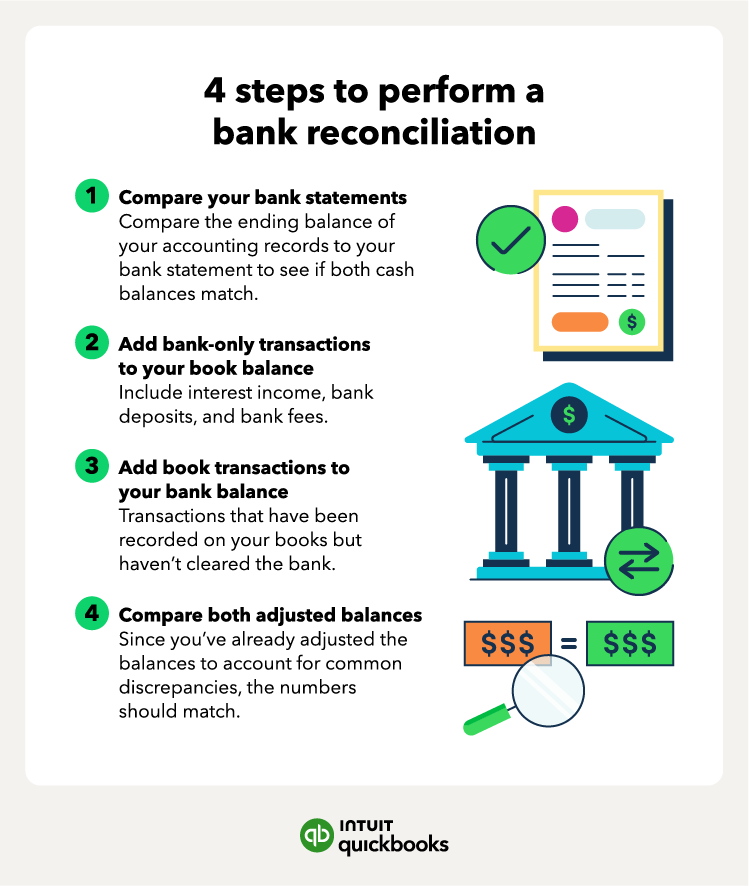

1. Compare your bank statements

Start by laying out your bank statement alongside your accounting records. Go line by line, matching each transaction by date and amount.

If something’s missing or doesn’t line up, flag it. The issue might be timing, like a check that hasn’t cleared yet, or a data entry error. Make a note of any discrepancies so you can dig into them later.

2. Add bank-only transactions to your book balance

Next, check for transactions on the bank statement that aren’t recorded in your books. These often include things like interest earned, automatic deposits, or bank fees.

Update your records by adding any income (like interest) and subtracting charges (like monthly fees or overdrafts). These items are usually listed at the end of your bank statement.

3. Add book transactions to your bank balance

Now, account for any transactions in your books that haven’t cleared the bank yet, such as deposits in transit or outstanding checks that haven’t been cashed.

Add pending deposits to the bank balance, and subtract any unprocessed checks. If you’re using accounting software, flag these items so you can track them when they clear.

4. Compare both adjusted balances

After you’ve made all your adjustments, your book balance and bank balance should match. If they do, congrats—your reconciliation is complete.

If the numbers don’t match, double-check your entries for typos, missed transactions, or timing issues. Keep digging until you’ve accounted for every difference. Reconciliation is about accuracy, and it’s worth the time to get it right.