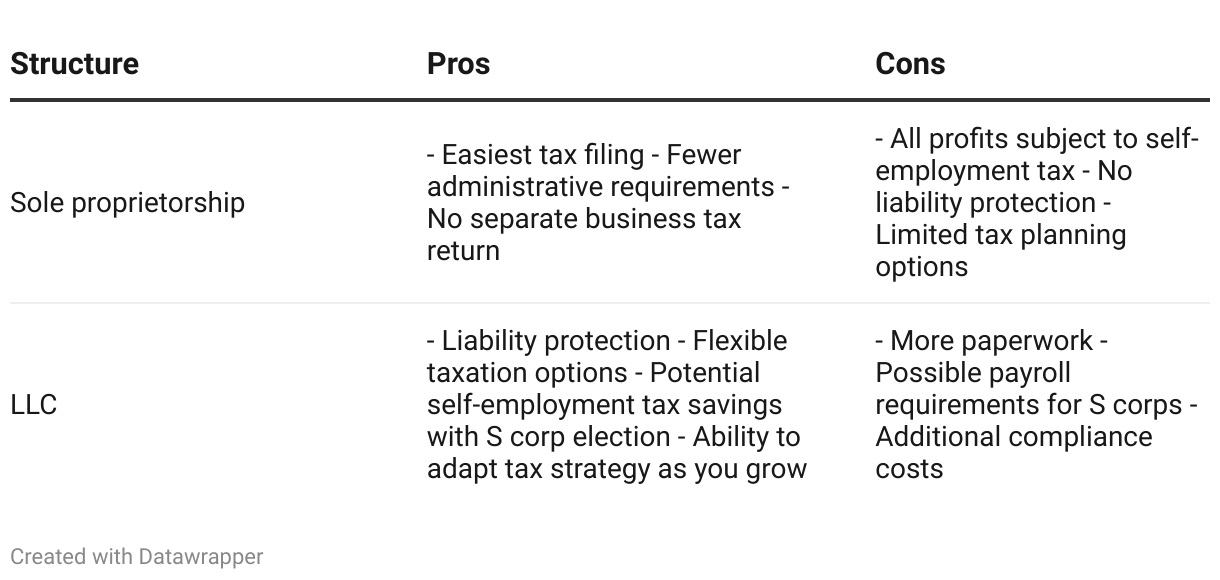

If you actively participate in the business, you’re considered self-employed. That means you pay 15.3% self-employment tax (Social Security + Medicare) on your share of the profits. This applies whether you’re in a single-member or multi-member LLC taxed as a sole proprietorship or partnership.

Do I have to pay self-employment tax if I form an LLC?

Yes, unless your LLC elects to be taxed as an S corporation, which can reduce how much of your income is subject to self-employment tax.