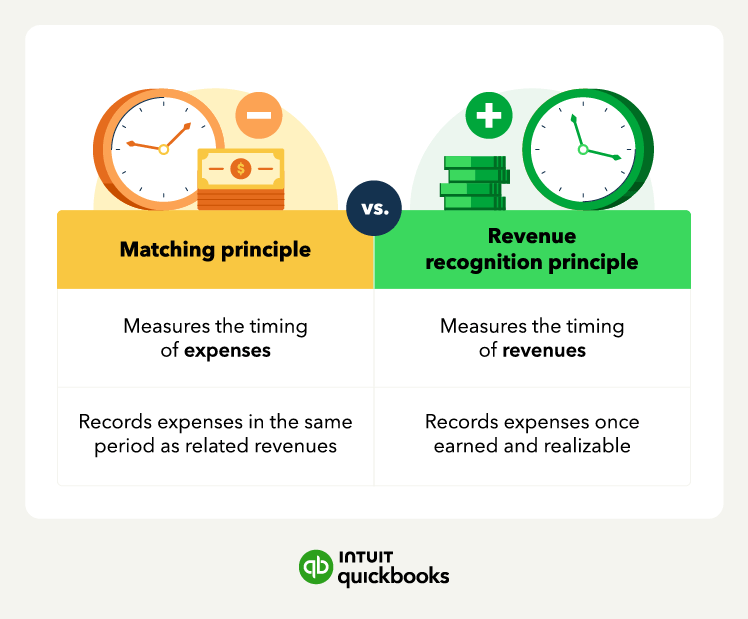

Ensures accurate profitability and performance measurement

The matching principle helps you create a more realistic record of your business’s financial performance. When you report costs alongside the revenues they help bring in, you avoid skewing your results with timing inconsistencies.

If instead, you recognize expenses too early or too late, you could distort your net income in two periods—artificially inflating profits in one while understating them in another.

Promotes consistency in financial reporting

Consistency is key in financial reporting, and the matching principle is the key to consistency. When you always record expenses in the same period as their related revenues, your financial statements (especially your income statement) follow a uniform timing. That makes it easier to compare your performance across accounting periods.

This helps internal stakeholders, like you and your managers, make better informed strategic decisions. Similarly, it gives external stakeholders, such as prospective lenders and investors, reliable data they can use to decide if they want to work with you.

Supports proper asset depreciation and amortization

The matching principle is the reason you spread the cost of long-term assets over the period you expect them to help your business. It’s called depreciation for tangible assets, like vehicles or buildings, and amortization for intangible assets, like patents or trademarks.

For example, say your business buys a patent for $20,000 with a 10-year useful life. Instead of deducting $20,000 upfront, you would amortize the amount over the next 10 years. Under the straight-line method, that would create $2,000 of amortization expense each year during the decade the patent contributes to your business.

If you use the cash basis of accounting, you don't have to worry about the matching principle—it only applies when you follow accrual accounting.

If you use the cash basis of accounting, you don't have to worry about the matching principle—it only applies when you follow accrual accounting.