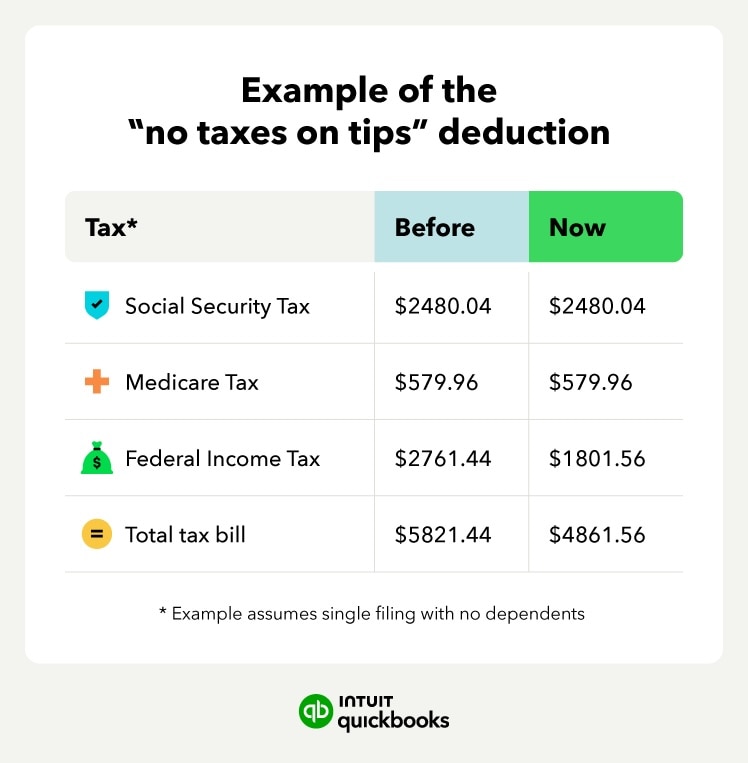

Eligibility requirements

To qualify for the income tax deduction under OBBBA, an individual's tips must satisfy specific requirements. The occupation must be one of the nearly 70 identified by the IRS as customarily receiving tips, like waitstaff, and the tips themselves must meet the definition of "qualified tips".

Outside of the occupational guidelines, this deduction will apply only to qualified tips reported on a W-2, 1099, or Form 4137. This means the deduction will be available to both traditional employees and self-employed individuals.

A work-eligible Social Security number will be required to file for this deduction. Additionally, those who are married will need to file jointly. This deduction will not be available when married filing separately.

Unfortunately, individuals who work for (or are self-employed under) a business that is categorized as a Specified Service Trade or Business (SSTB) won’t be able to take this deduction and will have to pay taxes on tips.

Income limitations

The new tip tax deduction does come with some income limitations and phase-out rules. To qualify for the full deduction, the MAGI (modified adjusted gross income) caps are:

- $150,000 for single filers

- $300,000 for married filing jointly

Above these income amounts, the deduction will begin phasing out and will zero out at:

- $400,000 or single filers

- $550,000 for married filing jointly

This deduction will be available to both those who take the standard deduction and those who itemize their deductions.

The maximum annual deduction (per individual) is $25,000. However, for self-employed taxes, there is an added rule: The deduction cannot exceed net income from tip-based work.

So, if you made $40,000 with half that being tips, but you had $25,000 worth of expenses, you’d only be able to deduct $15,000 of your tips instead of the full $20,000.