Key bookkeeping tasks

Wondering how to do basic bookkeeping for your small business? To keep your startup financially healthy, getting a handle on your bookkeeping is a must. Here’s a breakdown of common tasks you’ll need to manage:

Track and analyze financial transactions

Up-to-date records are essential for accurate financial reporting and decision-making. A bookkeeper should record sales revenue (income), bills and operating costs (expenses), equipment and property (assets), and loans and debts (liabilities). Specific records include sales receipts, purchase invoices, bank statements, and expense reports.

Transaction recording methods: This task can be managed manually or by using automated accounting software, like QuickBooks, which streamlines the task and helps minimize errors.

Reconcile accounts

Account reconciliation means comparing your bank account balance with your ledger's cash balance to confirm they match. Reconciling your accounts helps spot discrepancies, prevent fraud, and keep your financial records accurate.

Account reconciliation is typically done on a daily or monthly basis. Businesses with higher transaction volumes, such as restaurants, commonly reconcile accounts daily.

Manage accounts payable

Managing accounts payable (AP) involves handling unpaid bills to suppliers, vendors, and creditors. Startups sometimes find this somewhat challenging due to limited resources, lack of experience, cash flow constraints, and rapid growth. Yet effective management of the following AP tasks is essential for financial stability.

- Invoice processing: Receiving, verifying, and recording invoices from vendors accurately and efficiently.

- Payment authorization: Establishing approval workflows and ensuring that invoices are reviewed and approved by appropriate stakeholders before payments are made.

- Payment execution: Scheduling and executing payments on time to avoid late fees and maintain positive vendor relationships.

- Recordkeeping: Maintaining accurate and up-to-date records of all invoices, payments, and vendor information for financial reporting and compliance.

- Vendor management: Building and nurturing strong relationships with vendors to negotiate favorable terms, ensure timely delivery of goods and services, and resolve any issues.

A professional bookkeeper, equipped with robust accounting software, can streamline these AP responsibilities, ensuring timely payments, accurate recordkeeping, and fostering positive vendor relationships.

Organize invoices

Bookkeepers should monitor invoices, ensuring they're sent out promptly and following up if there are any payment delays. Efficient invoice management helps maintain healthy cash flow, which is vital for covering essential operational expenses and investing in growth opportunities.

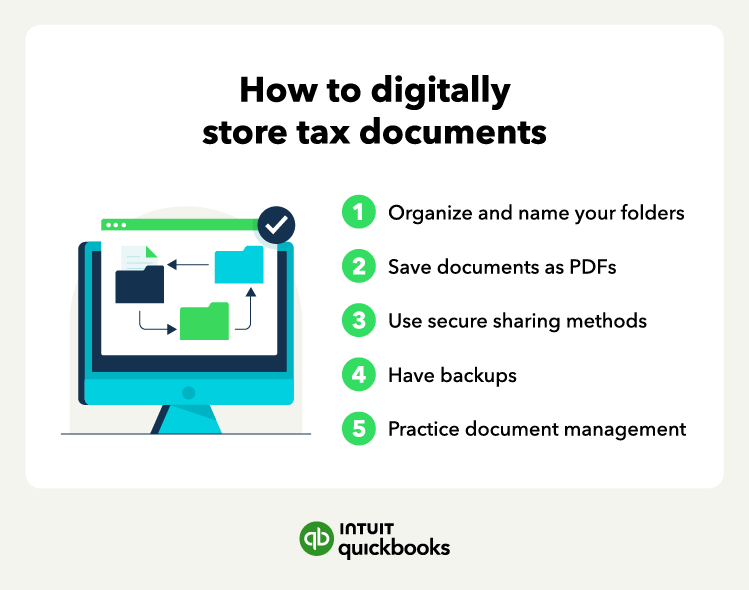

Digital storage and organization

Invoices are also essential documents required for taxes and compliance. Consider the benefits of digitally storing your tax-related documents. This storage method not only saves physical space but also helps keep them secure and ensures easy access and organization. Here's a step-by-step guide to help you:

Step 1: Organize and name your folders

Create a clear folder structure for each tax year (e.g., "2024 Taxes"). Within each folder, create subfolders for different categories like income, expenses, deductions, etc. Name your files descriptively (e.g., "W2_2023_JohnDoe.pdf") for easy retrieval.

Step 2: Save documents as PDFs

Convert all your tax documents into PDF format, which helps provide compatibility across different devices and prevents accidental changes to the original files.

Step 3: Choose a secure storage method

You could use a cloud storage provider or consider QuickBooks Online, which offers a secure document storage feature. Always protect your files with strong passwords or encryption.

Step 4: Maintain backups

Create multiple backups of your digital tax records. Store them on different devices or cloud services to safeguard against data loss.

Step 5: Practice document management

Regularly review and update your digital files. Delete unnecessary documents and ensure your folder structure remains organized.